Walmart Stock Drops 6% After Q4 FY2025 Earnings: 5 Key Takeaways for Investors

TradingKey - The US consumer has remained strong over the past few years, despite higher inflation and higher interest rates. That may have surprised some market watchers but certain listed companies have cashed in on this strength in the US consumer.

Indeed, investors had high hopes heading into the latest Q4 FY2025 earnings from big box retailing giant Walmart Inc (NYSE: WMT) on Thursday (20 February). The retail behemoth delivered better-than-expected revenue and earnings per share (EPS), showing resilience in a challenging consumer environment.

However, Walmart’s guidance for the year ahead left Wall Street wanting more, sending shares sharply lower during the trading day on Thursday. So, is this a case of short-term market jitters, or should investors take a closer look at Walmart’s long-term trajectory?

Here are the five key takeaways from the latest earnings report from Walmart.

- Strong quarter but slower growth ahead

Walmart delivered another solid quarter, with revenue coming in at US$180.6 billion, slightly ahead of Wall Street’s expectations of US$180.0 billion.

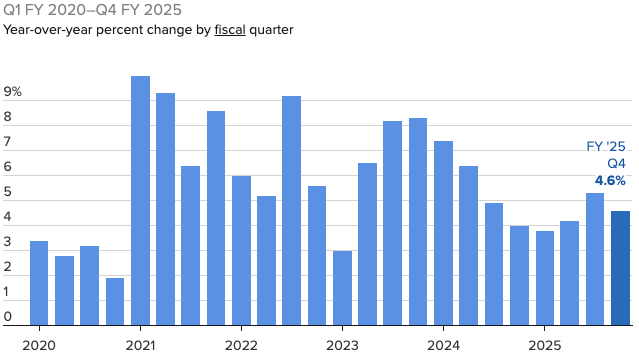

The company also beat earnings estimates, reporting adjusted EPS of US$0.66, compared to the expected US$0.64. Comparable sales in the US climbed 4.6%, marking yet another quarter of steady consumer demand.

Walmart US same-store sales growth

Sources: CNBC, company reports

One of the biggest highlights was Walmart’s continued success in e-commerce. Online sales in the U.S. surged 20% year-on-year, extending an impressive 11-quarter streak of double-digit growth.

This consistent performance underscores Walmart’s ongoing digital transformation and its ability to capture more online shoppers, particularly through in-store pickup and home delivery services.

- Wall Street didn’t love Walmart’s guidance

Despite delivering strong results, Walmart’s outlook for the current fiscal year didn’t sit well with investors. The company expects revenue growth of just 3% to 4%, a step down from last year’s 5.6% increase.

Similarly, adjusted operating income is projected to rise 3.5% to 5.5%, a notable slowdown from the 9.7% gain recorded in the prior fiscal year.

Adding to the disappointment, Walmart forecasted full-year EPS between US$2.50 and US$2.60, falling short of the consensus estimate of US$2.76. This more measured outlook was attributed to several factors, including macroeconomic uncertainty, the potential impact of new tariffs on imports from Mexico and Canada, and costs related to its US$2.3 billion acquisition of smart TV company Vizio.

While the company remains optimistic about its long-term trajectory, investors had been hoping for a more aggressive growth forecast, which led to the post-earnings stock drop.

- Tariff risks loom large for Walmart

Walmart’s CFO, John David Rainey, addressed concerns about potential tariffs on Mexico and Canada, warning that while the company is well-positioned, it won’t be completely insulated from their impact.

Although two-thirds of Walmart’s products are sourced domestically, any increase in import costs could weigh on profit margins, particularly in key categories like fresh produce and general merchandise.

That said, Walmart has navigated tariff challenges before (during President Trump’s first term in office) and intends to deploy similar strategies this time around. The company plans to work closely with suppliers, shift sourcing where possible, and lean into private-label brands to mitigate cost pressures.

However, with uncertainty around whether – or when – tariffs will be implemented, Walmart chose not to factor them into its guidance. That added another layer of unpredictability for investors.

- E-Commerce and membership growth drive higher margins

Walmart has increasingly diversified its revenue streams beyond traditional retail, and those efforts are starting to pay off in a big way. The company’s higher-margin businesses – advertising, membership programmes (Walmart+ and Sam’s Club), third-party marketplace, and fulfillment services – all saw strong growth in the latest quarter.

Global advertising revenue jumped 29%, with Walmart Connect in the US rising 24%. Meanwhile, Sam’s Club saw a 6.8% increase in comparable sales, fuelled by a 16% rise in membership income. Walmart+ and Sam’s Club members are proving to be valuable long-term customers, driving repeat purchases and increasing store visits.

Additionally, over 30% of Walmart’s customers are now paying extra for faster delivery options, helping to improve e-commerce profitability. The company has also expanded same-day pharmacy delivery, which not only adds convenience but also drives larger basket sizes as customers bundle prescriptions with other purchases.

- Dividend boost from Walmart highlights confidence

While Walmart’s growth forecast was more cautious than expected, the company still sent a strong message to investors by raising its dividend by 13% – its biggest increase in more than a decade. This move underscores Walmart’s confidence in its long-term cash flow and ability to return capital to shareholders.

Despite short-term concerns, Walmart’s underlying business remains strong. Its ability to gain market share, expand e-commerce operations, and grow high-margin revenue streams suggests it is well-positioned for the future, even if near-term challenges – like tariffs and macroeconomic uncertainty – keep the stock volatile.

Bottom line: A buying opportunity?

Walmart remains a retail powerhouse with strong fundamentals, but the stock’s reaction shows how high expectations were. With shares down over 6%, long-term investors may see this as an opportunity to scoop up a reliable blue-chip stock at a discount.

The company’s growing e-commerce business, expanding high-margin revenue streams, and consistent market share gains make it a strong player in any market environment.

However, investors will need to be comfortable with the potential impact of tariffs, a slower growth outlook, and macroeconomic uncertainty before making their move to invest.