Goldman Sachs: Repricing Resilience Amidst Strategic Reinvention

- Earnings Beat: Q1 EPS rose 22% YoY to $14.12 with 18% ROTE, defying restructuring concerns.

- GBM Strength: Record equities and FICC results power a 20.2% ROE; AI boosts efficiency.

- Stable AWM, Streamlined Platform: $24B AWM inflows and improving Platform margins signal resilience.

- Undervalued: Trading at 11.36x P/E and 1.58x TBV, SOTP points to 15–25% upside.

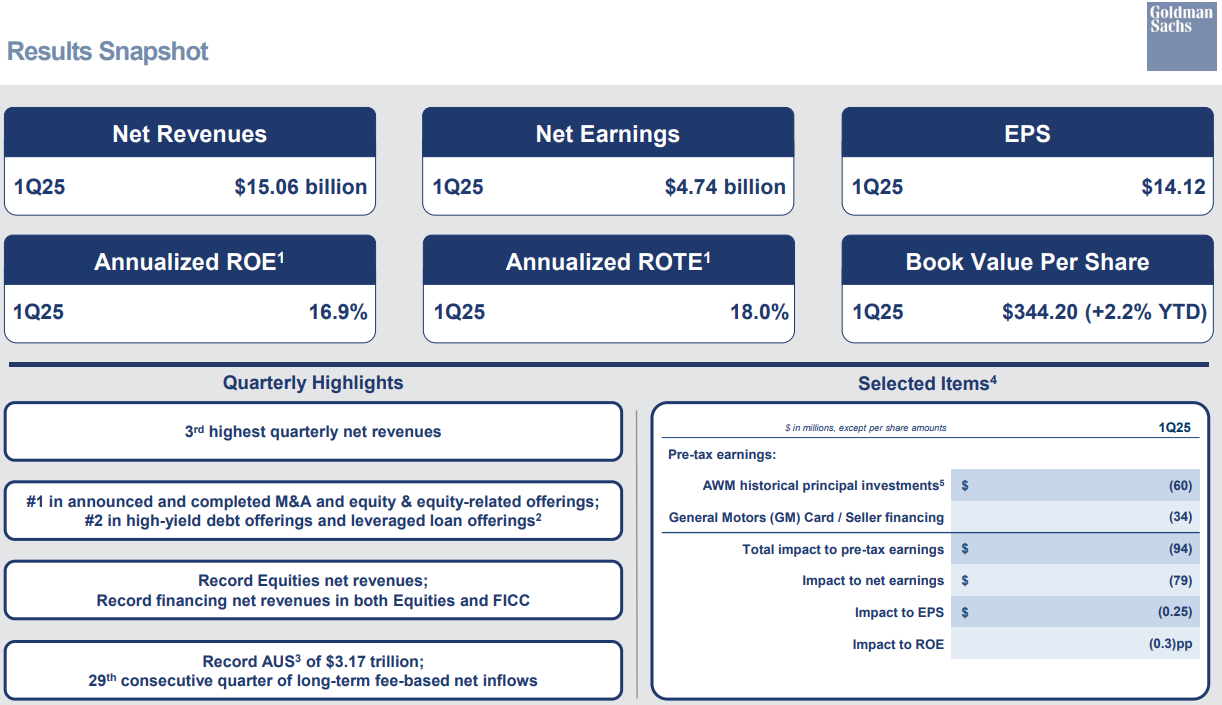

TradingKey - Goldman Sachs (GS) steps into Q2 2025 with a mix of operational rebound and long-term readjustment, offering investors a multifaceted but intriguing enigma. Despite consensus opinion being wary in light of structural issues regarding its consumer banking pull-back and asset management overhaul, the company's Q1 results defy gloom. Goldman registered strong $15.06 billion in net revenues and $4.74 billion in net earnings, a 22% YoY EPS advance to $14.12 and a remarkable 18.0% ROTE, its finest since the post-pandemic boom. More striking is the company's consistency: this is its 29th successive quarter of net long-term flows in Asset & Wealth Management (AWM), even in the event of divergent segment performance.

This counter-narrative is worth noticing. Goldman's equities and fixed income financing groups reported record results, bolstering its fortress in Global Banking & Markets (GBM) even as competitors such as Morgan Stanley endure M&A-related diversions. The firm's lean strategies in Platform Solutions and divestment of legacy principal investments signal careful redeployment of capital. Even more significantly, Goldman is applying artificial intelligence (AI) as both an internal efficiency lever and client productivity driver, even as it positions to rebound in investment banking in cyclical fashion. Cumulatively, Goldman Sachs is not merely coasting through trouble, but quietly transforming itself into an AI-leveraged, high-margin, capital-light giant.

