Amazon 2025: Retail Strength, Cloud Dominance, and AI-Powered Growth

Key Takeaways

- Retail Resilience: Retail remains a core driver of revenue, with strong performance in North America.

- AWS and AI Leadership: AWS continues to demonstrate robust growth and healthy margins, supported by advancements in AI infrastructure and proprietary technologies like Trainium.

- Valuation Upside: Base case valuation of $245, with potential upside to $310 driven by AWS growth and broader AI adoption.

Amazon’s 2024 performance reflects its resilience and adaptability across its core businesses: Retail, Cloud Services (AWS), Advertising, and Subscriptions. By leveraging innovation, operational efficiencies, and strategic investments, Amazon has sustained its leadership in e-commerce, while rapidly expanding its presence in high-margin segments like cloud computing and advertising.

Source: Amazon, Tradingkey.com

Retail: The Cash Cow Driving Stability

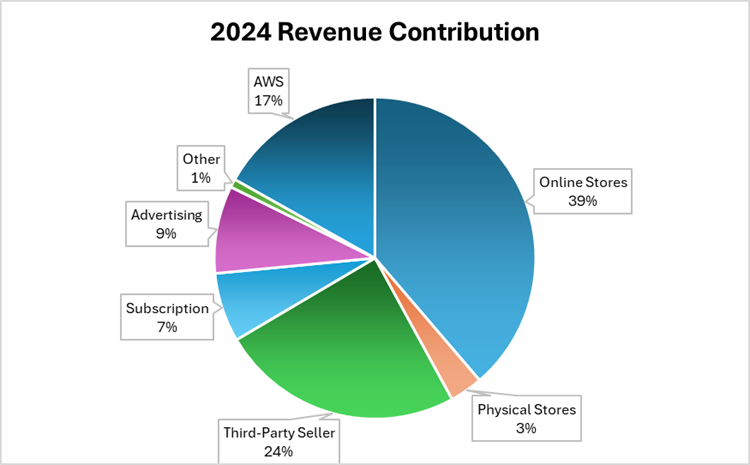

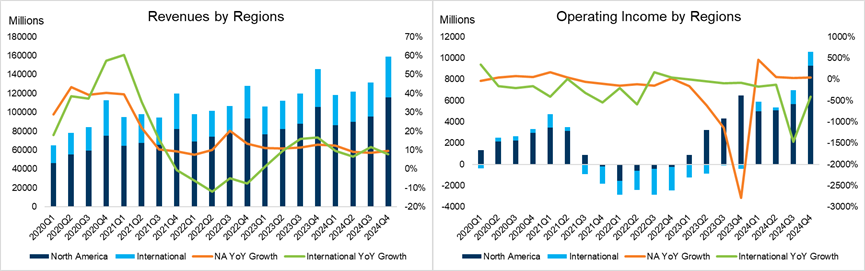

Amazon’s Retail segment remains the backbone of its business, contributing 66% of total revenue through Online Stores, Physical Stores, and Third-Party Seller Services. In 2024, the retail business demonstrated robust performance across North America and International markets, supported by operational efficiencies and strong consumer demand.

North America

- Revenue Growth: Revenue increased 10% year-over-year, reaching $387.5 billion.

- Profitability: Operating income surged 68%, hitting $24.97 billion, with operating margins expanding to 10.8%.

- Drivers: A strong U.S. consumer market and AI-powered cost optimizations significantly boosted profitability.

International

- Revenue Growth: Revenue grew by 9% to $142.9 billion.

- Profitability: The segment achieved positive operating income for the first time in years, driven by higher unit sales and increased advertising revenue.

- Drivers: Many countries are recovering from economic downturns.

Source: Amazon, Tradingkey.com

Subsegment Performance

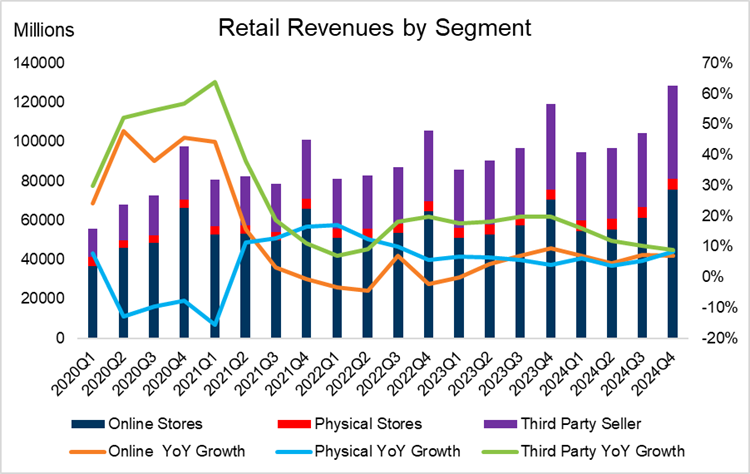

- Online Stores: Amazon achieved a 7% year-over-year sales growth, with record-breaking holiday season performance. U.S. Prime shipments rose 65% compared to the previous year, showcasing strong consumer engagement.

