Intel: A New Chapter for an Old Titan

- Intel’s CCG segment generated $8B in Q4 revenue with 38.1% margins, driving AI PC momentum toward 100M units shipped.

- DCAI posted $3.4B in revenue but operating margin dropped to 6.9%, reflecting stiff competition from AMD and Nvidia.

- Intel Foundry earned $17.5B in 2024; a conservative 3x EV/Sales implies ~$50–55B standalone valuation potential.

- Forward P/E at 49.6x and negative ROE of -17.8% highlight Intel’s valuation disconnect amid margin compression risks.

TradingKey - Intel Corporation (INTC), the tried-and-true gold standard for semiconductor leadership, finds itself in the midst of one of the most aggressive company transformations in recent history. Traditionally defined by domination in powering the world’s PCs and servers, Intel today struggles with margin compression, increased competitiveness, and the tech landscape revolutionized by the presence of AI.

Intel's not just tracking the changes in the sector—it's rewriting the playbook itself. Scanning the landscape using foundry strategy, government-sponsored capital support, and all-in-on-next-gen platform wagers on AI, Intel's positioning long-term innovation front and center in the company's DNA. It's no longer about CPUs; it's about owning the compute throughout the stack: xPUs, accelerators, and platform integrations.

Intel replaced the temporary co-CEOs David Zinsner and Michelle Johnston Holthaus with new CEO Lip-Bu Tan in March 2025. Lip-Bu Tan, the former Cadence Design Systems' CEO and Intel director, has semiconductor experience and an innovative background. Intel will make strategic strides in AI and manufacturing in his leadership.

As Nvidia surfs the AI tsunami and AMD sweeps the server wins, Intel's leadership bid hinges on perfect execution and clear value definition. Investors aren't buying the stock—they're buying the turnaround drama with geopolitical connotations and technological significance.

Inside the Intel Engine: Intel's New Business Model Rewired for the Artificial Intelligence Era

Intel's transformation begins in the way the company organizes its enterprise. Historically a vertically integrated design-manufacturing giant, the company first went down the internal foundry path in early 2024 by unbundling chip design (Intel Products) from fab work (Intel Foundry). That internal unbundling makes cost management even more critical, as well as productivity and product development timelines—while setting the company up to open up its capacity to third-party customers such as Qualcomm and Microsoft and even potential competitors.

