[IN-DEPTH ANALYSIS] Oracle (ORCL): Big Ambitions but Difficult Reality

Key Points

- Oracle is one of the biggest legacy providers of data solutions, offering a wide range of services including databases, ERP and CRM software products, as well as data management solutions.

- Currently the company is focusing on developing their cloud business, as this is already the main driver of its revenue growth

- Despite the solid growth in the recent years, the Oracle cloud may face a risk of underinvesting due to the low cash reserves and significant debt

- The generous dividend consumes a large amount of the net income, preventing the company from further investing in growth

- The company is currently overvalued compared to its peers, but there might be positive developments from the partnership with Meta, Project Stargate and the TikTok legal case

Business Description

Oracle has been a leading data company for more than 40 years. Oracle offers a wide range of products and services, including, but not limited to, relational and non-relational databases, cloud in the form of IaaS, PaaS and SaaS, enterprise applications related to resource planning (ERP), supply chain management (SCM), customer relationship management (CRM), business intelligence and data security and governance solutions.

Oracle was one of the first companies to introduce the concept of relational databases in the business world. Its early innovations laid the foundation of the modern database technologies.

.jpg)

Source: SEC Filings, TradingKey

Revenue Segmentation

Source: SEC Filings, TradingKey

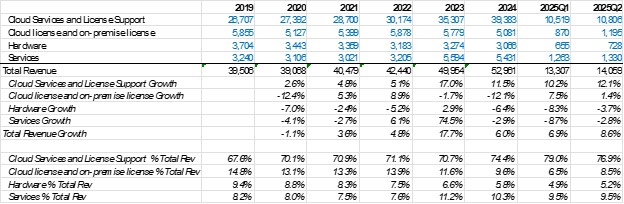

Oracle's revenue model is a blend of subscription-based and traditional sales-based services, categorized into four main segments:

Cloud Services and License Support: This is the largest segment, representing nearly three-fourths of the total revenue. The segment includes all the recurring revenue from the cloud business (e.g. customers paying subscriptions to IaaS, PaaS and SaaS products) and the license business (e.g. annual fees for updates, maintenance and technical support for the Oracle software).

Cloud and On-Premises License This includes the revenue from the initial deployment of cloud services and software, which happens on the client’s premises. Unlike the upper segment, this segment encompasses only the one-time sale of the respective products and it usually represents around 10% of the total revenues.

Hardware: Oracle sells hardware such as servers and storage systems. This is a legacy business and its portion of the total revenue gradually decreases.

Services: These are the add-on services related to Oracle’s software and cloud, such as consulting, client education, training and certification.

Source: SEC Filings, TradingKey

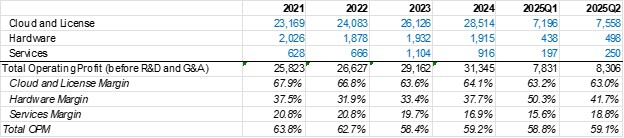

In terms of profitability, the picture becomes even more skewed in favor of cloud and license, as these two businesses contribute around 90% of the operating profit due to the larger margins compared with the other revenue streams.

Cloud Ambitions Face Complex Debt Situation

Source: SEC Filings, TradingKey

Oracle holds a 3% market share of the total cloud industry, making it the sixth largest cloud provider after AWS, Microsoft, Google, Alibaba and Salesforce. Oracle's cloud business is currently growing at a very high rate of over 20%. Despite its growth, Oracle's market share is not expected to threaten the top three players.

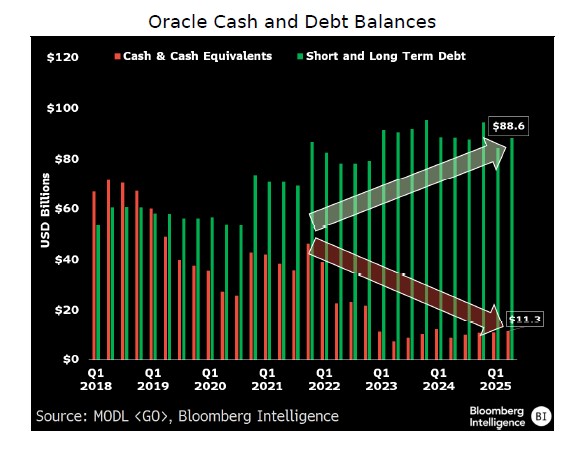

Oracle is in a much less advantageous situation when it comes to cash reserves, levels of debt and operating cash flows. First, in the last six years, Oracle's cash reserves have shrunk, while its total debt has significantly increased. This is a stark contrast to the other major cloud players, as they have much larger cash reserves and an insignificant amount of debt.

