Nvidia's Outlook: Short-Term Dip vs. Analyst Bullishness and Long-Term Gains

Historical financial result review

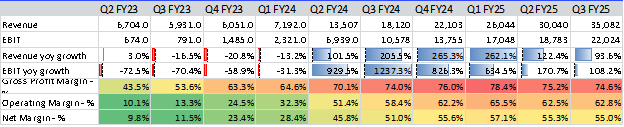

We've observed that NVIDIA's revenue and EBIT have both experienced year-over-year and quarter-over-quarter growth, albeit with a deceleration in year over year growth rates. For instance, the revenue growth rate has slowed from 205.5% in Q3 FY24 to 93.6% in Q3 FY25, and the EBIT growth rate has dropped from 1237.3% in Q3 FY24 to 108.2% in Q3 FY25. Concurrently, NVIDIA's gross profit margin (GPM) and operating profit margin (OPM) had been rapidly increasing, reaching peaks of 76%, 62.2%, and 55.6% respectively before Q1 FY25, and have since gradually declined starting from Q2 FY25.

Quarterly result overview

Source: Routers, Tradingkey.com

Therefore, Q2 FY25 marked a turning point, as the company's performance post this quarter indicated a slowdown in revenue growth and a decline in profit margins. We observed the stock price and market consensus expectations for the next three fiscal years surrounding the release of this earnings report and found that:

1) Following the Q2 FY25 earnings release, the stock price declined by 2.1% and 6.4% on Aug 28th and 29th, 2024, respectively. This aligns with the deceleration in revenue growth, indicating that the market has factored in the company's growth potential.

2) The EBIT growth rate for the next three years is expected to gradually decline from 146% to around 20%, which is consistent with the current quarterly EBIT trend.

3) Analysts have raised their revenue expectations post-earnings release, reflecting a positive outlook on NVIDIA's future. Specifically, the EBIT forecast increased by 4.1-5.1% for the next two years, and the target price rose by 5.2% within the two days.

Year over year EBIT growth after Q2 earnings release

Source: Routers, Tradingkey.com

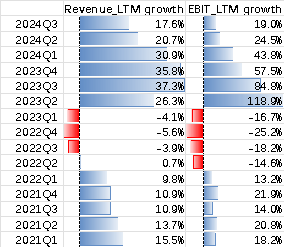

We employed a relatively conservative DCF model to calculate its intrinsic value. Within two days following the Q2 earnings release (Aug 28-29, 2024), the average revenue growth rate for the next seven years showed slight fluctuations, while operating profit margin slightly increased. The target price range saw an increase of 22.6%-23% in the two days following the Q2 release, as compared to the day prior to the earnings announcement, aligning broadly with the year-over-year changes in revenue and EBIT for the 2Q FY25 LTM period (Revenue_LTM: 20.7%, EBIT_LTM: 24.5%).

The TP (DCF) is roughly calculated as EBIT_LTM * (EBIT growth) / (discount rate), with the new TP reflecting changes in EBIT_LTM and EBIT growth / (discount rate). This time, the TP adjustment was primarily due to LTM changes, suggesting that the EBIT growth rate has been factored in with a smaller impact on valuation.

DCF model may not be well-suited for a stock with such a high PE ratio. A method for high PE stocks using DCF is to compare the percentage changes in the target price range output from the model, based on estimates before and after the earnings release, and then apply that percentage to the stock's actual price to derive a new target price. With the closing price at $128.3 the day before the earnings announcement, the resulting target price range is approximately $157.3-157.8.

Pre- and post-Q2 earnings release DCF results

Source: Tradingkey.com

Predictions for Q3 FY25 based on the same pattern

1) Following the Q3 FY25 earnings release, the stock price fell by 0.76% on Nov 20th and then rose by 0.53% on Nov 21st, 2024. Overall, the decline is in line with the deceleration in revenue growth, indicating that the stock price already reflects high market expectations.

2) The EBIT growth rate for the next three years is anticipated to gradually decrease from 153% to approximately 21.5%, aligning with the current quarterly EBIT trend. Compared to the growth rate in Q2, we observe a sequential increase in both annual and two-year average growth rates quarter-over-quarter, reflecting the market's optimistic expectations.

3) Also analysts have raised their revenue expectations, showing a positive outlook on Nvidia's future. Specifically, the EBIT forecast increased by 3.1-8.2% for the next two years during these two days, and the target price rose by 5.2% within the two days.

