December 2024: Top AI Stocks to Capitalize on Artificial Intelligence Growth

The surging integration of AI has driven a significant uptick in tech stocks in 2024, with strong indications that this trend will continue into 2025. As a result, we have pinpointed a set of stocks that are primed for investment. Following our in-depth analysis in Micron Technology (MU) and NVIDIA (NVDA), we are now turning our focus to the next three companies in our portfolio.

Overview of selected stocks

Ticker | Name |

NVDA | NVIDIA Corp |

MU | Micron Technology |

CRDO | Credo Technology |

STX | Seagate Technology |

PINS | Pinterest Inc |

Source: Tradingkey.com

Credo Technology

Price overview

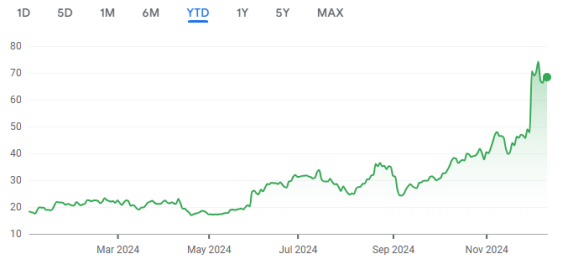

Credo Technology's stock has risen by 272.3% year-to-date, with a 47.3% decline in the past month. Given its robust growth prospects, we believe this presents a buying opportunity in the short term.

Source: Google Finance, Tradingkey.com

Business overview

Credo Technology provides high-speed connectivity solutions that enhance data infrastructure, breaking bandwidth barriers with power and cost efficiency. Their offerings include active electrical cables, optical DSPs, and SerDes technologies, which ensure reliable high-speed data transfer. Credo's innovation, market responsiveness, and industry partnerships secure its competitive edge in AI and data centers.

Financial overview

Growth Drivers:

· Leading provider of high-speed connectivity for AI and data infrastructure, with a focus on AEC technology.

· Q2 FY25 revenue jumped 88% YoY to $72M, with a diversified client base and new product launches.

· Projected revenue growth to $800M by FY27, driven by AI market demand and client expansion.

Margins:

· Achieved a 63.6% non-GAAP gross margin and holds a strong cash position of $383M.

Risks:

· Faces competition from industry giants like Marvell and Broadcom.

· Must sustain innovation amid rapid technological changes.

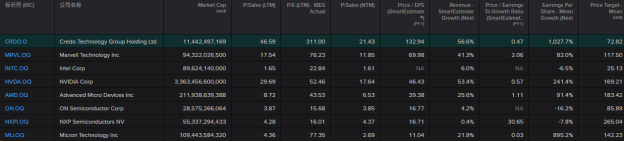

Valuation

The company is currently trading at a P/E ratio of 311 and P/S ratio of 46.6, which is relatively high compared to its peer. Analysts anticipate Credo Technology's P/E ratio for the next year to be 132.9. However, considering the company's robust EPS growth forecast of 1027.7% for the next year, it suggests that the stock has potential for its share price to increase. This high growth rate could justify the elevated P/E ratio, indicating that investors expect significant earnings growth in the future, which could drive the stock price higher.

Peer comparison

Source: Refinitiv, Tradingkey.com

Seagate Technology

Price overview

Seagate Technology's stock has risen by 18.1% year-to-date, with a 2.2% decline in the past month. Given its robust growth prospects, we believe this presents a buying opportunity in the short term.

Source: Google Finance, Tradingkey.com

Business overview

Seagate Technology is a prominent global manufacturer of hard disk drives (HDDs), holding a dominant position in the enterprise storage solutions market, especially within the Nearline HDD segment. With over 40 years of industry experience, Seagate has solidified its reputation as a leading innovator in mass-capacity data storage solutions. The company's product portfolio encompasses a diverse range of HDDs, solid-state drives (SSDs), and data management services, catering to both consumer and enterprise segments

Financial overview

Growth Drivers:

· Seagate's strategic focus on cloud and enterprise customers has been highly successful, with all Nearline exabyte products sold out for 2024, indicating strong and sustained cloud demand as a key growth driver.

· AI-Driven Solutions: Seagate capitalizes on the AI boom, with enterprise data growth projected at over 40% CAGR, aiming for higher-margin products.

Margins:

· Gross Margin: Seagate reported a 33.3% gross margin in Q1 2025, with a forecasted increase to 34.2%, reflecting financial strength.

Risks:

· HAMR Delays: Delays in HAMR technology could affect Seagate's competitiveness in high-capacity drives, and production capacity limits may hinder meeting growing demand, increasing competition.

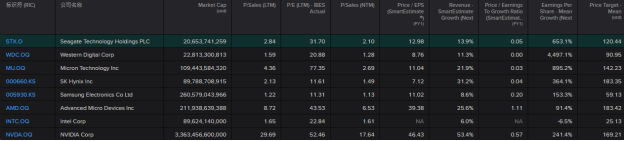

Valuation

The company's P/E ratio of 31.7 is in line with the industry average. Considering its strong revenue and earnings growth, coupled with a PEG ratio of 0.05, the stock presents an enticing investment prospect.

Peer comparison

Source: Refinitiv, Tradingkey.com

Pinterest Inc

Price overview

Source: Google Finance, Tradingkey.com

Business overview

Pinterest is a leading global visual search and discovery engine, engaging over 537 million monthly active users, notably Gen Z and women, in over 100 countries. It capitalizes on the path from inspiration to purchase by integrating seamlessly with advertisers' marketing strategies within a secure brand environment. Revenue is primarily derived from digital advertising, including video, carousel, and shopping ads, managed through an auction-based model focused on maximizing user engagement and advertiser ROI. The company is dedicated to AI investments to refine personalization and boost advertising efficiency.

Financial overview

Growth Drivers:

· Pinterest serves 537 million monthly active users globally (yoy growth rate at 11%), positioning it at the intersection of social media, e-commerce, and visual search.

· Q3 2024 revenue grew 18% YoY to $898 million, with key market monetization in U.S., Canada, Europe, and Rest of World. Also over 96% of Pinterest queries are unbranded searches, offering advertisers early engagement opportunities.

· AI integration through initiatives like Performance+ has improved cost-per-action for shopping campaigns by 20%.

Margins:

· Adjusted EBITDA margin stands at 27%, considering strong revenue growth, EBITDA margin is expected to reach 31.5% by 2026.

Risks:

· Revenue deceleration and growth limitations in mature markets.

· Balancing ad load with user experience to maintain engagement.

Valuation

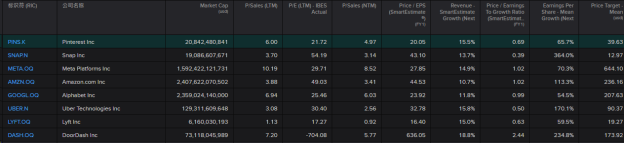

The company has demonstrated consistent revenue growth, with an 18% increase for three consecutive quarters, and a monthly active user (MAU) growth rate that has held steady at 11-12% year-over-year for four quarters. Currently, the company's LTM P/E ratio stands at 21.7, which is considered low within its industry. Furthermore, with an anticipated PEG ratio of 0.69 for the coming year, we believe the recent pullback in the stock price presents a buying opportunity.

Source: Refinitiv, Tradingkey.com