Goldman Sachs Asset Management’s Outlook for 2025: New Balancing Act for Investors

TradingKey - When it comes to the profession of banking, there are few names out there more respected than Goldman Sachs Group Inc (NYSE: GS).

While the bank has made a name for itself in investment banking, it also has a very strong asset management arm that is responsible for managing more and more “long-term” capital from clients such as endowments right through to high net-worth individuals.

Recently, Goldman Sachs Asset Management came out with its 2025 investment outlook for investors and here are some key talking points that investors should be aware of.

Balancing a new equilibrium

According to Goldman, the past few years of high inflation coupled with high interest rates is starting to fade away. The diminishing of these macroeconomic imbalances is undoubtedly a positive. Inflation has come off without a global recession taking hold and an easing cycle from global central banks is now underway.

The bank expects interest rate cuts across most developed and emerging markets in 2025 although the timelines for these will vary. The most important point is that interest rates will settle at a higher level than the low-rate world that we became accustomed to in the pre-pandemic era of 2009-2020.

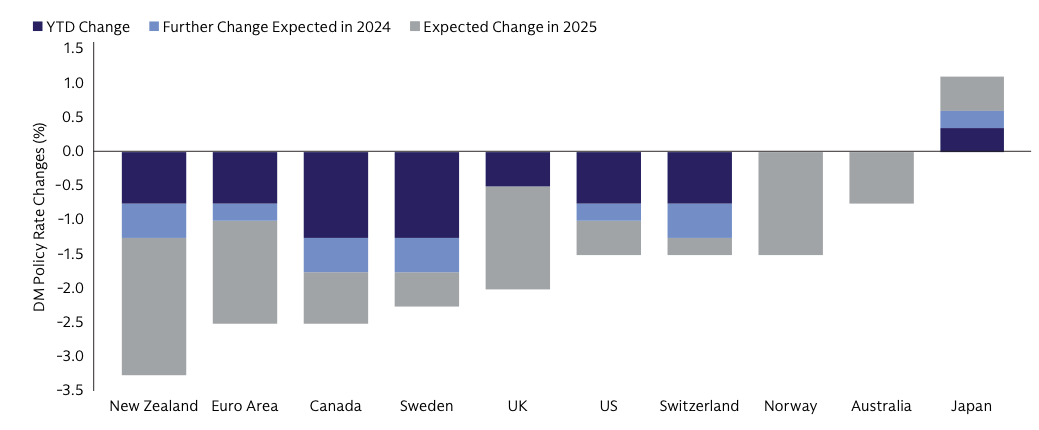

Easing underway in most Developed Markets and Goldman sees it continuing in 2025

Sources: Macrobond, Goldman Sachs Asset Management. Year-to-date (YTD) change as of 13 November 2024. Forecasts as of 9 November 2024.

What about the US? Well the economy there remains robust heading into 2025 and inflation is basically back at the US Federal Reserve’s target of 2%. Meanwhile, tight labour conditions have eased. All that is pointing towards the bank’s base-case scenario of a “soft landing” for the economy.

They expect additional cuts to the Fed Funds rate in 2025 – incumbent on inflation continuing to fall – and that could potentially mean an easing cycle that concludes by the end of the year.

Not surprisingly, the bank sees that inflation upside risks are posed by a second Trump presidency. This comes in the form of tariffs and it also raises the prospect of a Fed pause and a slower pace of cuts.

Incidentally, this is what happened in the latest FOMC gathering of the Fed during 17-18 December, where the central bank projected a total of two rate cuts in its December “dot plot” instead of the previous four.

More easing in both Developed and Emerging Markets

For Goldman, the Euro area’s loss of economic momentum and a second Trump presidency will put pressure on growth given potential tariffs and a focus on countries that have large trade deficits with the US. All this will mean that rate cuts will accelerate in 2025 for Europe.

Over in Japan, the country remains an economic outlier and its strong underlying wage-price dynamics mean that the Bank of Japan (BOJ) will further “normalise” policy in 2025 and Goldman expects gradual upward rate adjustments in 2025 as election uncertainty subsides.

For Emerging Markets (EMs), a Fed that continued to cut in the second half of this year had provided an opportunity for them to ease along with it. Asian markets are particularly rate sensitive to the Fed cycle and South Korea and Thailand have cut rates in the fourth quarter of 2024. Rates have also been cut in South Africa and Mexico in recent months.

In totality, EMs remain in strong shape given growth has stayed resilient and inflation is well below the 2022 peaks. While there are threats from tariffs once Trump takes office, the overall fiscal policy in EMs has been less expansionary than its Developed Market peers. Central banks in EMs are also driving more demand for hold as a hedge against any geopolitical uncertainty.

Where do the opportunities exist in 2025?

In conclusion, Goldman Sachs Asset Management is relatively sanguine on the outlook for stock investors heading into the new year.

The main takeaway from Goldman, for investors, is that it sees as strong case for international diversification (away from the US) given the narrow gains in the market in the world’s largest stock market – it remains near its highest level of concentration in 100 years.

Of course, it does acknowledge that the US market remains attractive, too, given the country’s resilient econoimic growth, consistent earnings growth, and culture of innovation.

However, better value opportunities exist elsewhere. European banks, for example, have recently outperformed the “Mag 7” tech stocks. Areas in Europe, such as healthcare, green energy, and luxury goods, also contain companies that don’t have US equivalents or are more attractively priced.

Outside of the US, Goldman favours dividend-paying companies with sustainable returns on invested capital, strong cash flow generation, and a robust track record of capital disciplined and dividend payouts.

This focus on a “defensive value” approach to international markets could prove rewarding for investors, particularly in Europe – where growth risks are skewed more to the downside.