- Third-Party Sellers: Contributing 24% of total revenue, this segment grew by 11% in 2024, with the holiday season driving record sales.

- Offline Expansion: Physical stores, while accounting for just 3% of revenue, saw new initiatives like Amazon Go and Whole Foods partnerships with brands like Clinique and Armani Beauty to enhance the in-store experience.

Source: Amazon, Tradingkey.com

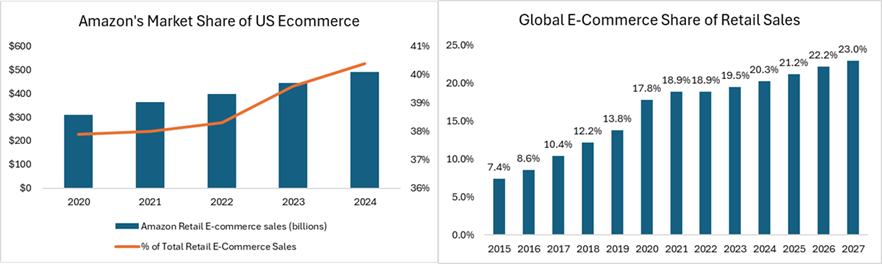

Market Share

Amazon commanded approximately 40% of the U.S. e-commerce market in 2024, with projections of 40.9% by 2025. However, e-commerce only occupies 20% of total retail sales, signaling significant growth potential in broader retail.

Source: EMarketer, Statista, Tradingkey.com

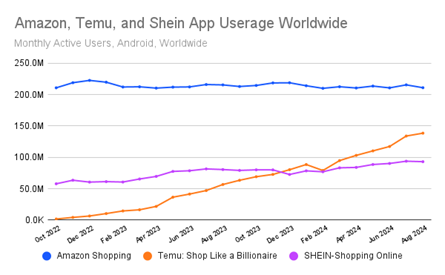

Competition

Amazon operates in a highly competitive landscape, facing challenges from established players and emerging disruptors in specific segments.

- Established Competition: Walmart continues to expand its delivery services, targeting higher-income demographics. The company’s focus on convenience and competitive pricing has driven strong growth in this segment.

- Emerging Players: Platforms like Temu and Shein are gaining traction, particularly in the fashion and ultra-low-cost retail categories. While Amazon maintains its leadership, Temu is quickly catching up with aggressive pricing strategies.

Source: SimilarWeb

Amazon’s Competitive Edge

- Price Leadership: Amazon’s products are, on average, 14% cheaper than competitors, according to Profitero. This pricing advantage reinforces its value proposition across categories.

- Policy Shifts: The 2025 U.S. policy change eliminating the $800 import exemption could benefit Amazon by reducing the pricing advantage enjoyed by competitors like Temu and Shein, who rely on low-cost imports.

- Global Expansion: The anticipated launch of Amazon Ireland in 2025 will expand Amazon’s global marketplaces to 22 countries, increasing its international footprint and consumer reach.

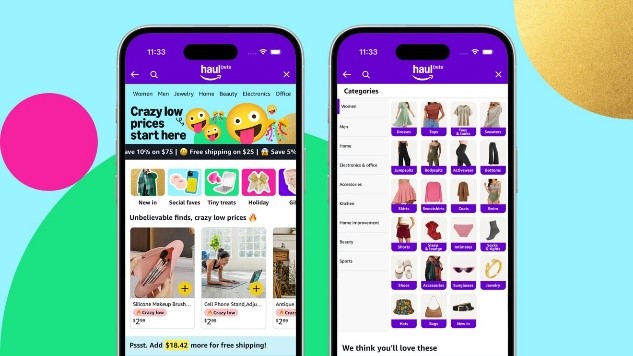

Amazon Haul

In Q4 2024, Amazon launched Amazon Haul, a new feature exclusive to its U.S. mobile app. This initiative targets the ultra-low-price retail segment dominated by players like Shein and Temu.

