Sea Ltd Stock: Higher Projected 2025 Sales Sees Shares Jump 7%

TradingKey - For investors in Asia focused on e-commerce stocks, betting on the big operators and platforms that have scale tends to be the most astute strategy.

Within the Southeast Asia region, Sea Ltd (NYSE: SE) dominates the e-commerce landscape via its Shopee platform that has seen considerable growth during the pandemic and continues to scale post-pandemic too.

There were relatively high expectations heading into Sea’s earnings but the company didn’t disappoint. Sea Ltd released its Q4 2024 results before the market open on Tuesday (4 March) and shares ended the trading day up 7%.

Here’s what Sea investors, and Asian tech investors alike, should know about the company’s latest results.

Shopee posts better-than-expected growth

While Sea Ltd does operate a big gaming platform and a nascent digital financial services business, Shopee (or e-commerce) remains its biggest revenue component.

And growth at Shopee impressed investors. Overall, Sea posted revenue of US$5 billion in Q4 2024, up 36.9% year-on-year and coming in ahead of the consensus estimate of US$4.84 billion in revenue for the period.

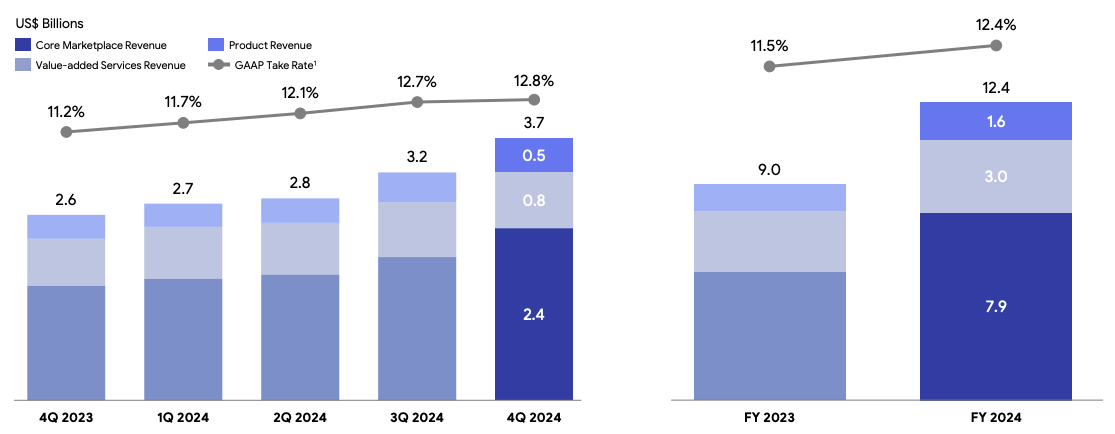

This impressive growth was driven primarily by Shopee, where revenue surged 41.3% year-on-year to US$3.7 billion for Q4 2024, up from US$2.6 billion in Q4 2023. That also beat analysts’ expectations for growth of Sea’s e-commerce platform.

Shopee revenue and take-rate

Source: Sea Ltd Q4 2024 earnings presentation

As for orders, gross orders hit a landmark of 3 billion for Q4 2024, up from 2.5 billion in Q4 2023, while gross merchandise value (GMV) hit US$28.6 billion during the quarter – up 23.5% year-on-year from the year-ago quarter.

Encouragingly, Sea’s profitability continued in Q4 2024 as the company posted net income of US$237.6 million for the period, reversing a loss of US$111.6 million for the same period in 2023.

Guidance for Shopee impresses

What drove a lot of optimism among investors was Sea Ltd’s management’s guidance that Shopee’s GMV will hit US$120.6 billion for the whole of 2025, up a robust 20% year-on-year from the US$100.5 billion in GMV recorded for 2024.

That also topped average analysts’ estimates for around US$117 billion in GMV for 2025. This boost has been driven by Sea starting to pull away from ByteDance’s TikTok and Lazada of Alibaba Group Holding Ltd (HKEX: 9988) (NYSE: BABA) in the region’s fiercely-competitive e-commerce landscape.

The strong increase in 2024 sales for Shopee was largely attributed to the platform operator steadily raising commissions (or the take-rate) that it charges its merchants in core markets.

These hikes bring its fee structure to a much higher level than its rivals but Shopee remains confident that it can attract and retain merchants on its platform given the broad user base in the region as well as established and reliable delivery services.

TradingKey analyst Petar Petrov said:" Three years ago, Sea’s operation suffered a lot due to headwinds in the gaming business, increased competition in e-commerce and over-expansion. However, in the last year, the management did a good job stabilizing the operations, solidifying its market share in Southeast Asia and taking a more conservative approach towards marketing spending and expansion." -- Sea Limited Delivers Strong Q4 Results – Can the Growth Momentum Continue?

What about Sea’s gaming and financial services?

The other two business units of Sea – its gaming and digital financial services arms – both managed to notch up growth.

The gaming business (Garena), which is driven by the wildly-popular Free Fire mobile game, saw revenue of US$519.1 million for Q4 2024 and this happened to be its first quarter of revenue growth since early 2022. Meanwhile, bookings for its gaming business hit US$543.2 million for the quarter, up a healthy 19% year-on-year.

On the digital financial services side, revenue came in at US$733.3 million, representing a robust 55.2% year-on-year expansion. The business’s loan book was US$5.1 billion as of the end of 2024, up 63.9% year-on-year from the loans outstanding as of the end of 2023.

Overall, it was another solid quarter from Sea Ltd and its cash pile continues to grow as it maintains profitability. As of the end of 2024, Sea’s cash position entered double digits as it hit US$10.4 billion – up from the US$8.7 billion for the end of 2023.

Investors will be impressed with Sea’s latest earnings and, if the company can continue to see its Shopee platform scale profitably both in terms of revenue growth and take-rate, then there certainly could be more upside this year and next.