Intel: Can It Turn the Tide?

Takeaways

- Intel is at a critical juncture, navigating challenges from rising competition, execution setbacks, and heavy capital demands under its IDM 2.0 strategy.

- While its foundation in PC and data center markets remains strong, execution risks in advanced process nodes and losses in its foundry business weigh on near-term prospects. That said, opportunities in AI, government subsidies, and potential breakthroughs in process technology offer long-term upside.

- Our valuation reflects this balance of risks and opportunities, resulting in a neutral rating and a target price range of $14–$28.

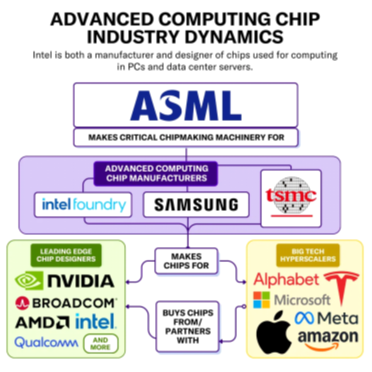

Company Overview: The Double-Edged Sword of Vertical Integration

Founded in 1968, Intel is one of the world’s largest semiconductor companies, known for its vertically integrated model (IDM, Integrated Device Manufacturer), which encompasses chip design, manufacturing, packaging, testing, and instruction set development. This model once gave Intel a strong advantage, particularly in the PC and data center markets.

Intel's Vertical Integration Model

Chip Design:

Intel handles everything from fundamental architecture design to microarchitecture implementation, covering: PC processors (e.g., Core, Xeon), Data center chips, GPUs, and Specialized accelerators (such as Mobileye for autonomous driving).

Chip Manufacturing:

Intel operates its own semiconductor fabrication facilities and produces chips using its proprietary process technologies, such as Intel 7, Intel 4, and 18A. This vertically integrated model historically allowed Intel to achieve technological leadership, driven by Moore's Law.

Instruction Set Architecture (ISA):

Intel is the primary developer of the x86 instruction set, which has long dominated the PC and server markets. This architecture is one of Intel's core "moats," providing a significant competitive advantage over rivals.

Source: EETOP

However, Intel's vertically integrated model has faced significant challenges in recent years: its process technology has lagged behind TSMC and Samsung, while it has been surpassed by NVIDIA and AMD in the GPU and AI accelerator markets. This all-encompassing internal model has also introduced immense cost pressures in the capital-intensive semiconductor industry, weakening Intel's overall competitiveness.

Strategic Adjustments: IDM 2.0 Strategy and Leadership Changes

1. IDM 2.0 Strategy: Reviving Manufacturing and Foundry Business

In 2021, the CEO Pat Gelsinger introduced the IDM 2.0 strategy to rebuild Intel’s manufacturing leadership and expand its foundry business.

Key Initiatives:

- 5 Nodes In 4 Years: Achieve five process nodes (Intel 7, Intel 4, Intel 3, 20A, 18A) by 2025, aiming to surpass TSMC and Samsung at the 18A node.

- Foundry Business Expansion: Attract external customers (e.g., Qualcomm, Amazon) and support multi-architecture chips (x86, ARM, RISC-V) to establish Intel Foundry Services (IFS) as a leading third-party foundry.

- Global Manufacturing Network: Build new fabs in Arizona, Ohio, and New Mexico, supported by $7.87 billion in U.S. CHIPS Act subsidies in November 2024.

Key Challenges:

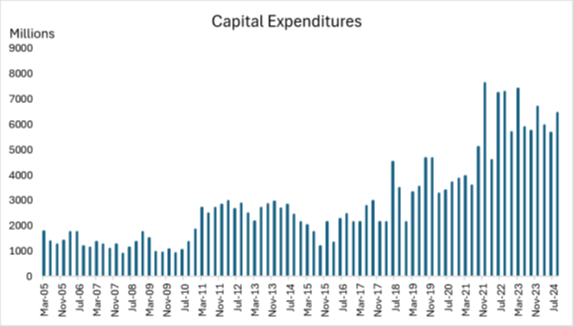

- Massive Capital Expenditures: IDM 2.0 requires over $100 billion in investments. Since 2021, capital expenditures have surged while revenue has declined, straining cash flow. Government subsidies cover only a fraction of the costs.