Source: Q1 Deck

Business Model Redesign: From Principal to Platform

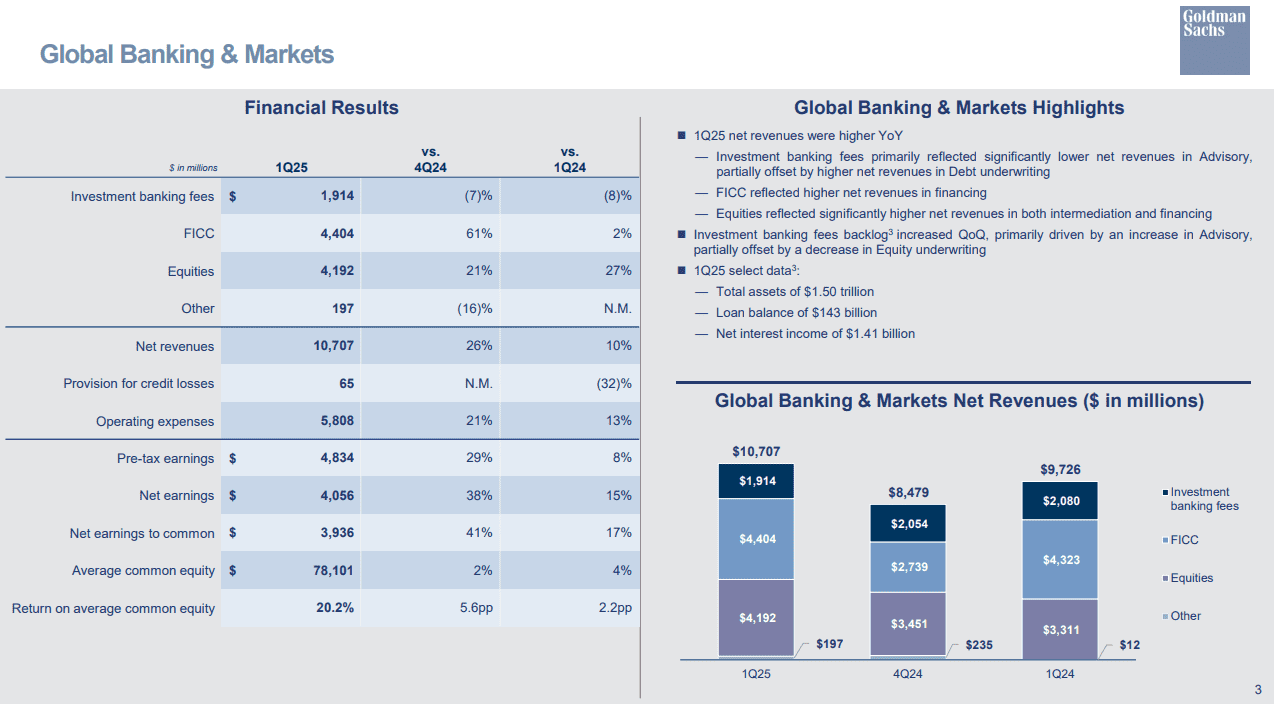

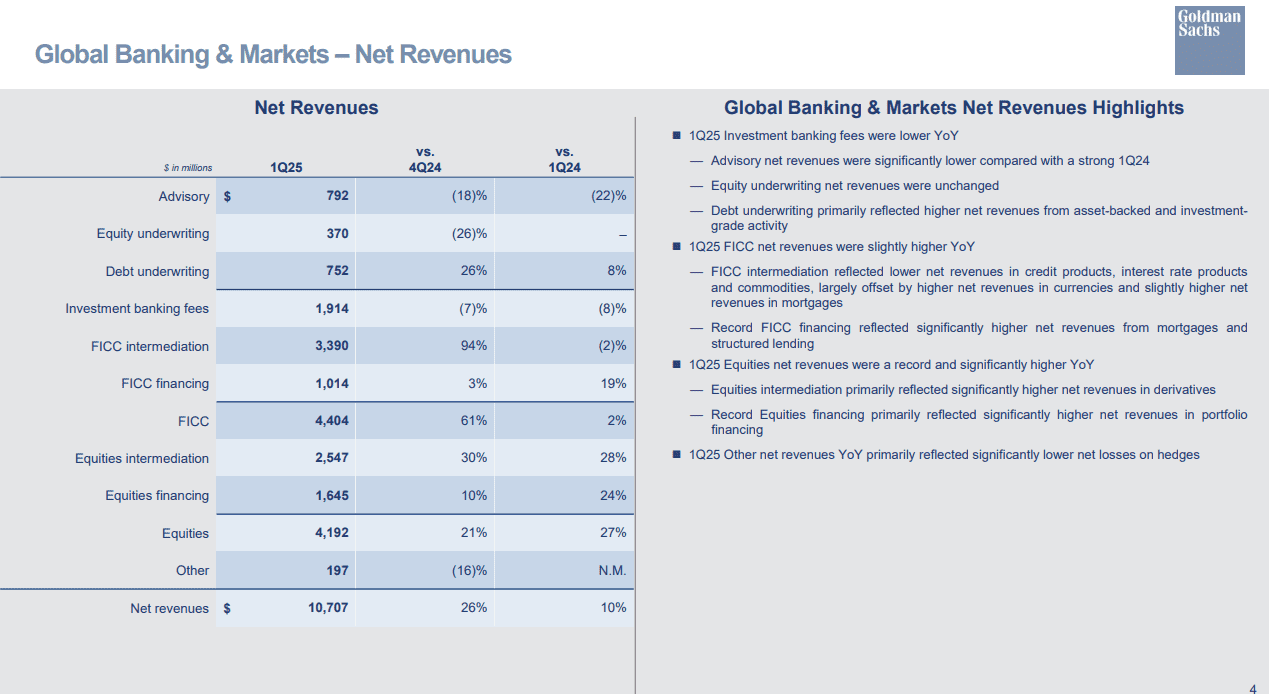

Fundamentally, Goldman Sachs is active in three core business segments: Global Banking & Markets (GBM), Asset & Wealth Management (AWM), and Platform Solutions. GBM is still the crown jewel, generating more than 70% of Q1 2025 revenues. It continues to dominate competitors in high-margin products and sectors like derivatives, portfolio financing, and debt underwriting. Equities revenue grew 27% YoY to an all-time high of $4.19 billion, with both intermediation and financing performing robustly. FICC financing saw a 19% YoY rise, evidencing the bank's prowess in leveraging collateral-rich relationships.

Conversely, AWM is in a deliberate transition. Net revenues declined 3% YoY to $3.68 billion due to a $5 million loss in equity investment income and a sharp drop of 63% in debt investment revenues. The segment's underlying health, however, remains robust. Management and other fees increased by 10% YoY off an all-time high of $3.17 trillion in Assets Under Supervision (AUS), a $36 billion quarter-over-quarter rise with $29 billion of net flows coming from Wealth clients alone. This reflects Goldman's capacity to hold high-value relationships in place even as transitioning to fee-generating, lower-capital strategies.

Platform Solutions, Goldman's young consumer and transaction banking business, accounted for only $676 million in Q1 revenues, down 3% YoY. Nevertheless, losses reduced, and the unit produced net interest income of $768 million. Given that Goldman is tempering expectations from this business (including closing down the GM credit card business), this segment is likely to become a more streamlined, enterprise-focused infrastructure facilitator.

Essentially, Goldman's in-house AI initiatives are optimizing processes in risk modeling, sales analysis, and regulation. Not commercialized in as straightforward way as rivals with AI-as-a-Service, Goldman is subtly adding algorithmic leverage to raise productivity per banker and offset costs of regulation and credit. This technologically native change increases scalability and customer customization with minimal risk to margins.

