Does Qualcomm (QCOM) Have the Potential to be the Next Nvidia?

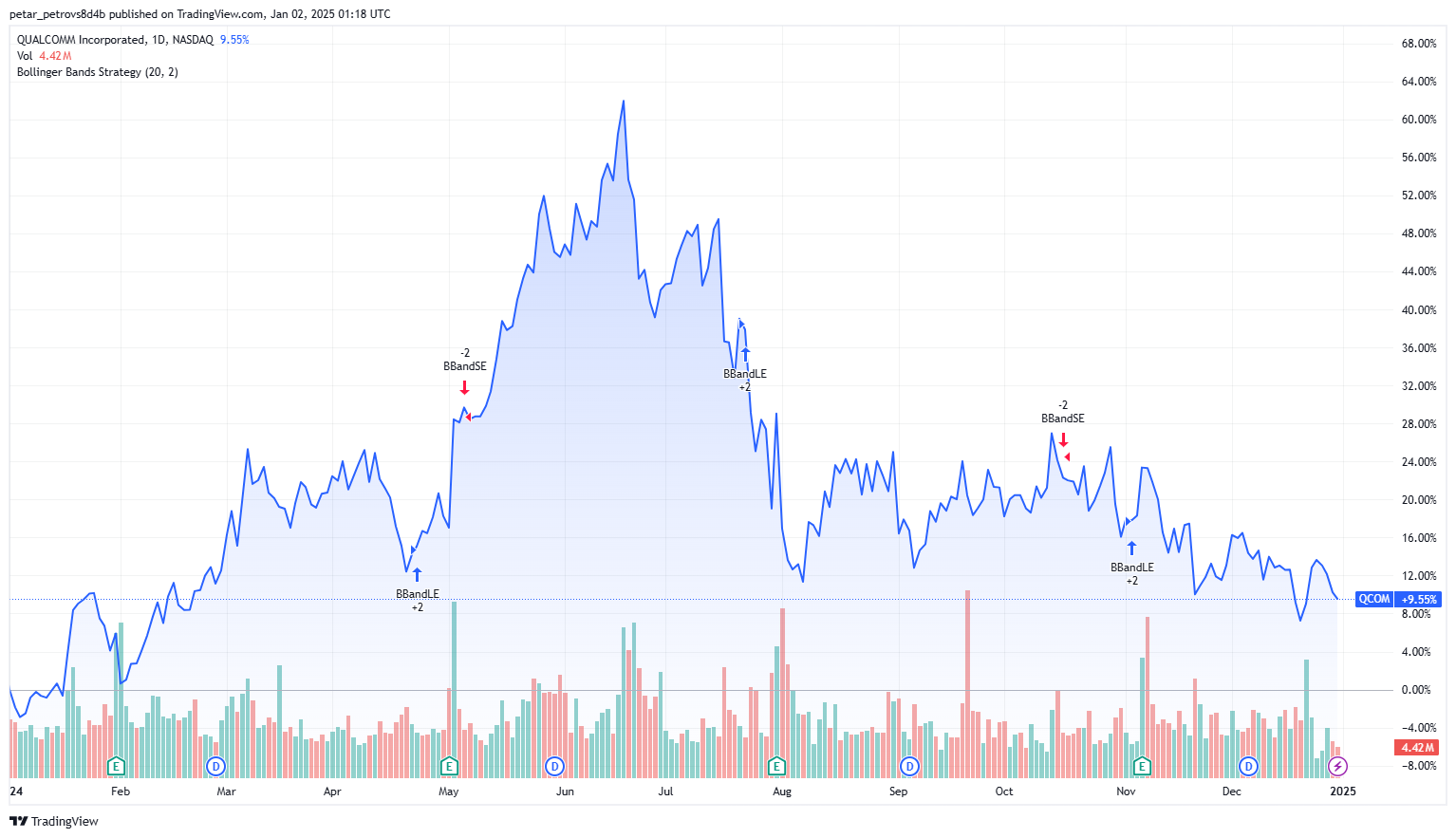

Source: TradingView

Too Many Uncertainties for QCOM to Go Up but Limited Downside, HOLD

In 2024, Qualcomm (QCOM) stock price went up just 10% - tepid growth in contrast with the broad market rally. The reason behind this is the QCOM investment thesis lays on several uncertainties: 1) The diversification of QCOM away from their legacy mobile business; 2) How US-China relations will affect their business in China; and 3) What will be the outcome of Apple producing their in-house modem. As long as these uncertainties are present, it will be difficult for QCOM to skyrocket, but on the positive note, the shareholder-friendly nature of the company (generous dividends and buybacks) provides a good safety net against major downturns.

How does QCOM Make Money?

Qualcomm is a semiconductor company that is primarily focused on wireless technology, especially related to 3G, 4G, 5G. That’s why their primary customers are mobile phone companies. This is different from other players focusing on CPUs, GPUs, or memory chips.

