Airbnb Shares: Should Investors Be Bullish Ahead of Q4 2024 Results?

TradingKey - If we go on a holiday nowadays, many travellers could easily be choosing between a chain hotel or a property that is on Airbnb Inc (NASDAQ: ABNB).

By being a platform for landlords to connect with those looking for short-term stays and, increasingly long-term stays, Airbnb has become the “Netflix of travel”.

Outside of the traditional hotel groups, it’s the go-to platform and its December 2020 IPO was carried out at the height of the Covid-19 pandemic craze. Despite that, shares – now trading at around US$135 per share – are still well above the US$68 offer price.

Airbnb is also set to report its Q4 2024 earnings on Thursday (13 February) after the market closes. Given it has already achieved a profitable scale, alongside its ubiquitous nature, investors will be keen to hear more from management on the outlook for one of the world’s largest travel-related firms.

What’s on the itinerary for Airbnb?

Airbnb reported a solid Q3 2024 when it released its results for that period in early November 2024. In that report, the company posted revenue of US$3.73 billion, which was up 10% year-on-year and came in slightly ahead of expectations.

Airbnb also delivered net income of US$1.37 billion, or US$2.13 in earnings per share (EPS). That was a big drop from the US$4.37 billion net income, or US$6.63 in EPS, for Q3 2023 but the company did not a US$2.8 billion tax benefit for that quarter.

From that results release, management also guided for Q4 2024 revenue of between US$2.39 billion and US$2.44 billion. During Q3 2024, Airbnb also carried out share buybacks that totalled US$1.1 billion.

The company also noted in its Q3 2024 shareholder letter that its app bookings now account for 58% of total nights booked, significantly higher than the 53% from the same period in 2023. That should be getting investors looking towards how the company can continue to monetise its offering better via its mobile app.

Where are the growth areas for Airbnb?

For Airbnb, in Q3 2024, the company’s Nights and Experiences Booked increased by 8% year-on-year with nights booked on Airbnb’s app increasing 18% year-on-year during the quarter.

For Q4 2024, investors will be expecting this to continue as the company guided for year-on-year growth for Nights and Experiences Booked in Q4 2024 to be higher versus Q3 2024. For the whole of 2024, Airbnb foresees an adjusted EBITDA margin of around 35.5%.

However, the company also projected that its Q4 2024 adjusted EBITDA margin is expected to decline versus Q4 2023 given higher marketing and product development costs.

During Airbnb’s Q3 2024, one of the core growth markets for the company was Asia Pacific, where the region saw a 19% year-on-year rise in Nights and Experiences Booked during the period. The company also revealed that it saw cross-border travel to Asia Pacific grow by 23% year-on-year.

Solid metrics look to continue but concerns linger

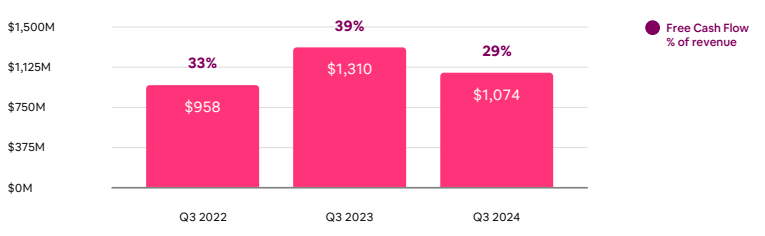

Airbnb has actually been a solid generator of free cash flow as well as operating cash flow. Investors might not be able to tell that given the company’s stock price is actually down over 12% in the past year.

But in Q3 2024, Airbnb generated US$1.07 billion in free cash flow with a free cash flow margin of 29%. While that was down year-on-year, it’s still up from Q3 2022 and the company appears to be a stable generator of free cash flow.

Airbnb quarterly free cash flow (US$ millions)

Source: Airbnb Q3 2024 shareholder letter

So while Airbnb is now consistently generating free cash flow alongside robust operating cash flow, investor sentiment has been weighed down by slowing revenue growth. In Q1 2024, the company posted 18% year-on-year revenue growth followed by Q2 2024’s 11% year-on-year revenue growth, and then Q3 2024’s 10% top line growth.

At the midpoint of Airbnb’s guided revenue range for Q4 2024 (US$2.41 billion), it translates into a year-on-year revenue growth rate of just under 10%. Therein lies the real conundrum for investors. Is the slowdown in Airbnb revenue growth something that is temporary and which can be reversed by its growth initiatives?

Investors will want to hear more from management on that as well as what they’re projecting for the whole of 2025. Despite all this, Airbnb remains a consistent, heavily cash-generating business and long-term investors could see any post-earnings dip as an opportunity to buy into a world-class brand in the online travel space.