U.S. Banking Sector Q4 2024 Earnings Preview

The fourth quarter of 2024 is poised to marks a significant shift to the U.S. banking landscape. As the Federal Reserve embarks on a rate-cutting cycle, the sector is transitioning from the high-interest-rate environment that dominated the past two years. This shift is expected to reduce net interest income for U.S. banks in 2025, with larger institutions likely facing slower earnings growth. However, the rate cuts could also stimulate loan demand, particularly as consumer savings dwindle and financial pressures mount.

Market expects that a potential return of Trump to the White House would introduce tax reduction policies, easing banks' tax burdens and spurring business investment and economic growth. Drawing from the 2017-2020 period, Trump's administration favored financial deregulation, which could lower compliance costs and operational pressures for banks. These factors, combined with heightened lending demand, are expected to bolster bank performance. With U.S. investment banks trading near record highs, market sentiment remains delicate. Given these dynamics, Q4 earnings per share (EPS) growth is likely to surpass Wall Street estimates, especially since actual EPS outperformed consensus in the first three quarters of 2024.

Source: LSEG, Tradingkey.com

Profitability Outlook:

Banks are anticipated to shift their focus from interest rate-driven gains to growth in trading volume. While net interest income may continue to decline, the rate-cutting environment could alleviate the intense competition for deposits, as customers may seek fewer high-yield products. Growth in trading volume could help offset shrinking net interest margins. Non-interest income, particularly from investment banking, may benefit from improved market valuations and risk appetite, though its performance hinges on the recovery of corporate financing demand.

Bank-Specific Analysis:

JPMorgan Chase:

With its diversified operations and strong market presence, JPMorgan is well-positioned to navigate this transitional period. Key areas to watch include its investment banking market share and trading revenue resilience. The investment banking division is expected to see positive momentum in Q4:

• Debt underwriting is likely to benefit from year-end corporate refinancing activity, as companies aim to lock in financing costs amid the current rate environment.

• M&A advisory has a robust pipeline, with revenue expected to materialize as deals close by year-end.

• Equity underwriting could gain from improved market sentiment, particularly in the technology and healthcare sectors.

• In its Markets division, fixed income and equity trading are expected to remain stable, supported by potential year-end market volatility.

Overall, JPMorgan’s investment banking arm, with its 9.1% global market share, is poised for moderate growth in Q4.

Goldman Sachs:

Goldman Sachs’ Q4 performance will largely depend on its Global Markets and Investment Banking segments. As a trading-focused institution, it is expected to benefit from:

• Increased institutional client activity, driving equity trading and derivatives revenue.

• Bond market volatility, creating opportunities for fixed income, currencies, and commodities (FICC) trading and underwriting.

• M&A advisory fees from year-end deal closures.

• Goldman’s asset management division, with assets under management (AUM) reaching $3.1 trillion in Q3, is expected to deliver steady revenue growth in Q4.

Morgan Stanley:

As a dominant player in wealth management and investment banking, Morgan Stanley is anticipated to sustain steady growth in its wealth management division during Q4 2024. Key areas of focus include net interest income performance amid expectations of rate cuts and potential growth in assets under management (AUM) driven by year-end client asset reallocations.

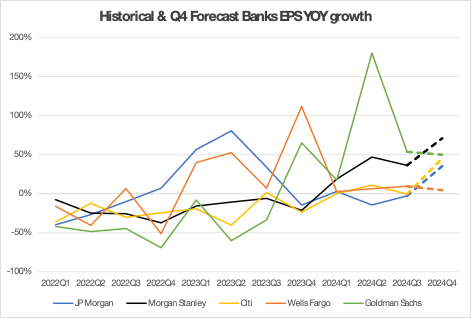

• Within its Institutional Securities segment, the firm’s leading equity trading business is expected to capitalize on trading opportunities arising from market volatility, building on the strong 21% year-over-year growth achieved in Q3.

• The Investment Management division, now fully integrated post-merger, is entering a phase of heightened activity, with year-end institutional allocations typically driving management fee income growth. However, the impact of market volatility on client investment appetite remains a factor to monitor closely.

Citigroup:

Under CEO Fraser’s strategic transformation plan, Citigroup is on track to meet its full-year expense and revenue targets in Q4, setting a solid foundation for 2025.

• The bank’s international operations, particularly in Asia and Europe, are expected to maintain the strong growth momentum seen in Q3, supported by robust demand in Asian wealth management and cross-border payments.

• The Services business, a consistent revenue generator, is likely to benefit from increasing cross-border payment and clearing activity. Positive trends from Q3, including an 8% rise in cross-border transaction value and a 7% increase in USD clearing volume, are expected to continue, bolstered by year-end corporate client needs.

• Wealth management, which saw a 24% surge in client investment assets in Q3, is poised for further growth in management fee income as AUM expands. However, the potential impact of market volatility on client investment decisions remains a concern. Additionally, credit card asset quality requires close attention, given the 39% year-over-year rise in net credit losses reported in Q3.

Wells Fargo:

Wells Fargo’s Q4 performance is expected to stabilize despite ongoing challenges. The Federal Reserve’s potential rate cuts in Q4 could place downward pressure on net interest income, as expectations of lower rates may further compress the net interest margin, which stood at 2.67% in Q3.

• Ongoing competition for deposits is likely to delay meaningful revenue improvements in the near term. However, amid economic recovery, Q3-end loan balances reached $910.3 billion with deposits at $1.34 trillion, suggesting continued moderate expansion in Q4.

• The investment banking segment is expected to benefit from heightened capital market activity, contributing to its ongoing improvement. Meanwhile, wealth management revenue is likely to remain resilient, driven by year-end financial planning demand.

• Credit quality is improving, with non-performing loan (NPL) ratios on a downward trend, though uncertainties in the commercial real estate sector, particularly office spaces, necessitate continued cautious provisioning in Q4.

• Core business lines are showing promise, with consumer banking expected to stay active during the year-end spending season, especially in credit card activity.

• Wealth management, supported by improved risk appetite and year-end asset allocation needs, has grown to $1.8 trillion in client assets and is positioned to maintain its positive momentum.