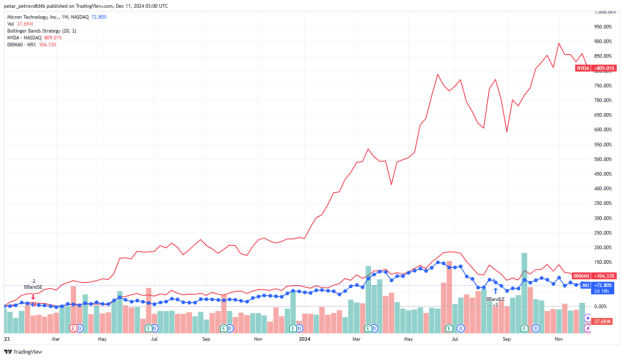

Micron Technology (MU): Why 2025 can be a great year for the stock

Source: TradingView

Summary

Since the beginning of the AI Boom, Micron has not been able to repeat the success of other semiconductor stocks like NVDA and AMD, which is understandable, considering the heavy cyclicality typical for the memory chip industry, compared to the logic chip industry. However, the market overlooks that the rapid adoption of High Bandwidth Memory technology will bring the much-needed tailwind for memory stocks like MU. This factor, combined with the significant efforts of Micron and the other memory chip firms to smoothen the cyclicality of their sales, puts their stocks in a good position for high investment returns.

Industry Overview

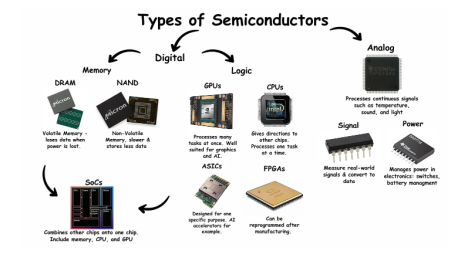

Micron is a semiconductor stock, but its business differs from that of Nvidia, AMD, and Intel. This is because MU is engaged with the design, production, and selling of memory chips, which have functions different from those of CPUs and GPUs produced by the companies mentioned above.

Source: Felicis Ventures

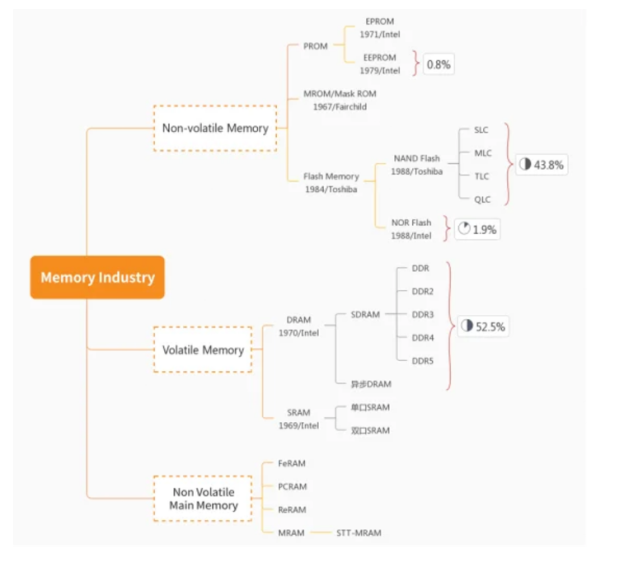

Memory chips are a subsection of digital chips, along with logic chips (CPUs and GPUs). While the main function of logic chips is to process information to complete a task, the purpose of memory chips is to store data.

Two main types of memory chips cover over ninety per cent of the memory market – DRAM and NAND. DRAM chips are ‘volatile’ memory chips, which means their data is lost when the power source to the chip is turned off. DRAM offers a larger store capacity and a faster speed. DRAM is used when fast processing speed is required. NAND chips, on the other hand, are non-volatile memory chips that preserve saved data when the power is turned off. NAND chips are used when data must be permanently saved. We can think of these two types as “memory” and “storage”, respectively.

Source: Depend Electronics Ltd

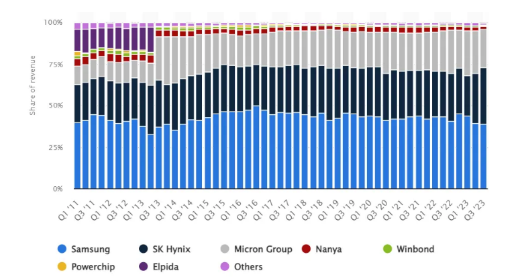

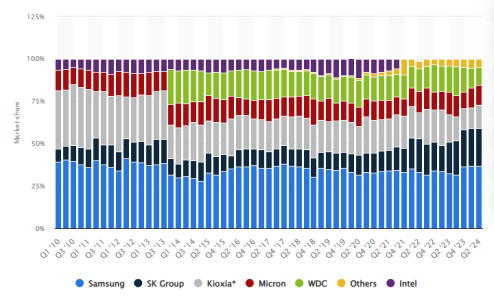

From a business perspective, there are two important things we need to consider. First of all, the market is very consolidated. For DRAM, the big three, Samsung (South Korea), Micron (USA) and SK Hynix (South Korea) have been dominant for the past ten years with no significant shifts in market share. The NAND market is slightly less consolidated as there are also Western Digital (USA) and Kioxia (Japan) as important industry players.

Source: Statista

Source: Statista

The second important aspect is the notorious cyclicality of the industry. The memory market is quite commoditized where memory has a price that can fluctuate quite significantly, depending on the supply and demand. Thus, we can observe very inconsistent growth rates and margins throughout history.

