Earnings Season Starts Under Heavily Clouded Skies

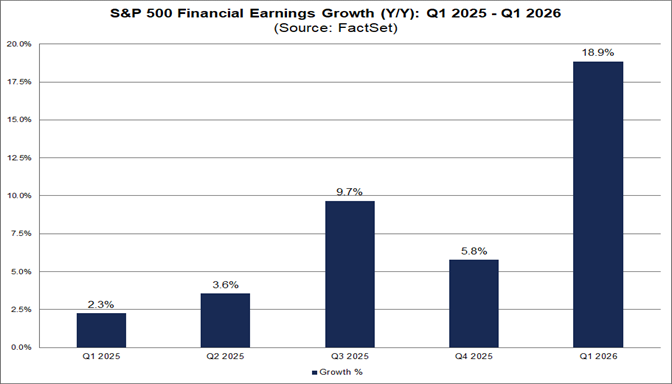

TradingKey - The earnings season begins this week as Wall Street's biggest banks report against an extremely volatile macro backdrop. Hopes are tenuous. While the S&P 500 Financials sector is expected to increase earnings modestly, 2.3% year over year, by FactSet's estimate, there is huge dispersion in the background.

The industry is tested by all the crosscurrents buffeting markets: rising interest rates, rising tensions in geopolitics, and encroaching credit worries.

Large banks have a contradictory earnings landscape.

Source: Seeking Alpha

Net interest income is still high because of high interest rates, yet deposit pricing competition has picked up, credit expenses have accelerated, and capital markets activity slowed once again following a temporary Q1 pick-up. Both consumers and corporates have become cautious and loan growth is slowing. In contrast, market volatility, fueled by rising Treasury yields and re-escalating U.S.–China trade tensions, has increased both risk and opportunity in investment banking and trading.

The next five days feature reports from JPMorgan (JPM), Wells Fargo (WFC), Goldman Sachs (GS), Citi (C), and Bank of America (BAC). Each institution is exposed to various segments of the economy, yet collectively, their performances will provide the strongest signal yet as to whether America's financial system is weathering the pressures, or is just starting to break down under them. In so many ways, this earnings season is as much concerned with guidance, provisioning, and balance sheet strength as it is headline EPS or top-line growth.

It is in this uncertainty that the path ahead for the Federal Reserve hangs in the balance. While not at center stage, markets will look for signs of distress in every earnings report for hints of speeding up policy. Let's review what each of the major banks can be expected to do as they share center stage.

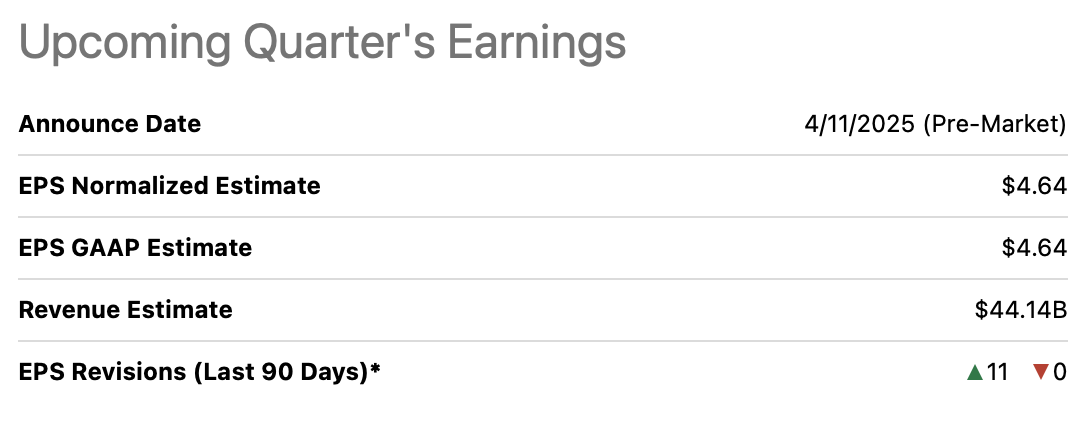

JPMorgan (JPM) – Schedules April 11 Pre-Market Report

JPMorgan is set to get earnings season started as the industry's barometer, and everything hinges on CEO Jamie Dimon's message. Consensus forecasts modest EPS expansion based on healthy net interest income, yet the street's closer watch will include builds in reserves. With Dimon's earlier caution on recession prospects due to any trade war, the market is anticipating sharp credit provisioning in commercial and industrial loan books. While JPMorgan's fixed income unit can profit from increased volatility, investment banking is set to be weak amidst capital market freeze.

Watch for emphasis by JPM in its remarks on liquidity coverage ratios (LCR), deposit migration, and whether the bank anticipates systemic tightening in its lending standards. Dimon's words might also indirectly send a message about whether he thinks Fed intervention is needed or premature.