Qualcomm business model can be seen from several perspectives:

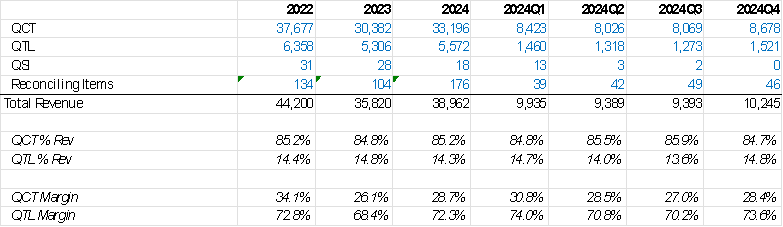

Qualcomm generates revenue from two major subsidiaries: Qualcomm CDMA Technologies (QCT) and Qualcomm Technology Licensing (QTL). QCT derives its revenue from the sale of products and services, primarily from the sale of chips for mobile devices, automotive, and Internet of Things (IoT) applications. On the other hand, QTL generates its revenue from licensing fees for its intellectual property (IP) portfolio, which includes patents for various wireless technologies. Unsurprisingly, the sales of products represent a very dominant portion of their total revenue, however the margins of the licensing business are much larger. QCOM also has a Qualcomm Strategic Initiatives (QSI) segment, but the revenue there is negligent.

Source: Company Financials

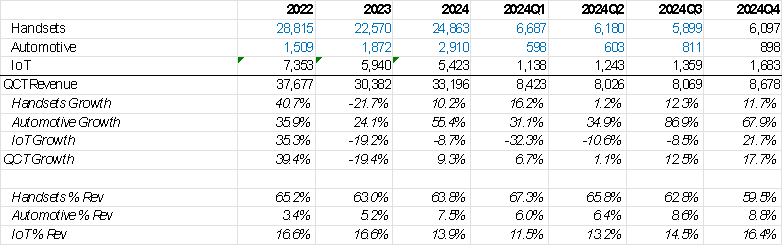

Where the products of QCOM are used is also an important aspect in understanding the company better. The majority of the QCT revenue comes from mobile phones (handsets). It is believed that Apple as a client contributes nearly 20% of the total sales. The rest of the end market are the growing businesses such as automotive and IoT. Due to the cyclicality of the mobile market, it is vital for the company’s future to focus on other business segments.

Source: Company Financials

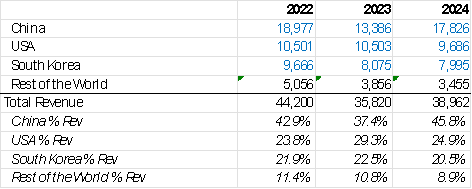

The geographical segmentation of revenue is also worth mentioning, as nearly half of the sales are from China. Even though it is not disclosed explicitly, it is believed that vast majority of the revenue from the US and South Korea comes from Apple and Samsung (~40% altogether).

Source: Company Financials

Licensing as a Centerpiece of Qualcomm Business

People often say that Qualcomm is a legal firm disguised as a tech firm. This is because the patent business is a huge part of their profit line. According to most recent data, QCOM has a total of 335 thousand patents grouped in 88 thousand patent families. The company is unmatched in its ability to derive revenue from both its products and patents. Even when QCOM sells a product, it also comes with a patent and the patent revenue streams continue even when the company stops selling the physical product.

This patent dominance by QCOM is getting challenged more in the recent years. The company often gets into lawsuits with different clients, and it is also closely observed by the anti-trust authorities in the US and globally. With the increased pressure of scrutiny, QCOM will have to adopt a less aggressive strategy towards licensing monetization, especially when a lot of license agreements with key OEMs expire in the coming 5-6 years.

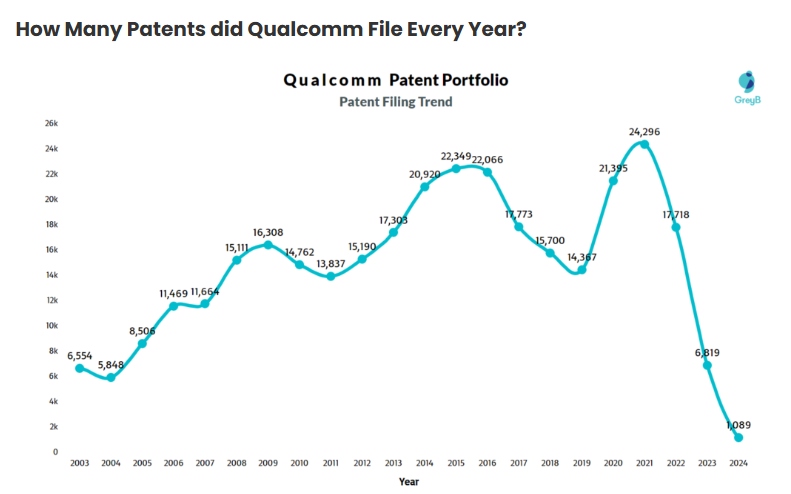

We can also observe that the number of patents filled in from Qualcomm has dropped significantly in the last three years.

