Asset Allocation in Global Developed Markets: Bullish on Japanese Stocks

Executive summary

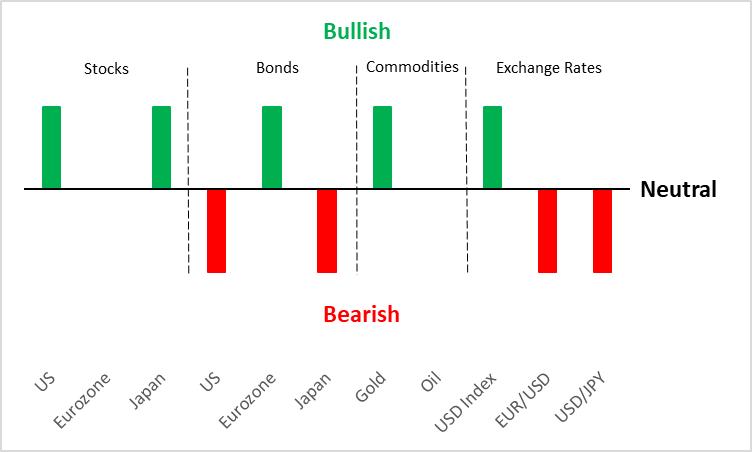

Short-term (0-3 months) view

Source: Tradingkey.com

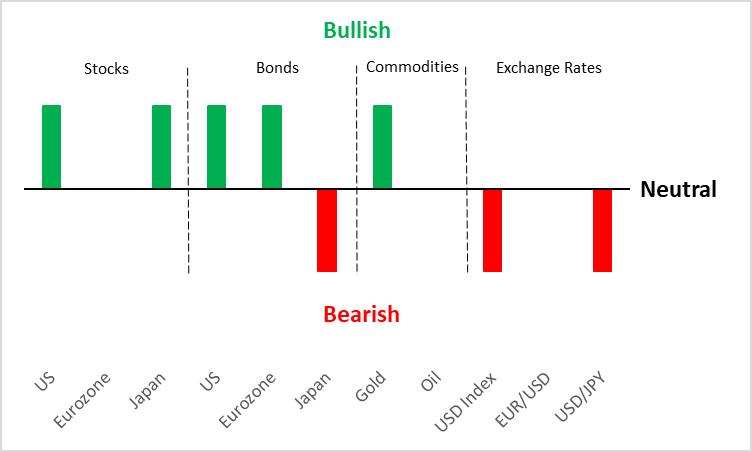

Medium-term (3-12 months) view

Source: Tradingkey.com

1. Macroeconomics

1.1 US

On 18 December, the Fed cut interest rates by 25bp, lowering the policy rate to 4.25%-4.5%. While the rate cut met expectations, Fed Chair Powell delivered hawkish remarks during the press conference. Additionally, the Fed raised its GDP and inflation forecasts while lowering its unemployment rate forecast, indicating that the pace of rate cuts in 2025 may be slower than previously anticipated.