JPMorgan is expected to post FY2025 EPS of $18.30 on $175.6 billion in revenue, but estimates reflect a -7.35% YoY decline in earnings amid rising reserve expectations and volatile capital markets. Investors will focus on credit provisioning, loan growth, and trading revenue amid heightened macro stress. CEO Jamie Dimon’s tone on tariffs and Fed policy may influence broader financial sentiment. JPM trades at a forward P/E of 12.8, with guidance likely to dictate near-term multiple expansion or contraction.

Source: Seeking Alpha

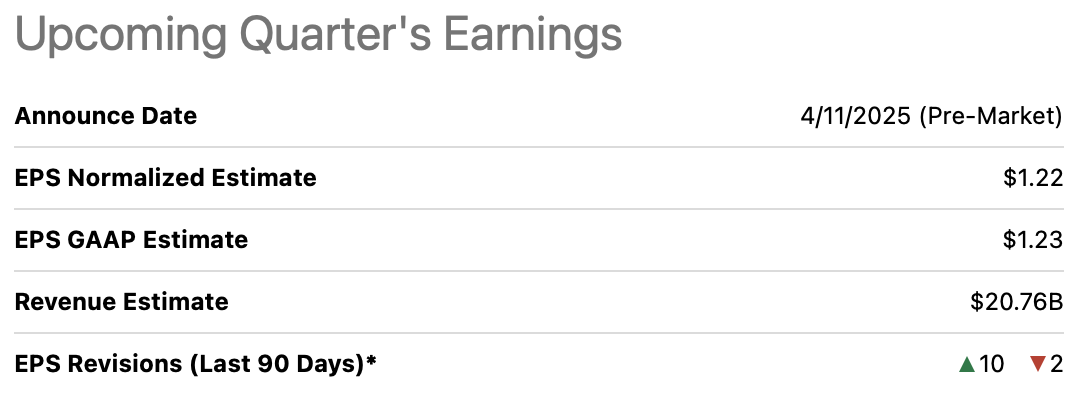

Wells Fargo (WFC) – Reporting April 11 Before to Market Opening

Wells Fargo's regional footprint poses it as a canary in the coal mine for the overall U.S. consumer and middle-market credit landscape. Q1 expectations are muted, and executives see EPS pressure due to increased funding expenses and higher reserves under CECL. Regional loan growth has plateaued and commercial real estate (CRE) remains a slow-brewing risk, so provisioning at WFC can potentially increase again this quarter.

Guidance from management on future lending appetite will be key, as it can determine whether the Fed's crisis measures in terms of liquidity, such as support in the repo market, need to be deployed in weeks ahead.

Investors will be keenly focused on the manner in which WFC is navigating its balance sheet mismatch of duration. Its fixed-income security unrealized losses keep continuing to strain regional banks' capital buffers. Wells stressing mark-to-market pressure or distressed AOCI positions would put further pressure on the market's demands for a Fed policy turn or selective backstops in terms of liquidity.

Wells Fargo enters earnings with muted expectations: FY2025 EPS of $5.79 (+3.5% YoY) and $84.6 billion in revenue. Watch for signals on commercial real estate exposure and deposit retention, which are critical pressure points for regional-heavy lenders. Its modest earnings growth masks risks tied to funding costs and duration mismatches. Trading at 11.4x forward earnings, WFC could re-rate sharply if reserves surprise to the upside or downside.

Source: Seeking Alpha

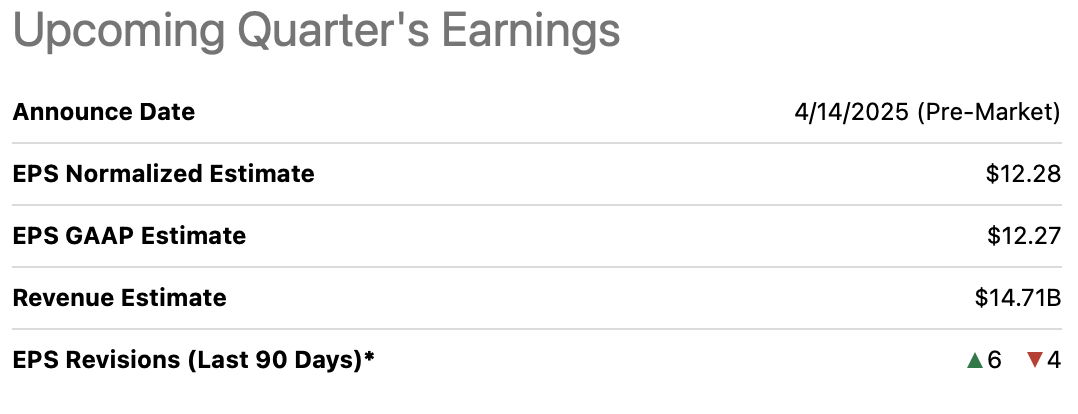

Goldman Sachs (GS) - Reports April 14 Before Market Opening

Goldman Sachs heads into Q1 earnings in an uncommon position for the firm: possibly one of the few banks to gain in the near-term from current turmoil. GS's trading and derivatives desks should have robust numbers due to the volatility spike driven by Trump's tariff announcements and declining Treasury prices. That's one part of the story, however. Investment banking activity is still weak, M&A and IPO pipelines slowed significantly in March, and analysts forecast sequentially decreasing fees, offset in part by wealth management expansion.