Source: GreyB

Lots of Question Marks around QCOM as a stock

What makes QCOM like other semiconductor stocks is the cyclical/inconsistent nature of the revenue growth and the inconsistent gross margins.

Source: Company Financials

The quality of the revenue and margins is what differs the pure-play semiconductor stocks from successful stories like NVDA (and AMD to a certain extent), as the latter ones were able to venture into the lucrative data center segment, fueling their growth for the years ahead, while companies like Qualcomm are still struggling with cyclicality. The customers of Nvidia (aka the big AI spenders) will most probably continue to spend regardless of the economic situation, and this is what makes Nvidia revenue high quality. We cannot say the same thing for the customers of QCOM, which may easily cut spending once there is an economic downturn.

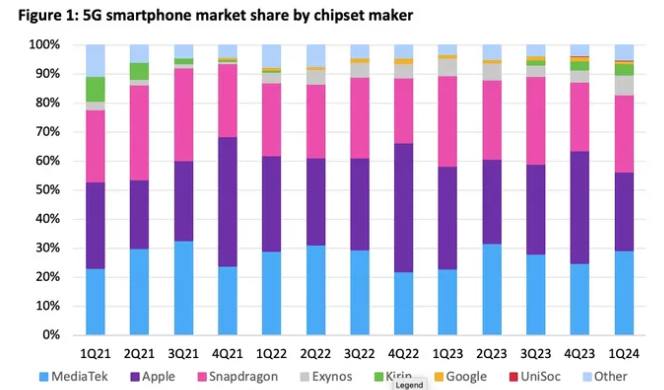

Further to this, we can see that within the smartphone industry, MediaTek has been taking market share from QCOM product – Snapdragon.

Source: Omdia Smartphone Model Market Tracker 1Q2024

At present, Qualcomm management is focusing on developing the non-headset business – PC, auto and IoT, as a way to move from the revenue cyclicality. So far, we can see the automotive business of QCOM performing more than remarkable as the largest OEMs across the industry are adopting Qualcomm’s Snapdragon platform and the digital chassis strategy, making QCOM a real leader in the automotive automation. However, auto-business itself is quite cyclical too, thus even if the current growth is very high, there is no guarantee this growth can be sustained in the long term.

The situation with IoT seems even less clear. The IoT-related revenue fell both in 2023 and 2024 respectively, despite the high management expectations at the beginning. However, this drop was most probably not due to poor management execution but more about IoT as a trend itself, not being able to materialize into a proper business case as of nowadays. There are a few factors holding IoT back such as lack of clarity in the applicability, lack of infrastructure to build on, and connectivity complexity.

The PC business is also a big question mark. QCOM, as a new player, will take time to establish a strong foothold within this market, but also it can utilize its expertise in the headset business. The PC market is competitive but also QCOM has a chance to steal some market share from INTC by taking advantage of its weaknesses.

The Risks are also there but Likely Overstated

Apple developing its own modem chip at this stage seems like a limited risk. First, the chances of Apple renewing its contract with QCOM beyond 2027 are still high. Apple has been working on this project for a couple of years after acquiring Intel modem business but has been constantly facing hurdles. Now they have a ready product, but it will only be used in the budget products of Apple (iPhone SE) since it is still not as superior as the QCOM components. Also, even if QCOM will not sell to Apple in the future, Apple still has to pay them licensing fees, making the profitability not as affected as many would think.

The other important risk is the big reliance on the Chinese market. Some of the largest phones and automakers are buying Qualcomm equipment. We believe this is a greater risk than the Apple one and also harder to quantify. On one hand, QCOM is probably the most exposed to China among the large US tech firms. On the other hand, the technology QCOM is involved in cannot be considered as too sensitive and the authorities will probably not risk harming the whole local mobile phone and EV industries by cutting QCOM away.

Source: Company Financials

Valuation

Currently, QCOM stock is traded with a 2025E Price-to-Earnings ratio at high-teens. Historically, the stock PE ratio has been quite stable, implying not much investor excitement:

Source: Bloomberg Intelligence

Growth-wise, we probably won’t see an explosive growth because the large growth from Auto and IoT will be offset by the sluggish growth in the legacy business.

Gross margins have been seeing a downward trend and will likely be further pressured by the fact that the licensing as a portion of the whole revenue will gradually diminish on the expense of lower-margin product revenue.

All things considered, the growth in profitability will be lower than the growth in revenue, with high single/low-teen percentage growth. This largely explains why the forward-looking valuations are not high.

We believe there might be some upside potential for QCOM but that really depends on how they develop their Auto and IoT business lines. If they are able to demonstrate high-level execution in the coming months, it won’t be surprising if they rerate upwards to 20 times 2025E P/E or $180.0 per share, but probably this will take some time.

What is worth mentioning is the fact that QCOM has always been generous towards investors, as their cash generating ability allows them to spend a significant portion of the free cash flows for either dividends or share buybacks. Thus, making the stock a safe bet for those who seek a growing dividend. But from the opposite perspective, we can view this as a potential risk of capex under-investing.

Source: Company Financials