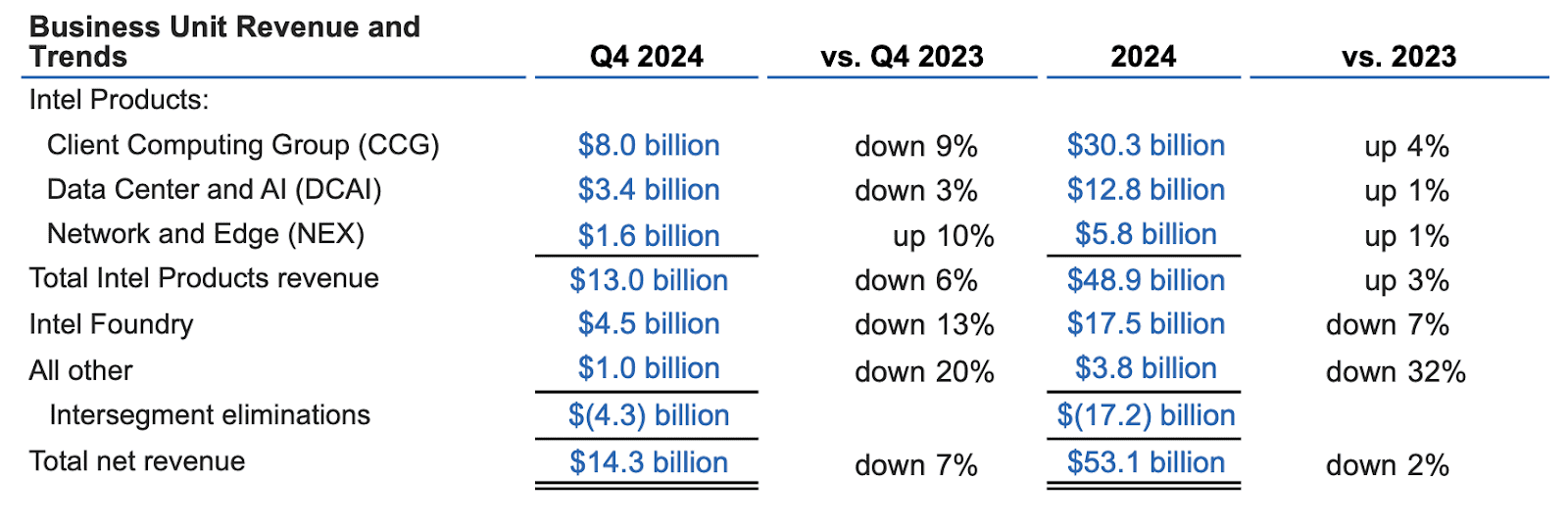

Its main product segment—Client Computing Group (CCG), Data Center and AI (DCAI), and Network and Edge (NEX)—remains the revenue driver for Intel. CCG, which earned revenues worth $30.3 billion in 2024, now spearheads the next computing revolution using AI PCs. Those PCs based on Intel Core Ultra processors and NPUs are revolutionary: taking AI into the hands of the user, on the device. Intel’s ecosystem of over 200 independent software vendors optimizes software for over 400 AI applications—ranging from productivity and creativity to edge AI. Intel anticipates shipping over 100 million such next-generation devices by the year 2025.

Source: Intel’s Earnings Release

DCAI leverages the muscle of Intel Gaudi accelerators and Xeon CPUs. Growth here in 2024 was modest at only 1% YoY, yet there's more momentum in the field of data center innovation. MRDIMM memory advancements and the twin Gaudi-3 servers showcased in collaboration with Dell are examples of Intel’s approach towards reestablishing itself in high-performance AI hardware.

NEX also picks up momentum on the strength of edge installations and 10% YoY Q4 growth. Overall companywide, the company’s vertically stacked product line—ranging from hardware all the way up to middleware—amounts to a strategic hedge against Nvidia’s dominance in the segment for AI accelerators.

The Competitive Chessboard: AMD, Nvidia, and TSMC in the Crosshairs

Intel's comeback occurs at a point where competitiveness reaches a peak. TSMC or TSM is the dominant foundry services company and has enabled Nvidia and AMD to lead Intel in recent years by providing the latest process nodes like 5nm and 3nm.

AMD has taken material server share based on the strength of its EPYC chips manufactured on TSMC's high-efficient manufacturing. Nvidia became a $2 trillion behemoth by dominating the AI software stack—CUDA is all but industry standard. Intel attempts to crack the duopoly via differentiation.

Intel’s foundry approach, backed by U.S. and EU-based facilities, offers a counterbalance to the Asia-based supply chain of TSMC. Governments and purchasers both have national security and resilience interest in Intel’s domestic capacity. Beyond geography, Intel is counting on a technological lead—Intel’s new 18A process node features RibbonFET and PowerVia, architectural innovations that have the potential to outperform FinFET in terms of density and power efficiency.

While Nvidia dominates the workloads for training AI, Intel targets the rest of the AI spectrum: edge, inference, and client applications. Its oneAPI software initiative tries to compete against CUDA by providing a vendor-neutral platform for cross-architecture development. If successful, this would break Nvidia’s developer lock-in and broaden Intel’s reach. Yet software ecosystems are hard to unseat, and AMD is not sitting still either—its acquisition of Xilinx builds out its adaptive computing capabilities, positioning itself well in the data centers and embedded AI. Intel must out-innovate and also compete on cost, dependability, and volume—a triple threat that requires perfect execution.

While AMD has picked up notably—holding over 40% of the client CPU market now following the success of its Ryzen 9000 line—Intel controls the higher share in overall shipments and enjoys deep OEM and enterprise relationships. AMD’s recent pickup resulted from Intel’s delayed Arrow Lake-S introduction and earlier-generation CPU instability that have temporarily changed sentiment. Intel’s road map, featuring the Panther Lake launch on its 18A process, lays the foundation for regaining share based on next-generation performance and power efficiency innovations. Competitive gap bridging continues, but Intel’s scale, ecosystem strength, and upcoming product cycles offer the clear path for regaining ground.

.png)

Source: Puget Systems

Behind the Scenes: Financial Momentum or Illusion?