- Target Audience: Budget-conscious consumers seeking affordable clothing, home goods, lifestyle products, and electronics, all priced under $20.

- Key Features: Free shipping on orders over $25, though purchases under this feature are not eligible for Prime benefits.

- Future Prospects: While performance data is not yet available, Amazon Haul’s success will likely depend on its ability to attract and retain price-sensitive customers in a highly competitive segment.

Source: Amazon

Amazon's Haul strategy aims to offset lower margins on individual items with higher sales volumes, potentially maintaining or boosting profitability if volumes are significant. Currently, 60% of Amazon's retail sales are from third-party (3P) sellers, where Amazon earns through commissions and fees, and 40% are first-party (1P) sales, where Amazon profits from product markups. Haul might increase this 3P share by attracting more sellers to use Amazon's logistics. The increase in tariffs could benefit Amazon because it can diversify its sourcing, such as purchasing from Southeast Asia, thereby reducing reliance on countries with high tariffs and lowering overall procurement costs, and meanwhile making 3P sellers more dependent on Amazon's FBA services, impacting the operating margin in a mixed way: lower margins from Haul might be offset by higher volumes, FBA dependency, and tariff-induced pricing adjustments.

Personalized Shopping Experiences

To enhance customer engagement, Amazon has invested heavily in AI-driven personalization:

- AI Shopping Guides Rufus: These tools provide tailored product recommendations, improving the decision-making process for consumers.

- Immersive Technology: Amazon is exploring AR/VR technologies to offer immersive shopping experiences, particularly in fashion and home decor.

Amazon's retail e-commerce margins are likely to be stable to slightly increased over the medium term, with potential for more growth long-term if its strategies in volume growth, operational efficiency, and revenue diversification prove successful.

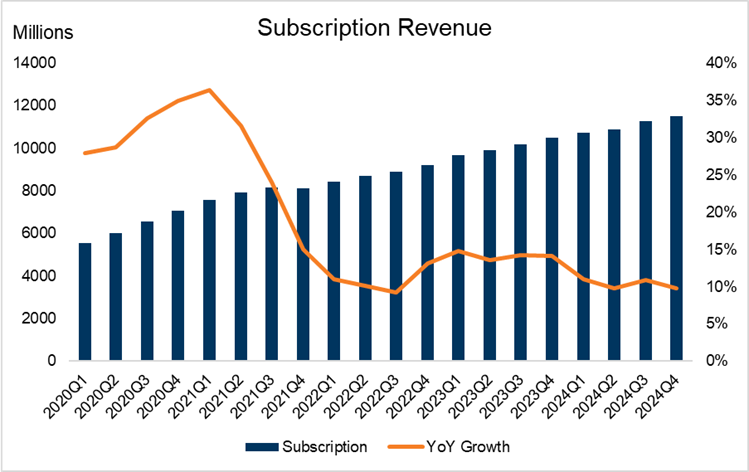

Subscription: A Stable Revenue Stream

Amazon Prime remains a cornerstone of Amazon's business, delivering consistent and reliable income through its diverse offerings, such as expedited shipping, healthcare services, and entertainment (including music, video streaming, e-books, and gaming). In 2024, Prime subscription revenue grew by 10%, reaching $44 billion. U.S. members saved an average of $500 annually on delivery fees, reinforcing the strong value proposition of Prime’s bundled services.

Source: Amazon, Tradingkey.com

Logistics Efficiency

Prime’s success is underpinned by Amazon's industry-leading logistics capabilities. Over the past two years, Amazon has significantly reduced global per-unit service costs through strategic network redesigns. A 40% improvement in U.S. inventory placement efficiency before Black Friday helped drive an 86% year-over-year increase in operating income for the subscription business.

Delivery Network Expansion

Amazon expanded its same-day delivery network by more than 60% in 2024, now covering over 140 metropolitan areas. This expansion enabled the company to handle more than 9 billion units for same- or next-day delivery, enhancing Prime’s appeal while optimizing costs.

Automation and Robotics

Amazon has further strengthened its logistics infrastructure with the integration of robotics and automation. These advancements have reduced costs, increased productivity, and improved safety, helping Amazon maintain its promise of fast and reliable delivery.

Source: Amazon

Advertising: A High-Margin Powerhouse

Amazon's advertising arm has emerged as a pivotal growth and profitability driver within its vast ecosystem, leveraging its data-rich platform and extensive user base to deliver highly targeted ads.