Source: Refinitiv, Micron Financials

High Bandwidth Memory (HBM) as a Turning Point in the Industry

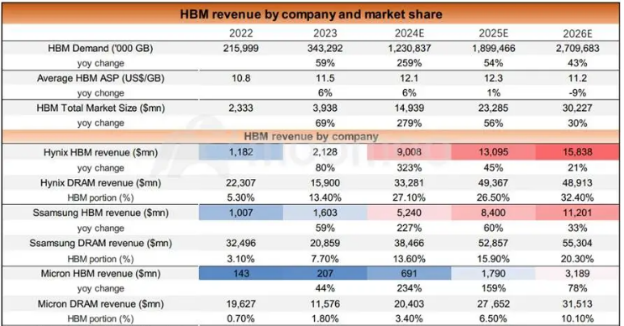

HBM is a type of DRAM that is used in AI applications. It has been very popular due to the recent explosion of generative AI. For the past couple of years, SK Hynix was the only HBM supplier. At that time, Micron and Samsung were fine with SKH dominating that market because it was a very niche product initially. HBM remained profitable even when DRAM was at a loss during the big memory price drop two years ago, thus proving that HBM is not as cyclical as traditional DRAM. After they saw the profit potential from AI, along with the non-cyclical nature, Samsung and Micron decided to switch their strategy towards ramping up HBM. The growth rate of this segment will be above 50% for the coming years, in line with the growth rate of data center chips (see NVDA and AMD).

Source: China Renaissance Securities

Non-HBM DRAM supply-demand outlook

As mentioned before, it is challenging to predict the growth rates of the memory business due to its cyclical nature. Throughout history we have observed negative growth rates, caused by oversupply, leading to sharp price decreases. However, now there are good reasons to see more sustainable long-term growth mostly due to the following factors:

1) HBM will become a more significant part of these companies’ revenue. And HBM is non-cyclical in nature.

2) As more production capacity will be allocated to HBM (HBM requires three times more wafers than a normal DRAM), there will be a lower chance of memory over-supply, hence lower chance of price swings.

3) As there are very few players controlling the market, combined with the high barriers of entry (due to the high technical complexity of the industry), the chance of new market entrants that can cut down prices will be very low.

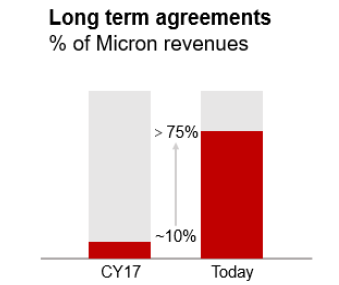

4) The general transition from short-term customer contracts to long-term ones. For example, Micron currently derives 75% of its revenue from long-term agreements vs just 10% a decade ago.

Source: China Renaissance Securities

About Micron

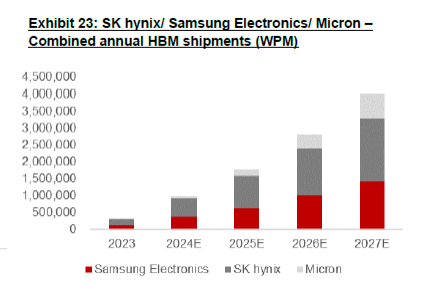

Currently, MU is trailing behind SK Hynix but ahead of Samsung in the development of the HBM business. SK Hynix was the first company to start working on HBM, thus, they already have a certain technological advantage. Also, a higher proportion of the SK Hynix revenue mix is from HBM. Both SK Hynix and Micron will benefit more from the growth of HBM. In contrast, Samsung still faces engineering hurdles as Nvidia has yet to approve their HBM chips.

As the main American player in this industry of such importance, MU has solid backing from the US Government. In April 2024, Micron was offered a direct government grant of up to US$6.14bn to support the construction of two advanced DRAM mega-fabs in New York state and a fab in Idaho state for mass production of DRAM. Additionally, Micron would obtain loans of up to US$7.5bn and qualify for investment tax credits from the US Treasury.

Finally, we have the TSMC factor. The Taiwanese firm is an important supplier of Micron, while Samsung is mainly integrated.

Source: Goldman Sachs, Moomoo

Valuation

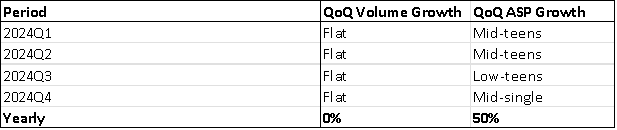

MU revenue growth for 2025 will be driven by restricted supply and healthy increase in ASP.

Source: TradingKey

In terms of profitability, the last quarter’s gross profit margin stood at 36% and the direction is pointing upwards. With the increasing role of a high-value product in the face of HBM within the revenue mix and the ability to raise prices, the GPM can head towards mid-40%.

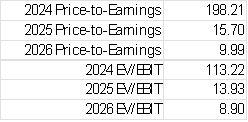

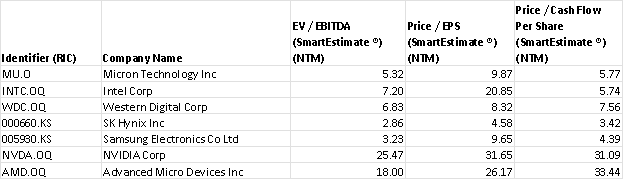

MU is traded at 16 times its earnings, which is very similar to SK Hynix’s multiple. We don’t believe the memory chip stocks should be valued as generously as NVDA, as NVDA has a strong software element that justifies the high multiple. However, 25x 2025E earnings seems a reasonable value for MU, giving it a target price range of USD130.00-160.00 (30%-60% upside).

Source: Goldman Sachs, Moomoo

Source: Refinitiv