Intel's balance sheet tells a mixed tale. Revenue for 2024 decreased year-over-year by 2% at $53.1 billion, fueled by macro demand pressures, enterprise inventory digestion, and competitiveness. Gross margin declined dramatically to 36% (non-GAAP), and GAAP operating margin declined all the way down to -22%.

Net losses were at staggering $18.8 billion on a GAAP basis, fueled by restructuring charges and impairments. And the fourth quarter held glimmers of early stabilization: revenue beat by $500 million and EPS came in positive on a non-GAAP basis at $0.13, ahead of expectations.

.png)

Source: Intel’s Earnings Release

Intel's cost discipline begins to become evident. R&D and MG&A expenses declined by 6% YoY in Q4, and the company continues to unleash efficiencies within the Smart Capital strategy. Operating cash flow hit $8.3 billion for the year, and while dividends were suspended on CHIPS Act obligations, this freed up capital for strategic investments. Importantly, Intel's CapEx—largely dedicated to EUV ramp-ups and fab constructions—is funded by over $25 billion in government grants, strategic co-investments, and foundry customer prepayments.

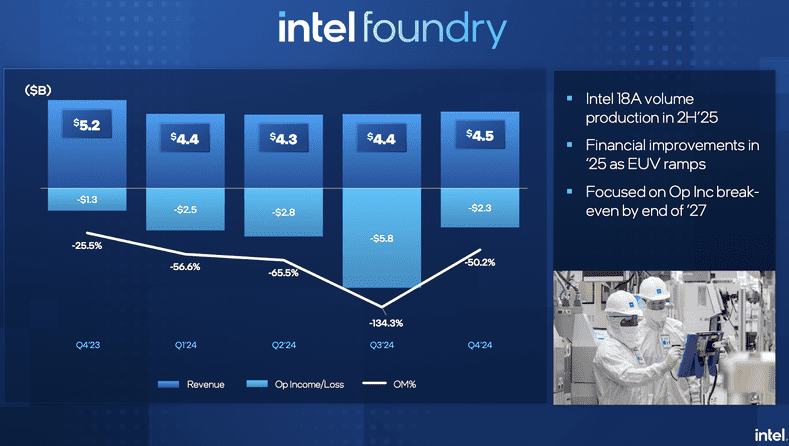

There are growth drivers on the horizon. The AI PC segment that takes off in 2025 has the potential to reaccelerate the top line, while Intel Foundry customer engagements are now translating into full tape-out success in Ireland and advanced package wins.

Meanwhile, production in Fab 52 in Arizona for the 18A process continues towards the ramp in H2 2025. Although Foundry today posts losses, Intel sees breakeven by 2027. If the margin recovers towards the mid-50s and capital intensity slows down post-2025, Intel’s long-term earnings potential may significantly improve.

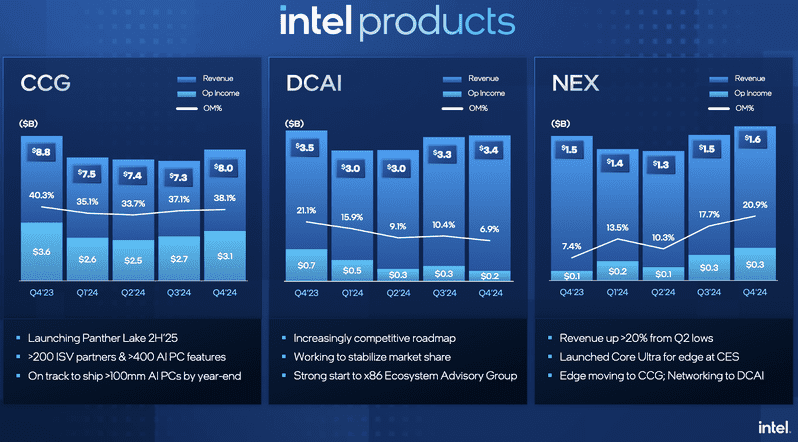

In Q4 2024, Intel’s CCG segment led the charge with $8.0 billion in revenue, up sequentially from Q3, and generated $3.1 billion in operating income with a solid 38.1% margin. This rebound reflects growing traction for AI PCs, backed by over 200 ISV partnerships and a roadmap centered on the Panther Lake launch in 2H 2025. Despite AMD’s share gains, Intel’s scale and roadmap remain competitive.