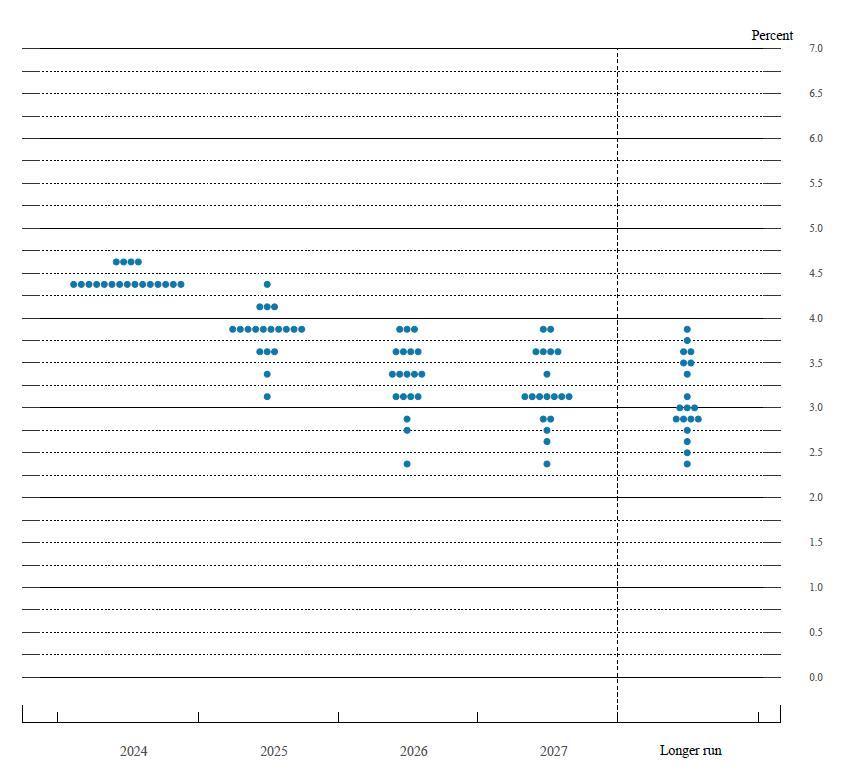

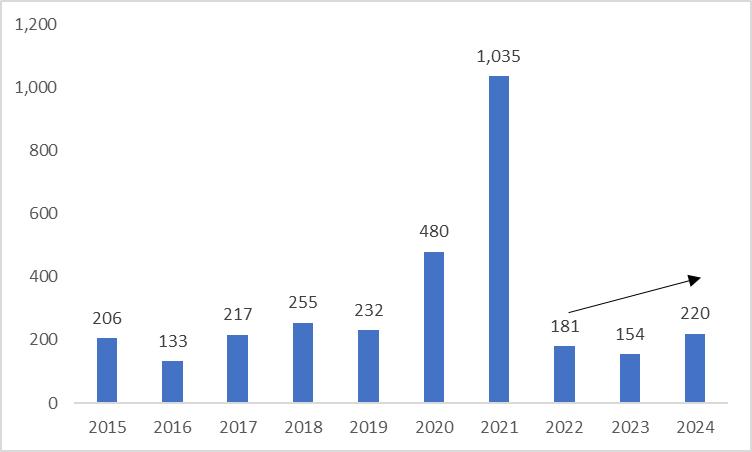

According to the Fed’s Dot Plot, the September forecast indicated four rate cuts for next year, but the December update reduced this number to two (Figure 1.1.1). Besides GDP growth and PMI data showing a persistent sign of resilience, the number of IPOs has reached 220 in 2024, more than that in 2022 and 2023 (Figure 1.1.2). Looking ahead, the US economy is expected to show a continued strong trend in the short term, bolstered by Trump's tax cuts and other related policies. However, given the Fed’s hawkish monetary stance, we maintain our view of an economic slowdown in the US in the medium term. We project GDP growth to decelerate to 2.2% in 2025, slightly above the Fed's forecast.

Figure 1.1.1: FOMC’s midpoint of target range for the federal funds rate (December 2024)

Source: Fed, Tradingkey.com

Figure 1.1.2: US number of IPOs

Source: Refinitiv, Tradingkey.com

1.2 Eurozone

Since the start of this year, the Eurozone economy has experienced a moderate recovery. Although GDP growth in the first three quarters of 2024 outpaced that of the second half of 2023, it remained significantly lower than the levels seen in 2021 and 2022. Looking ahead, weak domestic demand, fiscal consolidation in France and Italy, and the EU's fiscal deficit controls are likely to weigh on the Eurozone economy in 2025. Additionally, tariff measures imposed by the Trump administration may further heighten uncertainty surrounding the Eurozone's economic outlook.

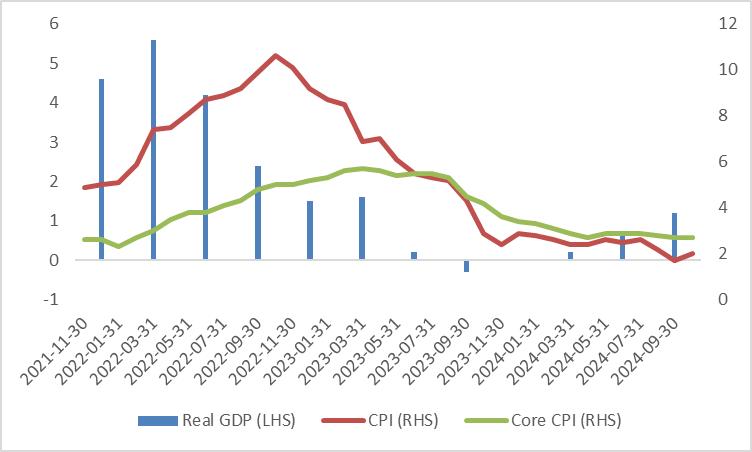

On the inflation front, both CPI and core CPI have declined sharply from their peaks in 2022-2023. Core CPI is projected to fall further, approaching 2% by the end of next year. Reflecting these dynamics—sluggish growth recovery and declining inflation (Figure 1.2)—the European Central Bank (ECB) cut interest rates by 25bp on 12 December. We anticipate that the central bank will implement an additional 4-6 rate cuts (each by 25bp) in 2025 to support economic stability.