Source: LSEG, Tradingkey.com

- Technical Bottlenecks: Media reports suggest that Intel’s 18A process yields are only around 10%, raising concerns about customer confidence.

- Short-Term Losses vs. Long-Term Bets: The IFS business has accumulated losses of $17.56 billion from 2022 to Q3 2024, highlighting its short-term unprofitability despite requiring massive capital support, leading to dissatisfaction among board members and investors.

2. Leadership Changes: Gelsinger’s Legacy and New Directions

In December 2024, Gelsinger stepped down as CEO, possibly due to the slow progress of reforms and heavy spending. Interim co-CEOs David Zinsner (CFO) and Michelle Johnston Holthaus (General Manager of Client Computing) lack technical semiconductor backgrounds. They appear more focused on improving the profitability of existing products in the short term rather than doubling down on long-term bets like the foundry business.

Key Developments:

- Prioritizing Core Products: The focus shifts to enhancing profitability in PC and data center businesses.

- Potential Foundry Spin-Off: IFS may become an independent company through an IPO or external financing to ease cash flow pressures. However, this would weaken Intel’s vertical integration and reduce synergies between design and manufacturing. The CHIPS Act mandates that Intel retain at least 50.1% ownership if IFS is spun off, limiting its flexibility.

3. Internal Culture: From Technology-Driven to Finance-Oriented

Intel, once known for its innovation-driven culture, has shifted toward a finance-first approach in recent years:

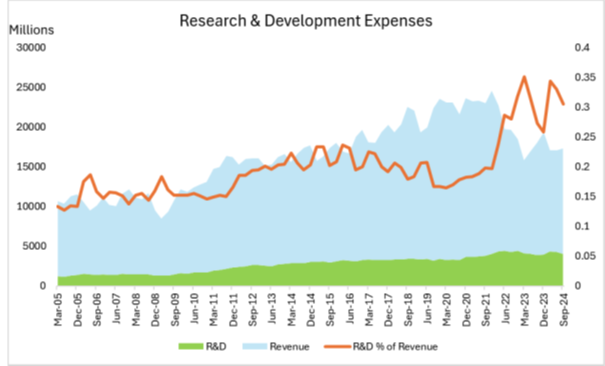

- R&D Cuts: Over the past decade, Intel prioritized shareholder returns, spending over $36 billion on stock buybacks and dividends instead of investing in R&D or emerging markets. R&D expenses dropped since 2016 and did not come back till 2021 when the company realized they should focus more on R&D. This delayed its response to its competitors’ rise.

Source: LSEG, Tradingkey.com

- Strategic Missteps: Aggressive technology choices (e.g., 10nm delays due to material issues) and slow adoption of EUV lithography allowed competitors like TSMC to take the lead.

Technology and Products: Eroding Moats and Innovation Challenges

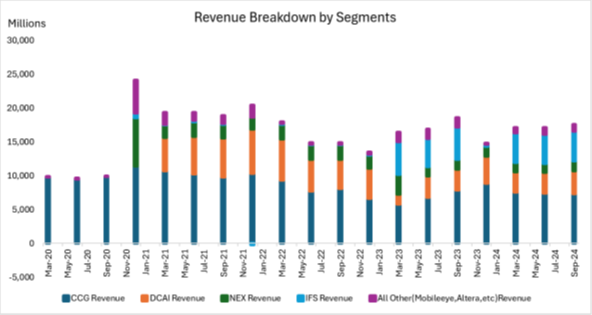

The following two charts are breakdowns of revenues and operating income for each segment to see their developments over the years.