Year over year EBIT growth after Q3 earnings release

Source: Routers, Tradingkey.com

Following the release of this earnings report, we calculated the target price movement using the same method as before, and the results are shown in the figure below:

Pre- and post-Q3 Earnings release DCF results

Source: Tradingkey.com

The target price range increased by 31.9%-35.5% compared to the day before the earnings announcement. This aligns with the year-over-year changes for the 3Q FY25 LTM period, where Revenue_LTM grew by 17.6% and EBIT_LTM by 19%. This time, the EBIT growth rate is also a contributing factor, that is, analysts have raised their year-over-year EBIT growth rate forecasts.

Quarterly revenue and EBIT long-term moving average changes

Source: Routers, Tradingkey.com

Why analyst are so optimistic about NVDIA’s future?

1) Solid financial performance: The company has outperformed expectations on revenue, earnings, and guidance. Plus, with its competitive edge, the new Blackwell product could help Nvidia expand its lead from training to the inference market. Also despite the anticipated decline in gross margin over the next few quarters, it is expected to rebound following the ramp-up of Blackwell.

2) Optimistic industry perspective: Is the market's appetite for Nvidia chips really that strong? We'd say yes, considering: 1) The global chip market is projected to reach $629.8 billion in 2024, a 18.8% increase from the previous year, which is higher than the 16.8% growth forecasted a year ago. 2) Foxconn's construction of the world's largest plant for Nvidia's GB200 chips in Mexico indicates that companies along the supply chain are optimistic about the future, anticipating a sustained demand for Nvidia's products. 3) Having ample orders on hand now: Blackwell's GPU production for the next 12 months is fully booked.

3) Expanding capabilities and innovative products: Blackwell's mass production kicks off in Q4 FY25, with anticipated demand outstripping supply in the upcoming quarters. This should bolster revenue and potentially back the market's 8.2% EBIT increase forecast for FY3 (FY2027).

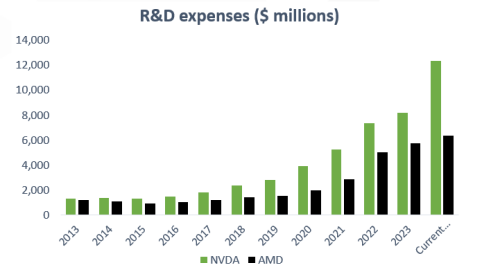

4) The market seems to have reached a consensus on the broad prospects of AI applications, attracting a large number of new entrants to the industry. Nvidia needs rapid product iteration capabilities and innovation capabilities. We believe Nvidia has a sufficient moat: that is, it continues to increase R&D investment, such as R&D expenses being twice that of AMD; it continuously launches products with better performance and higher quality, such as Blackwell; and it has more technical and talent accumulation compared to new entrants like Google.

R&D expense comparison

Source: cnBeta.COM, Tradingkey.com

5) Sufficient cash: We've observed that Nvidia has ample cash and generates significant cash flow from operations, which is more than sufficient to cover its capital expenditure and dividend payments. From a return perspective, it's a solid investment.

Quarterly cash flow update

Source: Routers, Tradingkey.com

6) Nvidia's stock price exhibits a significant positive correlation with the trend of Bitcoin: previously, the demand for Bitcoin has driven the demand for Nvidia's chips, thereby boosting the stock price. The current positive expectations in the Bitcoin market, combined with the development of large AI application models, will have a positive impact on the stock price.

Source: MacroMicro, Tradingkey.com

Our view on Nvidia

1) Based on our analysis, despite market concerns, we have solid reasons to expect that its revenue and earnings will not only grow but also surpass estimates in the near term. The company is well-capitalized to fuel its development and provide returns to shareholders. Additionally, Nvidia's P/E ratio is not excessively high but its growth rate is high, and its ROE is quite high, leading us to believe that there is potential for the target price to rise.

Peer comparison table

Source: Routers, Tradingkey.com; date as of 22 Nov 2024

2) Our TP calculation, mirroring Q2's method, yields $193.9-$199.2. However, we think this is overestimated. The decline in both current and forecasted EBIT growth rates year-over-year, likely due to a high base effect, contrasts with our DCF model's assumption of sustained FY3 (FY2027) growth rates, that is, we believe the target price should below $193.

Above all, We believe that the stock price has strong supportive information to back its rise, but it should be below $193.

.jpg)