Eli Lilly’s Q4 2024 Earnings: Is Stock Still a Buy After Latest Results?

TradingKey - For GLP-1 drug manufacturers, growth can be seen everywhere. One of the two big global pharma companies that sells these drugs is Eli Lilly & Co (NYSE: LLY).

The company reported its full Q4 2024 earnings before the market open on Thursday (6 February). Eli Lilly delivered a solid quarter, beating expectations on earnings per share (EPS).

The pharmaceutical giant reported Q4 2024 EPS of US$5.32, beating estimates by US$0.25, while revenue gained 45% year-on-year to US$13.53 billion.

While the revenue number had been known since last month, after a preliminary earnings release in mid-January, the beat on EPS was a new metric the company released and investors liked the sight of that. Eli Lilly shares finished the trading day up 3.4%, far outpacing the S&P 500 Index’s 0.4% gain for the day.

These impressive results were powered by the explosive growth of Mounjaro and Zepbound, two weight-loss and diabetes drugs that are reshaping the obesity treatment landscape.

With shares of Lilly skyrocketing nearly 150% over the past two years, investors are asking: Is there still upside, or has the stock run too far, too fast?

Revenue up on GLP-1 drugs

The key drivers of growth for Eli Lilly were no surprise. It was Mounjaro (its treatment for Type 2 diabetes) sales, that came in at US$3.5 billion in Q4 2024 sales and Zepbound (its treatment for obesity) that generated US$1.9 billion in Q4 2024 sales.

That resulted in total incretin (GLP-1 drugs) market share of 49% in the US versus its competitor’s – Novo Nordisk A/S (NYSE: NOVO) – 51% market share.

Mounjaro and Zepbound have quickly become category leaders, challenging Novo Nordisk’s Ozempic and Wegovy. Zepbound overtook Wegovy to become the market leader in obesity treatments in the US within months of launch.

Beyond weight-loss medications, oncology, immunology, and neuroscience also saw strong gains, with non-incretin revenue growing 20% year-on-year.

The total addressable market (TAM) for obesity treatments is massive, with analysts estimating it could exceed US$100 billion by 2030. With obesity affecting nearly 70% of US adults, demand for clinically proven, effective weight-loss solutions continues to soar.

Orforglipron: Game-changing oral GLP-1 drug

Eli Lilly is betting big on Orforglipron, a once-daily oral GLP-1 pill expected to launch in early 2026. Unlike Mounjaro and Zepbound, which require injections, Orforglipron eliminates the need for needles, making it an attractive alternative for millions of patients.

That ease of use could capture a much larger share of patients looking to go on obesity treatments.

Beyond that, the company is rapidly expanding Mounjaro and Zepbound internationally, with upcoming launches in China, Japan, and Europe. International sales should significantly ramp up in the second half of 2025, providing a new leg of growth for the company.

Valuation a concern?

Eli Lilly’s premium valuation is the biggest question mark. The stock trades at a forward price-to-earnings (PE) ratio of 57x, far higher than Novo Nordisk’s 36x. But here’s the catch – Eli Lilly is growing significantly faster than its peer.

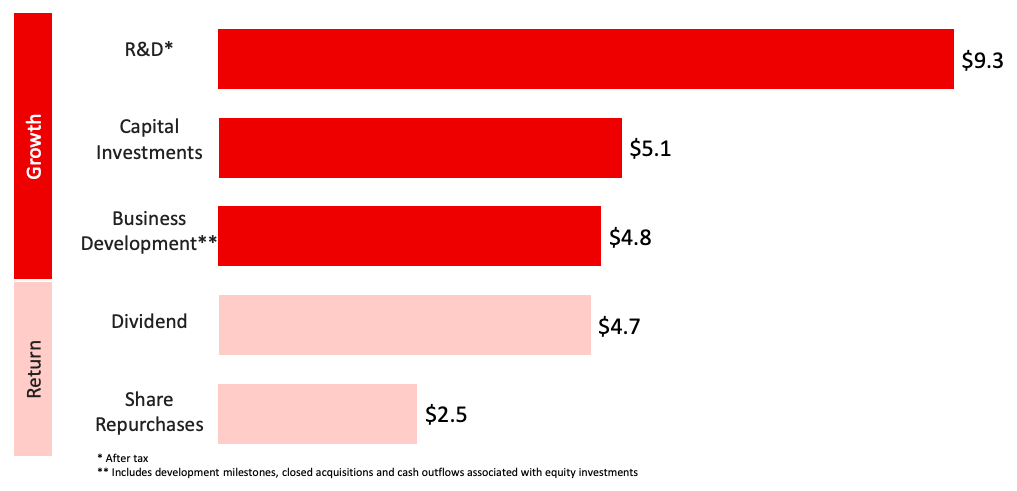

With projected 32% revenue growth in 2025 and 340 basis points of margin expansion, it’s hard to argue that the stock isn’t worth the premium. Eli Lilly also announced a US$15 billion share buyback and increased its dividend by 15%, signaling strong confidence in future cash flows.

Eli Lilly FY2024 capital allocation (US$ billions)

Source: Eli Lilly Q4 2024 earnings presentation

Despite the solid set of numbers, there are some factors to watch. First and foremost is the supply constraints. While Eli Lilly has ramped up production, demand still exceeds supply.

Meanwhile, there is intense competition from Novo Nordisk, which is also working on next-gen GLP-1 treatments, including a once-a-week pill that could rival Orforglipron. Finally, pressure from US drug pricing regulations, including potential Medicare negotiations, aren’t going to disappear quickly and could impact profitability over the long term.

Should you buy Eli Lilly stock?

Eli Lilly’s runway for growth is far from over. It is leading the charge in a once-in-a-generation medical breakthrough, with trillions in potential healthcare cost savings on the line.

Short-term investors should expect some volatility as supply catches up to demand. Meanwhile, Lilly’s dominance in weight-loss and diabetes treatments bodes well for long-term investors who see a long growth runway for the company.