The DCAI segment posted $3.4 billion in revenue, flat YoY, but operating income fell to $0.2 billion, with margins compressing to just 6.9%. Intel is working to stabilize market share amid fierce competition, with roadmap improvements and the x86 Ecosystem Advisory Group seen as early positives.

Similarly, NEX showed the strongest operating margin expansion, hitting 20.9% on $1.6 billion in revenue. That’s a 23% sequential revenue increase from Q2’s low of $1.3 billion, supported by demand for edge AI applications and the recent Core Ultra launch at CES.

Overall, Intel's product segments reflect stabilization and early signs of turnaround, though margin pressure in DCAI remains a concern. Continued execution across product launches and AI integration will be crucial in 2025.

Source: Intel’s Q4 Earnings Presentation

Valuation: Justifiably Punished or Substantially

Intel looks expensive based on forward P/E—49.6x against the sector median of 21.9x. That artificially high figure hides repressed earnings and one-off expenses that mask the company’s true ability to produce cash. Based on the price-to-sales measure, Intel’s valuation at just 1.96x (forward) is around 30% below the sector average—reflecting the market not yet having fully discounted the recovery. At 9.83x forward EV/EBITDA, which is at a modest premium to TSMC but well below the astronomical 30x+, the expectations around profitability differ.

A sum-of-the-parts valuation unlocks hidden opportunity. Intel Foundry earned $17.5 billion in revenue in 2024—if one applies a conservative valuation multiple of 3x EV/Sales, by itself it would be worth between $50–55 billion. CCG, DCAI, and NEX combined earned just less than $49 billion. If one values these companies at 2–3x EV/Sales, that's another $100–140 billion in enterprise value. Add in Mobileye and Altera, and Intel's break-up valuation far exceeds its current market capitalization (~$135B as of March 2025).

Source: Intel’s Q4 Earnings Presentation

A DCF based on mid-teens revenue growth, long-term margin restoration to the 20–25% level, and normalized FCF yield of 5% suggests fair value in the $55–65 range—some 30–50% above where the stock is today. That said, this potential upside rests on flawless execution, foundry customer wins, and margin restoration companywide. Meanwhile, Intel will remain a battleground stock, trading at a discount to peers but with significant optionality priced in.

Stormy Weather Ahead: Assessing the Dangers Facing Intel's Turnaround

Intel's strategic ambitions are matched by the threats that have the potential to derail them. Intel is undertaking transformation at the very same time that there are intense macro and competitive pressures. Failure in execution on Intel 18A and foundry commercialization are two of the most critical threats. Manufacturing yields issues, equipment slippage, or absent third-party customer timelines have the potential to kill credibility. The semiconductor world does not have room for errors—miss one node or have one bad ramp and the customer base disappears, and reputation damage is hard to recover from.

Its foundry model itself is capital-hungry and dilutive in the early years. Intel's Ohio, Arizona, and Ireland factories require massive investments that only become economical at scale. If third-party customer demand does not materialize—specifically hyperscalers—ROI profile will take the hit. Adding to the risk are Intel's Smart Capital transformation and reliance on CHIPS Act funds that introduce political uncertainties.

Any U.S. industrial policy changes or CHIPS enforcement changes would curtail access to capital and disrupt fab expansions. From the balance sheet perspective, Intel has suspended dividend payments, high levels of debt, and negative GAAP earnings. Cash flow remains positive, though there's little room for error in financing long-term projects without dilution or further leverage.

Competitive risk also continues to accrue—Nvidia's domination in AI hardware, AMD's success in servers, and Apple's vertical integration in client computing all nibble away at Intel's established leadership. And finally, geopolitical events—uncertainty in Israel, U.S.-China tension, or Europe's glacial regulatory processes—potentially bring unforeseen disruptions into fab production or foundry customer relationships.

Final Take: A Value Play with Strategic Optionality

Intel is taking on a high-reward, high-risk approach that would establish the company's legacy. While the near-term fundamentals are messy, the company’s long-term story—based on AI compute, US-based production, and vertically integrated foundry strategy—is robust. To patient investors, this is not just a turnaround. It’s silicon sovereignty moonshot, democratization of compute, and leadership in AI hardware.