Source: LSEG, Tradingkey.com

Source: LSEG, Tradingkey.com

1. Client Computing Group (CCG): Weakening Traditional Advantage

- Contribution to Revenue: CCG account for 42% of Intel's total revenue, making it the company’s “cash cow.” However, Q3 2024 Desktop Revenue: $2.07 billion, down 25% YoY. Weak desktop demand led to a 7% YoY decline in CCG revenue, with operating income down 2% YoY, dragging overall financial performance.

- Weak PC Market Demand: According to IDC and Gartner, global PC shipments have gradually declined post-pandemic, especially in the consumer market, where sluggish demand has shrunk the overall market size.

- Inventory Adjustments: Key customers, including Dell, HP, and Lenovo, had accumulated significant inventory in previous quarters. In Q3 2024, inventory digestion led to a noticeable slowdown in order demand.

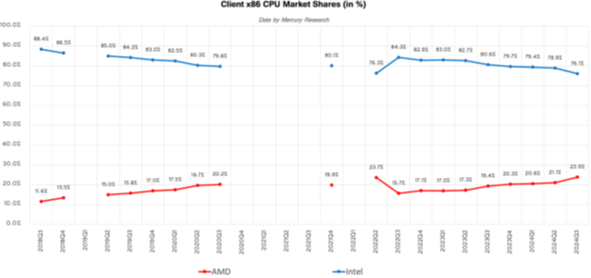

- Competition Intensifies: While Intel holds over 70% of the PC market, AMD, Apple’s M-series chips, and ARM-based designs are rapidly gaining market share.

Source: Mercury Research

2. Data Center & AI (DCAI): CPU Share Loss, GPU Challenges

- Contribution to Revenue: Data center account for 25% of total revenue, making it a critical growth area. Q3 2024 Revenue: $3.35 billion, up 9% YoY, driven by a 6% increase in server volume, mainly from hyperscale customer demand. ASP remained flat, with higher-core products contributing more to the mix. Operating Income: Declined 11% YoY, reflecting rising costs.

- Rising Costs:

High Initial Production Costs: Intel launched new products in 2024, including the Sapphire Rapids Xeon processors and Gaudi 2 AI accelerators, which incurred high production costs, particularly during the early yield ramp-up phase.

Increased R&D Expenses: Intel has made significant R&D investments in data center and AI fields to counter competition from AMD and NVIDIA.

Next-Generation Product Development: The development of next-generation products, such as Sierra Forest and Granite Rapids, has added significant costs to operational expenses.

- Market Share Challenges:

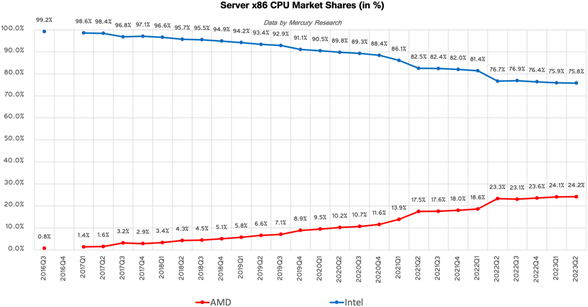

Data Center CPUs: Intel’s market share has declined to 75%, largely due to pressure from AMD.

Data Center GPUs: NVIDIA dominates with over 90% market share, and Intel’s Gaudi series has not posed a meaningful threat to NVIDIA’s position.

Source: Mercury Research

3. Network and Edge (NEX): Stable Growth Amid Challenges

- Contribution to Revenue: NEX accounts for 11% of total revenue and is considered a growth area, with a focus on 5G and edge computing. Q3 2024 Revenue: $1.51 billion, up 4% YoY, driven by growth in edge and networking businesses, partially offsetting inventory reductions by 5G customers. Operating Income: Increased 168% YoY, reflecting improved cost management.

- Cost Control and Efficiency Improvements: Intel optimized manufacturing and supply chain management for NEX-related products, achieving significant progress in operational cost control and production efficiency. This reduced operating expenses and boosted overall profit.

