Cybersecurity Stocks: What to Watch Ahead of Palo Alto Networks’ Q4 2024 Results

TradingKey - We all know that cybersecurity is a “must have” for all companies as increasingly large amounts of sensitive data transition online or to the cloud.

Thankfully, there are many companies in the cybersecurity industry that serve companies’ needs. One of the biggest is cybersecurity solutions provider Palo Alto Networks Inc (NASDAQ: PANW).

Palo Alto has taken a “platformisation” approach to cybersecurity by integrating diverse security solutions into a unified, scalable platform.

The cybersecurity player is set to report its Q2 FY2025 earnings (for the three months ending 31 January 2025) on Thursday (13 February) after the market closes in the US. Here’s what tech and cybersecurity investors should be watching ahead of its results.

Is new strategy paying off?

Palo Alto pivoted towards a new strategy of bundling together security solutions in a more integrated manner via its “platformisation” approach. Previously, the company sold individual security products and this was seen as a less inefficient and more fragmented approach to cybersecurity.

The company actually saw a big share price drop last year as near-term earnings took a hit and deal flow also slowed. However, that is now changing and since that big one-day fall about a year ago, shares are up 49%. Investors will no doubt be keen to see whether the new strategy’s benefits are continuing to show up in the numbers.

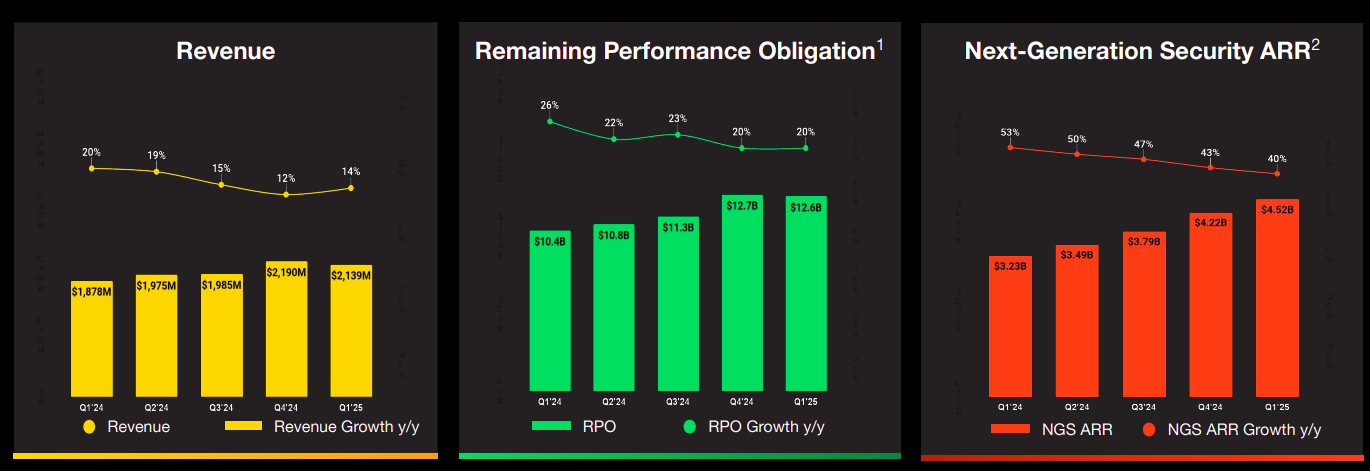

In Q1 FY2025, Palo Alto saw revenue of US$2.14 billion which was up 14% year-on-year. This was a sequential increase in the growth rate, up from the 12% year-on-year revenue growth for Q4 FY2025, but revenue was actually down in Q1 FY2025 from the prior quarter.

Meanwhile, Remaining Performance Obligation (RPO) – a key metric for software firms that combines deferred revenue and backlog (including unbilled revenue) in order to highlight future revenue potential – for Palo Alto in Q1 FY2025 came in at US$12.6 billion and was up 20% year-on-year. Both revenue and RPO beat consensus expectations in Q1 FY2025.

With the company wanting to create more annual recurring revenue (ARR), it was positive to see that its next-generation security ARR was up 40% year-on-year in Q1 FY2025 to US$4.52 billion. Palo Alto also said that US$250 million of this total came from Artificial Intelligence-related ARR as the importance of AI starts to ramp up in cybersecurity.

Key metrics for Palo Alto Networks Q1 FY2025

Source: Palo Alto Networks Q1 FY2025 earnings presentation

Guidance not too big to beat

Guidance from Palo Alto management for Q2 FY2025 wasn’t set too high when it released its Q1 FY2025 earnings back in late November 2024. Indeed, revenue for Q2 FY2025 is expected to come in between a range of US$2.22 billion to US$2.25 billion, up 12% to 14% year-on-year.

In terms of RPO, management guided for a range of US$12.9 billion to US$13.0 billion for Q2 FY2025 which would represent 20% to 21% year-on-year growth.

The most positive aspect of the company’s shift towards platformisation is that the cycle times to close deals appears to be reducing, according to management. Deals are also being structured to maximise ARR and also profitability.

Palo Alto is also well positioned to take advantage of strategic enterprise AI projects for cybersecurity in the years ahead as it recently launched a number of AI products, including Access and security posture management (SPM) – which should help the firm achieve greater scale in its platformisation quest.

For long-term investors in the cybersecurity space, Palo Alto Networks is certainly a company that is continuing to grow with a strategy that appears to be paying dividends. More details will come on Thursday.