Revenue Generation

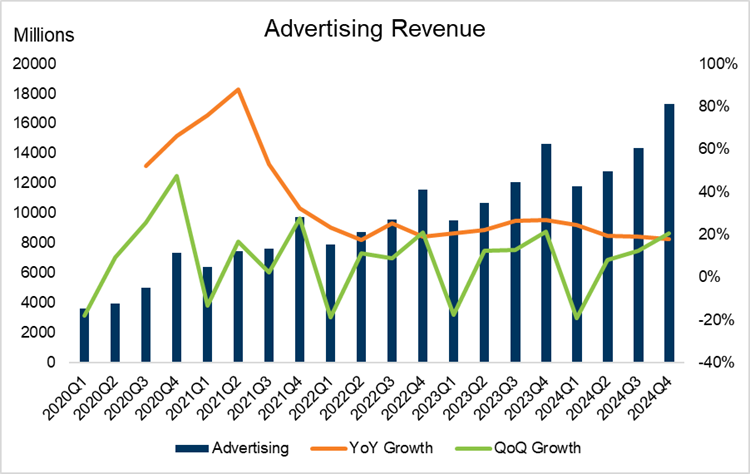

Amazon's advertising business continues to thrive, powered by its proprietary search algorithm that matches user queries with highly relevant offers. In 2024 Advertising revenue rose to $56 billion, an 8.8% year-over-year increase, driven by product promotions and the integration of ads into Prime Video. The addition of ads to Prime Video has become a significant growth factor, demonstrating the vitality of Amazon's advertising segment.

Source: Amazon, Tradingkey.com

Annual Run Rate

The advertising sector now boasts an annual run rate of $69 billion, a dramatic leap from $29 billion just four years ago. This trajectory highlights the scalability of Amazon's ad business, fueled by its extensive reach and the ability to monetize its ecosystem efficiently.

Growth Drivers

Several key factors have propelled Amazon's advertising success:

- Product Promotions: This remains the cornerstone of Amazon's ad revenue, with consistently high conversion rates driving ad spend growth. The stability of product promotion ads underscores their role as a durable income source.

- Streaming Media Expansion: The introduction of ads on Prime Video, now in its second year, has captured market share from traditional TV and other streaming services. With over 200 million monthly viewers, Prime Video is a lucrative platform for ad growth, enabling Amazon to diversify its advertising offerings.

Market Share

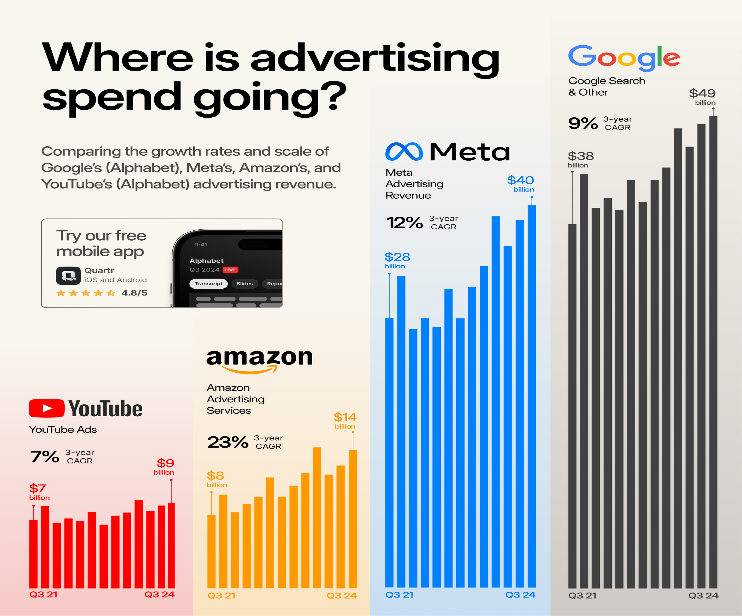

Amazon is solidifying its dominance in the global digital advertising market. In 2024, Amazon captured 11.3% of global digital ad spending, reflecting strong growth across multiple formats. In the U.S., Amazon commands 77% of digital retail media spending, up from previous years, underscoring its leadership in this niche market.

Source: Quantr

Future Revenue Potential

Amazon’s advertising arm is well-positioned for continued growth, bolstered by its strategic advantages:

- Full-Funnel Advertising: Amazon's ability to target customers across the entire purchase journey gives it a competitive edge.