Source: Bloomberg Intelligence

Source: SEC Filings, TradingKey

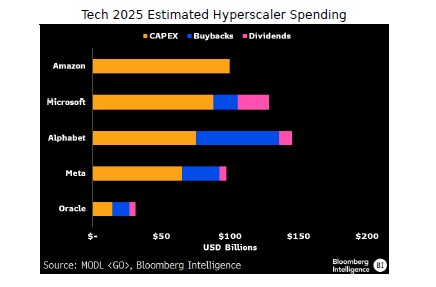

Second, Oracle generates healthy cash flow due to its high-margin business, with $20 billion in operating cash flows. However, this amount is quite modest compared to the amount that Google and Microsoft bring in. The combination of a weaker balance sheet and less cash flow implies Oracle’s projected capex will be way lower than its peers.

Source: Bloomberg Intelligence

Source: SEC Filings

For the fiscal 2025, Oracle has to repay $10.6 billion in bond maturities. This amount looks quite big, but the high-margin nature of the business allows Oracle to generate enough cash flow to prevent the company from becoming insolvent. However, the high amount of debt can have two negative consequences: 1) Oracle is forced to pay hefty interest payments (over $3 billion per year) and 2) limited ability to spend more on capex due to the need to settle the maturities of the debt.

Ownership Structure May Hinder Future Potential

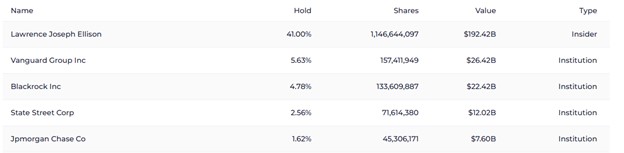

It is worth noting that 41% of the ORCL shares are owned by Lawrence Ellison, one of the founders of the company and the fifth richest person in the world.

Source: SEC Filings

Oracle also has a generous dividend policy with a dividend payout ratio of around 40%. As the largest shareholder, Ellison is also the largest beneficiary of the Oracle dividend policy, which implies that Ellison is using Oracle to pay dividends himself.

Source: SEC Filings, TradingKey

While a generous shareholder return policy is often viewed positively, it is typically suitable for companies in a mature, low-growth stage. By returning nearly 40% of its profit to shareholders, rather than reinvesting it in growth opportunities, Oracle is prioritizing short-term benefits for current investors.

If Oracle aspires to be a leader in a lucrative high-tech industry like cloud computing, it should invest as much as possible now; otherwise, it will trail behind the competition.

What Can Go Right for Oracle?

Oracle has several potential opportunities that could impact its business in a positive way.

Partnership with Meta

Meta, one of the major AI scalers, is putting significant efforts into developing its own series of language models – Llama. They have chosen Oracle to be the second cloud provider alongside AWS. From Meta’s perspective, Oracle is a good alternative to AWS, as the latter can be seen as a direct competitor in AI.

From Oracle’s perspective, the deal with Meta will give an extra revenue runway for their growing cloud business.

TikTok deal

Oracle is one of the candidates to take over the US-based operations of TikTok in case ByteDance (the Chinese parent of the app) is forced to give up its business in the US. Oracle currently manages TikTok US user data, ensuring security and privacy.

If the deal materializes, this will significantly transform the business model of Oracle by bringing a portion of a new revenue, as well as enhancing its AI capabilities with the data from the short-video app.

Stargate Project

The Stargate Project is a significant initiative aimed at advancing artificial intelligence (AI) infrastructure in the United States. Announced in early 2025, it is a joint venture involving major players like Oracle, OpenAI, SoftBank and Nvidia, with a planned investment of nearly $500 billion over the next four years. Oracle will contribute a small portion of funds worth 7 billion.

There are a number of benefits for Oracle from this project including acquiring more business and know-how, forging strategic partnerships and benefiting from the investment return.

Valuation

Currently, ORCL shares are trading at slightly over 40 times the trailing P/E ratio, with expected growth of 10% in 2025.

Considering that Oracle has a much smaller market share in cloud and a much weaker balance sheet than the above-mentioned peers, the high multiple is not justified.

However, there is a certain optimism surrounding Oracle’s recent moves, including the Meta partnership, the potential TikTok deal and the Stargate project – any of which could be a game changer for the company.