Source: Q1 Deck

Moats, Momentum, and Market Share: Goldman's Position

Goldman's investment banking position is still best-of-breed. Through Q1 of 2025, it was #1 in global M&A, equity and equity-related deals, and common stock issuance. Even with advisory revenues down sequentially YoY to $792 million, which is more indicative of cyclical softness than competition slipping, Goldman's backlog increased sequentially based on a pipeline of multi-billion-dollar complex transactions. Equity underwriting stayed even, but debt underwriting rose an 8% YoY as investment-grade and asset-backed security demand picked up.

In competition with peers such as Morgan Stanley, which is threatened with integration from both E*TRADE and Eaton Vance, or JPMorgan, with its capital markets business still less premier in non-debt markets, Goldman's targeted GBM engine enjoys superior margin strength. With ROE in GBM reaching 20.2% and net income climbing 17% YoY, the segment is still the company's economic flywheel.

In asset management, Goldman's 61 basis point fee rate on $341 billion in alternative investments is competitive, although Blackstone is ahead in absolute AUM and client depth of channel. Goldman's particular advantage is in the mix of discretionary and advisory mandates, with improved margin mix. Nevertheless, difficulties in selling off historical principal holdings continue, with $8.8 billion still on balance sheet, which may obscure actual efficiency.

In the meantime, Platform Solutions is confronted with uphill competition from digitally native platforms such as SoFi as well as traditional banks investing in consumer-facing technology. Goldman's withdrawal from consumer-facing credit products reflects a turn toward high-yield cash management and B2B transaction banking, where size, rather than experimentations, is paramount. Therefore, the firm is sacrificing optionality in favor of efficiency, something that will not appeal to all growth-oriented investors.