And the bigger concern for Goldman, however, is macro: as an indicator of capital markets health, any softness in its fixed income or equities revenue would portend wider cracks. Moreover, GS is unusually reactive to asset repricing and mark-to-market movements. If it reports client deleverage or increased margin calls, it would nudge the Fed toward secret liquidity injections through the repo or discount windows.

Goldman is forecasted to deliver $44.66 in EPS for FY2025 (+10.1% YoY) on $55.9 billion in revenue, supported by trading activity amid recent volatility. While investment banking likely slowed, trading desks may partially offset weakness. Analysts will probe asset management flows and client deleveraging risk. GS trades at 11.6x forward P/E with upside if markets stabilize and M&A pipelines revive.

Source: Seeking Alpha

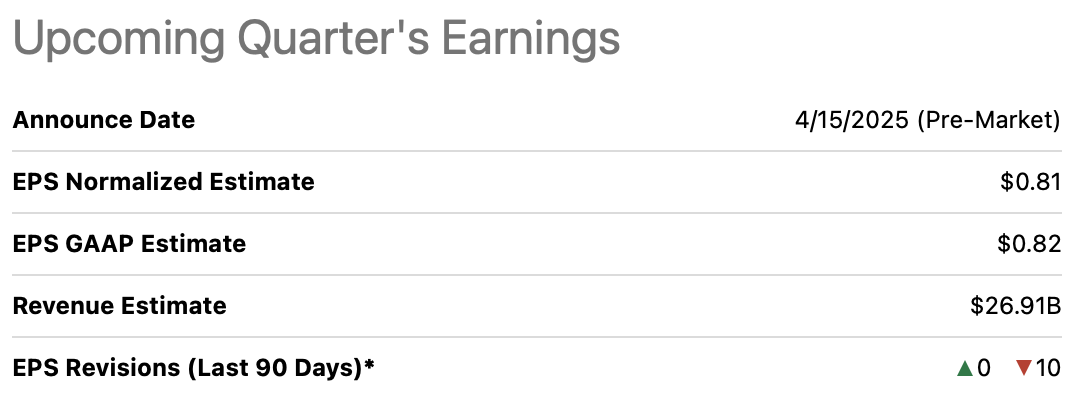

Citi (C) Early Report for April 15th Before Market Opening

Citi’s widespread footprint places it in an unusual position for observation of the overall effect of trade dislocations and capital flows driven by FX. It should see reasonable earnings growth from international consumer strength and increased interest income, while foreign exchange headwinds, and notably those in Asia, have the potential to counteract top-line resilience. Its risk profile in international trade finance exposes it to any deterioration in cross-border activity, and in particular, China's retaliation for U.S. tariffs.

Notably, Citi’s update of cross-border capital flows and interbank liquidity can provide an advance indication of whether dollar funding pressure is intensifying globally. If Citi expects higher cost of funds or use of short-term wholesale funding, this would add to arguments in support of preemptive easing in liquidity conditions, possibly through resuming large-scale repos or halting QT.

Citi is projected to earn $7.40 per share in FY2025, reflecting robust 19.1% YoY growth, with revenues at $83.6 billion. Its international exposure could pressure margins due to FX translation losses and weaker trade finance. However, rising interest income and capital strength may provide a buffer. With a low forward P/E of 8.7, C’s valuation implies skepticism that strong EPS growth is sustainable.

Source: Seeking Alpha

Bank of America (BAC) – Reporting April 15 Pre-Market

Bank of America caps off the bank earnings wave and should report subdued earnings growth. Consumer deposit balances are still healthy, yet BAC has an enormous portfolio of securities that is extremely sensitive to movements in long-duration yields.

With 10- and 30-year risk-free yields spiking in March, BAC might be reporting significant AOCI degradation, which can limit capital flexibility. Similar to JPMorgan, BofA enjoys diversified structure, yet net interest income support from deposit cost inflation is reversing. CEO Brian Moynihan's words carry significant weight. If he indicates rising client pressure, decreased consumer spending, or in-house projections for increased loan losses, this can be taken as an indication that the Fed's "wait and see" approach risks turning out to be an error in its policy. In addition, BAC's prospects for mortgage origination and service will be an in-the-wire update on the reaction of the housing market to rising interest rates, vital for extended macro modeling.

Bank of America is expected to report $3.63 in EPS for FY2025, up 13% YoY, alongside $108 billion in revenue. With large securities exposure, its AOCI losses may be in focus as long-term rates rise. Deposit cost inflation and balance sheet sensitivity remain key risks. BAC trades at a forward P/E of 10.2, with investor attention likely centered on capital ratios and mortgage trends.

Source: Seeking Alpha

Conclusion

Q1 earnings from the top five banks will offer a critical stress test for credit quality, deposit flows, and capital markets resilience. With rising macro volatility and investor anxiety, management commentary may shape expectations around Fed action. These results could either stabilize sentiment, or accelerate calls for liquidity support.