- Advanced Data Targeting: Tools like Amazon Marketing Cloud and multi-touch attribution enhance advertisers' ability to measure and optimize campaigns.

- Streaming Ads: The expansion into streaming media ads is expected to drive significant revenue as advertisers shift budgets from traditional TV to digital platforms.

AWS:Driving Growth and AI Leadership

AWS continues to be Amazon's primary engine of growth and profitability, reinforcing its leadership in the cloud computing market. With strong performance, impressive profitability, and strategic investments in AI, AWS is well-positioned to capitalize on future growth opportunities and maintain its competitive edge in a rapidly evolving industry.

A Strong Growth Engine

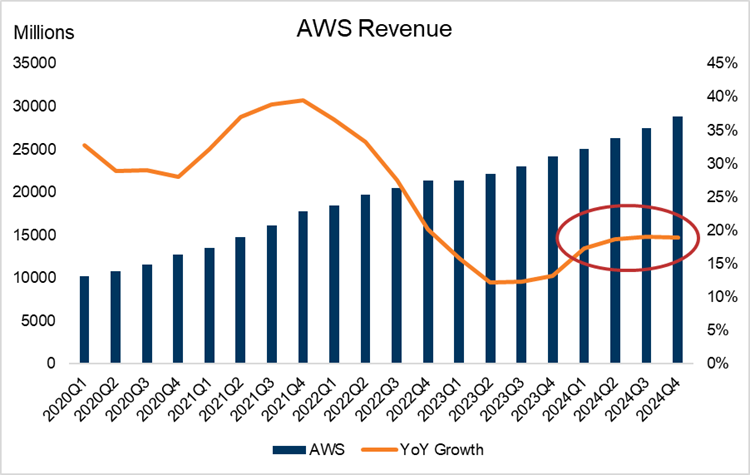

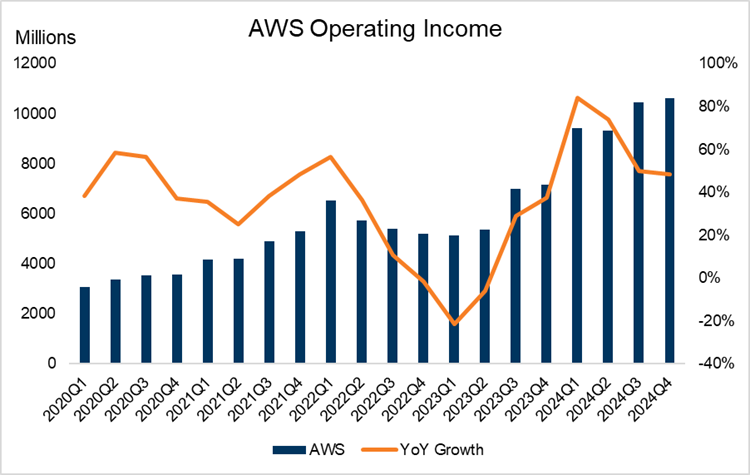

AWS delivered strong performance in Q4 2024, achieving revenue of $28.8 billion, a 19% year-over-year increase. This marks consistent growth from Q3 to Q4, showcasing AWS's stability in a competitive market. Over the full year, AWS has reinforced its role as Amazon’s primary growth engine, even as competition in the cloud market intensifies.

Source: Amazon, Tradingkey.com

Profitability and High Margins

AWS reported an operating income of $10.6 billion in Q4 2024, reflecting a 48% year-over-year increase and an impressive operating margin of 37%. Despite representing only one-tenth of Amazon’s North American sales, AWS generates more operating profit, illustrating the high-margin nature of cloud services. AWS also benefits from post-holiday strategic planning, completed cost optimizations, and the rollout of high-margin AI services, further driving profitability. Q1 typically shows the highest operating income growth for AWS, aligning with the start of many companies’ fiscal years, new cloud commitments, and budget allocations.