Source: Q1 Deck

Growth, Margins, and Capital Deployment: The Balanced Powerhouse

There are multiple secular and cyclical drivers underpinning Goldman's growth path. Debt issuance in GBM is recovering in tandem with credit markets, and derivatives and FICC lending are being fueled by volatility and rising rates. Management highlighted increased interest in structured lending and mortgage-backed products, where Goldman's balance sheet capacity and risk acumen facilitate premium pricing.

AWM is quietly compounding. The firm is making a transition to capital-light strategies that aim to maximiz recurring revenue with net Q1 inflows of $24 billion coupled with sustained fee growth. Alternative investment fundraising totaled $19 billion in Q1, with $6 billion in hedge fund platforms and $7 billion in credit platforms. Weak equity and debt investment results are due to timing mismatches, not structural deterioration.

Operating costs continue to be in focus. Operating costs increased by 5% YoY to $9.13 billion, with compensation costs increasing by 6% from performance-related accruals. CIE costs decreased substantially, though, and the company is expecting ongoing benefits from technology synergies and decreasing FDIC charges. The efficiency ratio increased marginally to 60.6%. The provision for credit losses decreased by 10% YoY to $287 million, which reflects improving asset quality despite macro uncertainty.

Goldman is also returning capital aggressively. Q1 buybacks totaled $4.36 billion (7.1 million shares at $610 average), alongside a $3.00 quarterly dividend. The board has approved a new $40 billion repurchase program, signaling confidence in intrinsic value despite economic ambiguity.

Valuation Reset: Premium or Fair?

GS trades at $509.49, which is around 1.58x tangible book value, based on an assumption of TBVPS of ~$322.95. With forward P/E at 11.36, based on forward EPS of $44.85, the company looks cheap compared to both its past trading range and peers such as JPMorgan, which generally trades at around a 12x forward multiple. Though providing superior return metrics, particularly based on ROE and ROTE, Goldman finds itself priced at a relative discount, something that is not typical for the firm based on its extent of dominance of the capital markets

Valuation based on Sum-of-the-Parts Indicates

A sum-of-the-parts (SOTP) analysis further supports the bullish argument:

- Global Banking & Markets (GBM): With projected revenue of over $42 billion annually at segment EBIT margin of ~35%, we calculate ~$15B of EBIT. Using a 9x EV/EBIT multiple, appropriate for high-margin, capital-efficient franchise, values the company at $135 billion.

- Asset & Wealth Management (AWM): Having revenue of the order of $15 billion with a lower margin of 21% EBIT, the total EBIT that this segment generates each year is roughly $3.1 billion. Assuming a reasonable EV/EBIT multiple of 12, this division is worth ~$37 billion.

- Platform Solutions: Continuing to evolve and almost breakeven, the division generates ~$2.7 billion revenue. Assuming a conservative revenue multiple of 1, we give it a value estimate of $2.7–3 billion.

Corporate Adjustments: Subtracting the around $12 billion of net debt, along with other adjustments (including minority interests), brings the total equity value to about $162–163 billion. With a market value of $165.4 billion, Goldman is nearly at intrinsic value based on this analysis. Even with modest assumptions of upside (e.g., +10% GBM uplift or Platform margin recovery), the implied value of the equity approaches $180 billion, which would be indicative of fair value at $700–750/share, implying 15–25% above current price levels.

Managing Known and Unknown Risks

Goldman Sachs is still exposed to various macro and firm-specific risks. Ongoing softness in M&A or sudden declines in capital markets activity would put pressure on GBM earnings, particularly in view of revenue concentration. Increased regulation, particularly Basel III Endgame proposals, would potentially add to capital needs or reduce balance sheet room. In addition, the partially executed exit from legacy principal investments may yield periodic write-downs.

Additionally, integrating AI, which is opportunistically attractive strategically, is not as transparent in terms of ROI as is commercializing AI directly by peers. Becoming technologically competitive as an independent non-software provider is also an open question for the firm. Finally, geopolitcal risks, surprise inflation, or credit shocks, particularly in leveraged loans, may have negative impact across segments.

Conclusion

Goldman Sachs is carrying out an under-the-radar but powerful overhaul, marrying its premier capital markets franchise with operations enhanced by artificial intelligence and capital-lite asset management. Volatility in headlines might mask this metamorphosis, however, but the firm’s record return on equity, careful return of capital, and under-sold valuation make it an enduring compounder. Investors capable of ignoring noise from quarter to quarter might discover asymmetric upside in a structurally superior franchise.