Nvidia Stock Drops Post-Earnings, But Analysts Remain Bullish—Here’s Why

Nvidia Corp. (NVDA), the leading chipmaker at the center of the artificial intelligence (AI) spending boom, reported solid but not spectacular quarterly earnings, disappointing investors accustomed to blockbuster results.

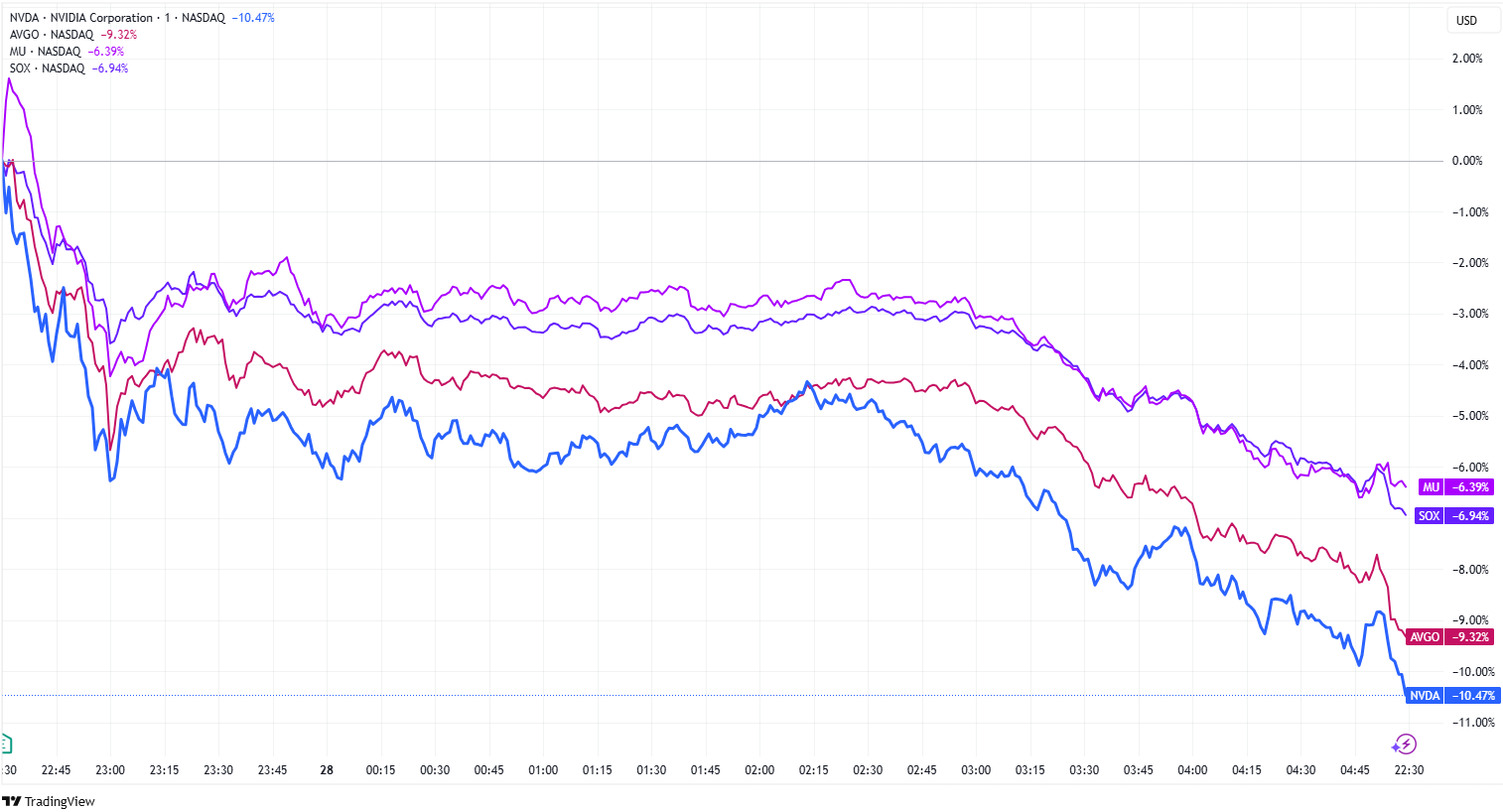

On Thursday, Nvidia’s stock closed down more than 8%, marking its worst single-day decline this year, with its year-to-date losses exceeding 10%. The sell-off also weighed on other chipmakers, with Broadcom (AVGO) and Micron (MU) each dropping over 6%, while the Philadelphia Semiconductor Index (SOX) declined 6%. These shares continue to decline in after-hours trading.