- Challenges: Inventory reductions of 5G customers continue to weigh on demand. Fluctuations in demand present ongoing challenges to revenue stability.

4. Foundry Business (IFS): High Losses Amid Strategic Focus

- Contribution to Revenue: IFS has been a significant drag on Intel’s financials, with quarterly operating losses. Q3 2024 Revenue: $4.4 billion, down 8% YoY from $4.7 billion in Q3 2023. In Q3 2024 alone, IFS incurred a loss of nearly $6 billion.

- Reasons for Decline:

Shift to Advanced Nodes: Focus on newer technologies like Intel 18A and advanced packaging reduced demand for traditional services.

Restructuring Impact: Intel took $3 billion in impairments related to Intel 7 equipment as part of cost-cutting efforts, disrupting short-term operations.

Customer Transitions: Customers are delaying orders, waiting for Intel's new nodes like Intel 18A to fully ramp up.

Market Conditions: Broader semiconductor industry slowdowns and inventory adjustments impacted demand.

- Technological Breakthroughs: RibbonFET and PowerVia: Key technologies for Intel’s 18A process, enabling further miniaturization and improved energy efficiency.

- Yield Challenges:

If 18A process yields remain below industry standards, it could severely impact customer confidence and strategic execution.

Competitors | Initial Yield | Mass Production Yield |

TSMC N3 | 60-70% | 75-80% |

Samasung 3nm GAA | 10-20% | ~60% |

Intel faces a dual challenge of cash flow pressure and rising capital expenditures. While PC chips remain its core profit driver, intensified competition in data center chips and foundry services, along with weak market demand, continue to constrain growth. Although the foundry business may provide long-term strategic support, its short-term losses and high capital requirements pose significant risks to Intel’s financial health.

Valuation

Use the Discounted Cash Flow (DCF) method to estimate Intel's intrinsic stock price. A sensitivity analysis is performed on the perpetual growth rate and WACC to capture valuation variability.

- Key Asuumptions:

Revenue Growth: Recovery begins post-2024 with projected growth of 5.86% in 2025 and 7.43% in 2026.

Free Cash Flow (FCF): Negative FCF in 2023-2024 due to high Capex but turning positive in 2025. Intel’s FCF is expected to turn positive in 2025 due to a significant reduction in capital expenditures as major fab investments under IDM 2.0 stabilize, coupled with revenue recovery driven by growth in AI, data center chips, and foundry services. Additionally, operating margins are projected to improve from cost optimizations, higher-margin product launches, and better execution of its advanced process nodes.

- Results:

A sensitivity analysis is performed on the perpetual growth rate and WACC to capture valuation variability because Intel's valuation is highly sensitive to changes in key assumptions. Based on our calculations, the WACC is approximately 8.5%. To account for potential variability, we used a WACC range of 8-10% in the analysis. For the growth rate, we assumed a range of 1.5-2.5%, considering that it aligns conservatively with long-term US GDP growth, which is typically in the 2-3% range.

Growth rate(%)/WACC(%) | 8% | 9% | 10% |

1.5% | 22.54 | 17.82 | 14.23 |

2% | 25 | 19.58 | 15.55 |

2.5% | 27.91 | 21.63 | 17.05 |

Based on the sensitivity analysis, the implied stock price for Intel ranges from $14.23 to $27.91.

Future Outlook: Opportunities and Risks

- Opportunities:

Process Technology Breakthroughs: If Intel can improve 18A yields within 12 months, it may regain customer confidence and market share.

Government Support: Subsidies and tax incentives under the CHIPS Act provide a cushion for expansion.

Foundry Business Potential: With technical progress and external financing, IFS could become a long-term growth engine.

- Risks:

Technical Challenges: Failure to resolve 18A yield issues could deepen Intel’s lag behind TSMC and Samsung.

Financial Strain: IFS losses and high capital expenditure may further weaken cash flow.

Intensifying Competition: Competitors like AMD continue to erode Intel’s market share, while NVIDIA dominates GPUs.