Source: Amazon, Tradingkey.com

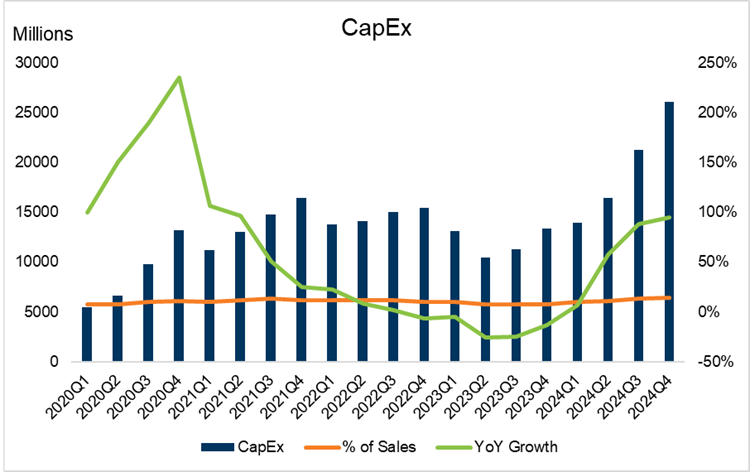

CapEx and Depreciation

Amazon reported a capital expenditure of roughly $26.3 billion for Q4, with a large chunk of this investment directed towards AWS's infrastructure, especially to accommodate the rising demand for AI services. This substantial CapEx, while beneficial for long-term growth, has introduced some pressure on profitability due to increased depreciation costs. This might lead to a dip in AWS's profit margins in the near future as these investments depreciate over time.

Source: Amazon, Tradingkey.com

Investing in AI and Compute Power

AWS’s strategic focus on AI positions it as a leader in the AI revolution. By investing heavily in cutting-edge infrastructure, proprietary hardware, and advanced AI services, AWS is enabling companies to unlock the potential of AI at scale. Key elements of its AI strategy include:

- Proprietary Chips: AWS leverages its Trainium chips, alongside NVIDIA GPUs, to deliver high-performance AI workloads at competitive costs.

- Cost Efficiency: Chips like Trainium2 lower the cost of AI computing, making AI more accessible for startups and enterprises alike, thereby accelerating adoption. Trainium chips could offer 30-40% better price performance than Nvidia's GPUs in some scenario according to Amazon.

- Optimized Performance: Trainium’s architecture is designed for faster training times and efficient inference, which is increasingly critical as AI models grow in complexity.

- Strategic Independence: Developing proprietary chips reduces AWS’s dependence on third-party hardware, enhancing performance optimization and supply chain control.

- Scalability: AWS's scalability allows companies to manage massive AI models, providing the infrastructure essential for pioneering AI-driven innovations.

- Strategic Partnerships and Customer Growth: AWS strengthens its leadership in AI-driven cloud solutions by securing key contracts and driving adoption of offerings like Amazon Bedrock, SageMaker, and advanced models such as DeepSeek's R1.

Trainium chips are in mass production, evidenced by AWS deploying a 400k Trainium2 chip cluster for Anthropic's "Project Rainier," while AWS planning a future deployment of over 1 million Trainium chips in 2025.

Supply Constraints

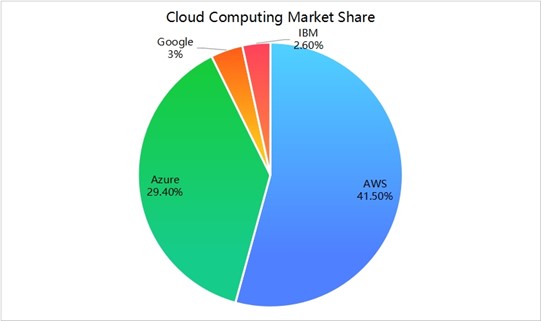

Despite its growth, AWS is not immune to industry-wide issues such as long build times for data centers and hardware supply constraints, which have slightly slowed down the pace of expansion, which affacted its competitors. In Q4 2024, Google Cloud's 30% year-over-year growth rate and Azure's 29% growth rate both fell short of Wall Street's expectations. However, AWS seems to manage these better than some competitors, maintaining a higher growth rate than Azure and Google Cloud.

Source: Sortlist, Tradingkey.com

Valuation

Amazon’s valuation highlights its leadership in e-commerce, cloud computing (AWS), and digital advertising, supported by innovation and high-margin scalability. Our scenario analysis outlines three potential valuation cases:

- Base Case ($245): AWS drives over 50% of operating income, with 9.5% sales CAGR through 2030, steady growth in Advertising and Retail, and continued AI investments.

- Bear Case ($185): Diversified revenue streams and strong cash flow provide resilience against Retail headwinds, with AWS maintaining EBITDA margins of 21%.

- Bull Case ($310): AWS and Advertising outperform expectations, driven by AI adoption and advertiser demand, achieving 12.2% sales CAGR through 2030 and 25% EBITDA margins by 2025.