Shopify Stock’s Q4 2024: Shares Swing on Mixed Earnings

TradingKey - With all the doom and gloom we read in the financial media, you’d think the global economy was in a recession.

Yet the world’s biggest economy – the US – is still growing relatively well and the global consumer has also held up by continuing to consistently spend more. Of course, holiday season sales are a key metric for any company involved in the world of retail.

While digital storefront provider Shopify Inc (NYSE: SHOP) doesn’t directly sell to consumers, over two million merchants worldwide use its software and payments processing platforms to create their own online stores.

In that sense, it’s a core part of the e-commerce world. Shopify also reported its Q4 2024 results on Tuesday (11 February) before the market open. Shares in Shopify initially fell as much as 9% in pre-market trading but then rebounded and ended the day up 3.1%.

What caused the wild swings? Here’s what investors should know about the e-commerce giant’s latest earnings and what investors were responding to.

Holiday quarter for Shopify impresses

As is the case each year, holiday quarter numbers were in focus for Shopify and the company did not disappoint. On the top line, Shopify delivered revenue of US$2.81 billion for Q4 2024, up 31% year-on-year.

This came in higher than the mid- to high-20s percentage guidance for revenue growth that Shopify management forecast back in November. It also beat analysts’ average consensus estimate of US$2.73 billion in revenue.

Gross merchandise volume (GMV), the overall value of merchant sales across Shopify’s systems, also hit a new record high of US$94.5 billion during the quarter and was up 26% year-on-year from the same period in 2023.

On the cash flow side of things, the numbers looked even more encouraging. Operating income for Shopify during Q4 2024 was US$465 million, up from US$289 million in Q4 2023.

Meanwhile, free cash flow was US$611 million for the quarter, up 37% year-on-year from the US$289 million in free cash flow for Q4 2024. That saw Shopify’s free cash flow margin hit 22% for Q4 2024.

Guidance disappoints but opportunities persist

What the market didn’t like about Shopify’s numbers came in the forward-looking guidance that management gave.

For Q1 2025, Shopify projected that revenue would grow at a mid-20s percentage rate, year-on-year. However, it was the operating expenses and free cash flow margin that slightly put off investors. The company foresees operating expenses rising as it looks to invest into R&D, marketing, and expansion into newer markets, according to Shopify CFO Jeff Hoffmeister.

Despite that, the investment is a good sign that management foresees opportunities to keep growing the Shopify business. Indeed, for the whole of 2024, Shopify’s international business grew revenue by 33% year-on-year – outpacing its overall 2024 revenue growth rate of 26%.

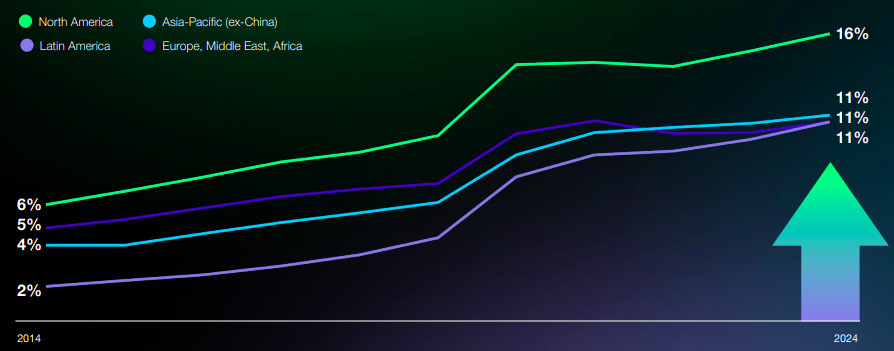

The company is starting to become a much more global e-commerce outfit rather than one focused primarily on North America. Given the lower penetration of e-commerce (as a percentage of overall retail sales) in regions outside of North America, that means there’s still plenty of growth potential ahead for Shopify.

E-commerce penetration as percentage of overall retail sales

Sources: Shopify Q4 2024 earnings presentation, eMarketer

What should investors be monitoring?

Besides the obvious top-line growth and holiday quarter numbers, investors should be on the lookout for how Shopify’s payment systems – Shopify Payments and Shop Pay – are performing and helping drive traffic to its merchants.

For Q3 2024, Shopify Payments processed US$43 billion in gross payment volume (GPV) which was up 31% year-on-year. Meanwhile, Shop Pay – which is a secure one-tap checkout option – was used for US$17 billion worth of gross merchandise value (GMV) during Q3 2024, up 42% year-on-year.

This virtuous flywheel for Shopify is what is driving growth and investors will want to see similarly strong numbers come Tuesday morning.

Solid quarter but things to watch

On the topic of tariffs, during the earnings call management addressed this and said that the company responded to the “de minimis” tariffs on small-value packages by working on a product solution for its merchants. Merchants can now display and collect duties at checkout, making the process much more seamless.

It was another solid quarter for Shopify but investors may be getting jittery about the near-term profit and margin outlook which explained the pre-market drop. However, Shopify shares had recovered that fall to open down around 2% and then finished the day over 3%.

That highlights how investors still believe the company has a strong long-term outlook for its business and earnings and the short-term miss on guidance is due to “good” factors like increased investment and opportunities to expand.