Source: TradingView; NVDA, AVGO, MU and SOX Stocks Performance on Thursday

Meanwhile, a trader placed a significant bearish bet, purchasing over 300,000 put option contracts wagering that Nvidia’s stock would fall to $115 by March 7—implying a 12% decline from Wednesday’s close. According to Bloomberg data, this bearish trade drove Nvidia’s put option trading volume to more than double its 20-day average.

Investor sentiment took a hit due to concerns over gross margins and potential tariff risks after earnings release. Nvidia disclosed that aggressive efforts to launch its new Blackwell chip architecture would lead to near-term margin compression In its earnings call. Additionally, CEO Jensen Huang acknowledged the challenges Nvidia faces in China, indicating that revenue from the region has declined by about half. The possibility of U.S. tariffs further impacting Nvidia’s business in China also weighed on investor confidence.

The emergence of Chinese AI startup DeepSeek has disrupted one of Wall Street’s strongest narratives: that developing AI requires massive investments in computing power and infrastructure—areas where Nvidia dominates. DeepSeek claims its AI models achieve performance comparable to leading U.S. models while requiring significantly fewer chips and computing resources.

"DeepSeek opened our eyes to the fact that Nvidia is not invincible," said Shana Sissel, Chief Investment Officer at Banrion Capital Management.

Adding to market concerns, TD Cowen reported that Microsoft has begun canceling substantial data center capacity leases in the U.S., highlighting fears that companies may be overbuilding AI infrastructure beyond long-term requirements.

Despite concerns about potential deceleration in AI-related spending, Nvidia’s major customers—including Microsoft, Amazon, Alphabet, and Meta Platforms—have reaffirmed or significantly increased their capital expenditure plans this earnings season. This suggests they are not yet prepared to scale back purchases of Nvidia products.

Wedbush analyst Dan Ives expects the combined capital expenditures of these "Magnificent Seven" tech giants to reach $325 billion this year, with a substantial portion directed toward AI infrastructure investments.

According to Bloomberg, analysts estimate that expectations for Nvidia’s 2026 net income have remained stable, while revenue projections have edged up by approximately 2%, suggesting that concerns over DeepSeek or broader industry headwinds have not significantly impacted Wall Street’s outlook on the company.

Huang argued that DeepSeek’s approach could actually bolster demand for Nvidia’s products. He explained that DeepSeek relies on fine-tuning, which requires more frequent computing sessions than traditional one-time AI training, potentially increasing long-term computing needs.

Despite recent stock volatility, BofA Securities reaffirmed Nvidia as the "dominant leader" in AI, spanning initial and specialized training, inference, and robotics applications, making it a preferred investment choice.

Moreover, Nvidia currently trades at a forward price-to-earnings (P/E) ratio of 27x—lower than Apple’s 32x, despite Nvidia’s significantly higher growth trajectory. Apple’s latest quarterly revenue grew just 4%, whereas Nvidia’s growth rate is roughly 20 times faster, making its current valuation appear relatively "cheap." Nvidia is now priced at just 20x its projected 2026 earnings—among the lowest multiples within the Magnificent Seven tech giants.

While trade policy remains a key risk for Nvidia this year, Barron’s noted that investors should focus on the company’s strong fundamentals. As Nvidia prepares to launch Blackwell and capitalize on accelerating AI demand driven by AI agents, inference workloads, and multimodal models, its growth outlook remains robust.

Looking ahead, Nvidia’s stock could regain momentum with three major catalysts expected in mid-March during its annual GTC conference: the announcement of a new Rubin product line, advancements in autonomous robotics solutions, and Nvidia’s expansion into quantum technologies.

"With a solid quarter behind us, investor focus now shifts to GTC in mid-March, which we expect to serve as a catalyst for the stock," wrote Rosenblatt analyst Kevin Cassidy. "We anticipate updates on Nvidia's technology roadmap and new AI inference use cases to drive further excitement."

According to Tipranks, 94.29% of Wall Street analysts have a Buy rating on Nvidia, with an average price target of $179.13, representing a 36% upside from the latest closing price.