Deutsche Bank Posts Higher Profit and Bad Debts For Q3 2024

TradingKey - In the European investment banking world, German heavyweight Deutsche Bank AG (NYSE: DB) has a stellar reputation. While it can’t compete with its American peers in terms of scale, Deutsche Bank also has other financial services offerings like an asset management arm as well as private bank.

Established in 1870, Deutsche Bank was a giant in the investment banking world in the period immediately before the Global Financial Crisis (GFC) of 2007-2008. Since then, amid many issues during the 2010s, the bank has scaled back its ambitions.

On Wednesday (23 October), before European markets opened, Deutsche Bank reported its latest Q3 2024 results. Here’s what bank stock investors, as well as anyone who’s interested in the fortunes of the European economy, should know about the latest numbers.

Bad debt provisions indicate European weakness

While Deutsche posted a 39% year-on-year increase in net profit for Q3 2024 to €1.7 billion, the headlines around the earnings were dominated by less-than-positive news. That’s because Germany’s largest lender put aside more money for expected debts that will go bad.

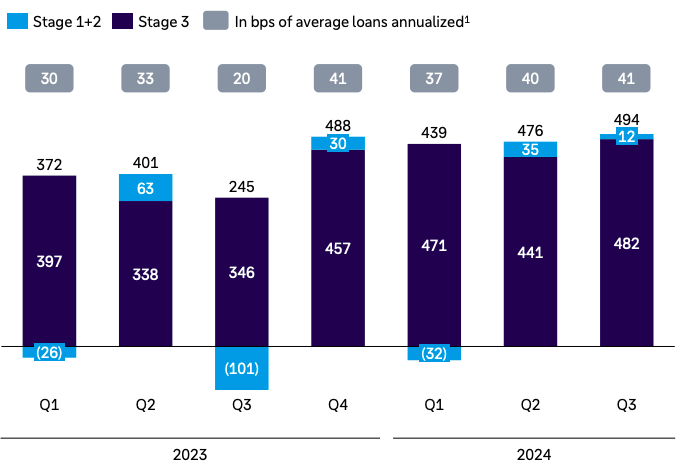

This higher “debt provisioning”, as it’s named in the banking world, is now set at €1.8 billion (or roughly 0.38% of its entire loan book) for the whole of 2024. This provision for credit losses was up substantially from the 0.30% management had guided for earlier this year.

Deutsche Bank’s provision for credit losses (in € millions)

Source: Deutsche Bank Q3 2024 earnings presentation

That bad debt provision level has remained elevated since trending higher in Q3 2023 and, based off the 2024 estimate from management, then the bad debt provision for Q4 2024 should come in around €400 million – down slightly from the Q3 2024 figure recorded. Yet the market wasn’t impressed with the fact that Deutsche Bank’s credit provisions in Q3 2024 hit their highest level in over four years.

Indeed, Deutsche CEO Christian Sewing attempted to reassure investors by stating that the increase in provisions was only “temporary”. Deutsche CFO James von Moltke also said on the earnings call that the higher credit provisions partially reflect integration of retail lender Postbank into the broader Deutsche group.

As the company revealed in its earnings release, the credit provisions for commercial real estate (CRE) were already coming down again.

Lower rates weigh on lending

Like all banks, Deutsche is having to confront lower interest rates that are impacting its lending businesses. This was obvious in Q3 2024 as lower rates meant that revenue at its corporate bank fell 3% year-on-year while revenue at its private bank also declined marginally by 1% versus a year earlier.

It was the firm’s investment banking division that drove growth during the quarter, as it grew its top line by 11% year-on-year to €2.5 billion.

The backdrop of weaker growth in Europe has seen the European Central Bank (ECB) cut interest rates for a third time this year, reducing the key deposit rate to 3.25% in mid-October. That lower-rate environment is less accommodating to European banks versus their US peers, where the Federal Reserve has only cut interest rates once so far in 2024.

Overall, Deutsche Bank has been committed to returning capital to shareholders via both share buybacks and dividends. It reaffirmed its dividend guidance of €0.68 per share for FY 2024 and €1.0 per share for FY 2025. That would bring its compound annual growth rate (CAGR) to 50% from 2022’s dividend per share (DPS) level.

However, a low Return on Tangible Equity (RoTE) of just 6% for 9M2024 suggests the bank still has work to do in growing its recurring, fee-earnings businesses like wealth management. Deutsche Bank’s New York-listed shares ended the day down 1.4% but they have gained 27.3% so far in 2024.