Figure 1.2: Eurozone real GDP and CPI (%)

Source: Refinitiv, Tradingkey.com

1.3 Japan

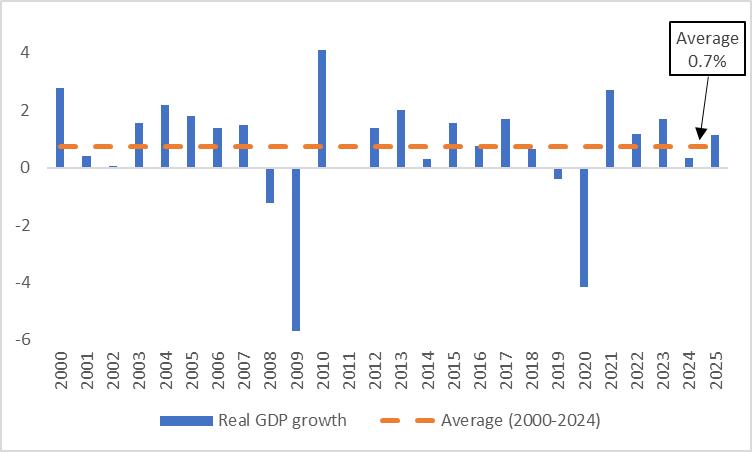

The Japanese economy has weakened since the beginning of this year, impacted by sluggish consumption, insufficient external demand, and geopolitical risks. However, a recovery is anticipated in 2025. According to IMF forecasts, Japan’s real GDP growth is expected to reach 1.1% next year, significantly higher than 0.3% this year and the 0.7% average since 2000 (Figure 1.3). Two key factors underpin this recovery:

· Rising Wages and Improved Consumption: Japan’s nominal average wage grew by 5.6% this year, driven primarily by the 2024 Shuntō wage negotiations. With strong backing from Prime Minister Ishiba Shigeru, wage growth is projected to exceed 5% in the 2025 Shuntō. Assuming inflation remains around 2%, real wage growth could surpass 3%, potentially boosting consumption. In fact, household consumption has already shown signs of improvement since Q2 2024, a trend we expect to continue.

· Economic Stimulus Measures: In November, the Japanese government unveiled a 21.9 trillion yen economic stimulus plan, which includes subsidies for low-income families, an increase in the tax-free wage threshold, and support for high-tech industries such as artificial intelligence and semiconductors. These supportive fiscal policies are likely to further contribute to economic growth.

On the inflation front, Japan’s headline CPI and core CPI (less fresh food) increased to 2.9% and 2.7% in November from 2.3% in October, respectively. Combined with robust nominal wage growth, this is expected to sustain upward pressure on consumer prices in the future. Although the Bank of Japan (BoJ) has taken a cautious approach to monetary policy normalization, holding the policy interest rate unchanged in December, we anticipate that the BoJ will raise interest rates in the coming quarters, supported by a favourable economic outlook and elevated inflation levels.

Figure 1.3: IMF forecasts of Japanese real GDP growth (%)

Source: IMF, Tradingkey.com

2. Stocks

2.1 US

We first recommended going long on US stocks in our report, The Impact of the US Election on Major Asset Classes, published on 29 October. We reiterated our bullish stance in the subsequent report, Asset Allocation in Developed Markets: Continue to Be Bullish on US Stocks, published on 26 November. Since our initial recommendation, the S&P 500 index rose by 4.4% to 6090 as of 6 December. However, due to Powell’s hawkish speech and the Fed’s slower rate cut stance, the stock index has dropped to 5974. In this report, we see the recent significant drop as a temporary market correction and maintain our positive outlook on US stocks for the following reasons:

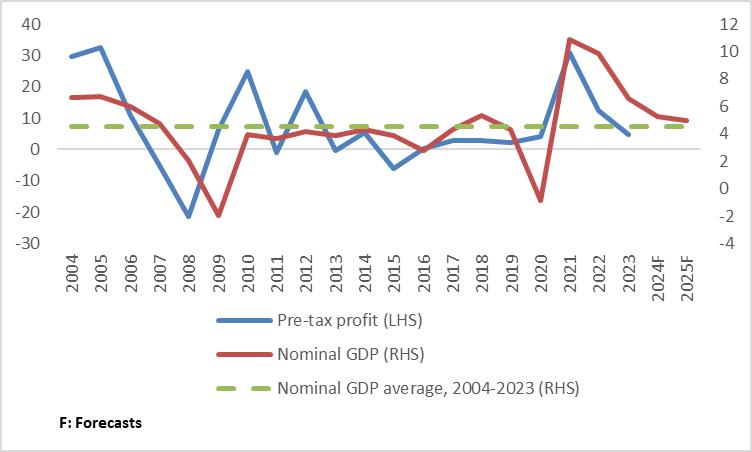

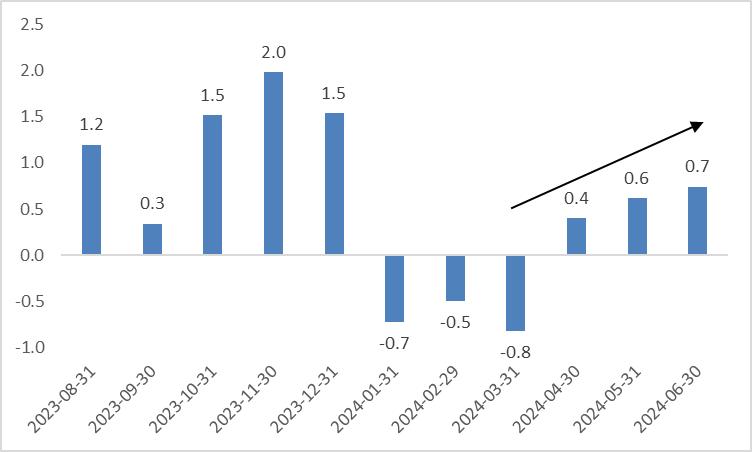

· Earnings Growth Linked to Nominal GDP: US corporate pre-tax earnings are positively correlated with nominal GDP growth. While we expect US nominal GDP growth to decelerate to 5% in 2025, this figure remains above the 20-year historical average (Figure 2.1.1). Additionally, excluding inflation, the month-on-month real growth rate of S&P 500 earnings per share (EPS) has been accelerating since turning positive in April (Figure 2.1.2). We anticipate continued EPS growth, coupled with a robust return on equity (ROE), which suggests further upside potential for US stocks.

· Supportive Monetary Policy: In the medium term, even as the influence of Trump Trade diminishes, the ongoing interest rate cut cycle is expected to support investment returns for US stocks.

On the other hand, US stocks face challenges, particularly from high valuations. Currently, the price-to-earnings (P/E) ratio of the S&P 500 is above the 90th percentile of its historical range. This has elevated valuation warrants caution, and investors should remain vigilant.

Figure 2.1.1: US company profits vs. nominal GDP growth (%)

Source: Refinitiv, Tradingkey.com

Figure 2.1.2: S&P 500 real EPS growth (%)

Source: Refinitiv, Tradingkey.com

2.2 Eurozone

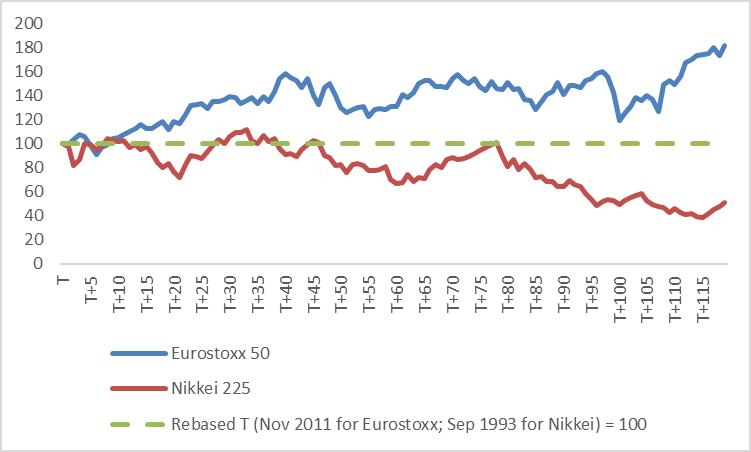

The Eurozone is expected to enter a period of low interest rates next year. Will this lead to a boom in Eurozone stocks? To explore this question, we compare the performance of the Eurozone and Japanese stock markets during similar periods.

Historically, the Eurozone entered a low-interest rate era in November 2011, one year after the European debt crisis erupted. Japan began its low-interest rate era in September 1993, three years after its asset bubble burst. Over the following decade, Eurozone stocks performed well, while Japanese stocks endured a prolonged bear market (Figure 2.2). The similarity of the two markets is that both attracted foreign capital inflows during their respective low-interest rate periods. However, there were key differences:

· Private Sector Behaviour: The Eurozone private sector increased its stock investments, whereas Japan’s private sector reduced theirs.

· Government Intervention: The Eurozone government did not directly intervene to rescue the market, while the Japanese government actively participated in market rescue efforts.

From historical trends and capital flow dynamics, it is evident that in developed markets, private sector investment plays a pivotal role in driving stock market strength. Stabilizing internal risk appetite is thus critical for sustained equity market performance.

Looking ahead, whether the Eurozone stock market in this low-interest rate period mirrors its prosperity of the 2010s or the stagnation of Japan in the 1990s will depend largely on the effectiveness of Eurozone fiscal and monetary policies. If these policies successfully create a supportive environment for private sector investment, the Eurozone stock market could thrive. However, if policies fail to stimulate economic growth, the market may underperform. Given the uncertain outlook, we adopt a neutral rating for Eurozone stocks and remain cautious about downside risks.

Figure 2.2: Eurozone vs. Japanese stock performance during low-interest rate periods (monthly data)

Source: Refinitiv, Tradingkey.com

2.3 Japan

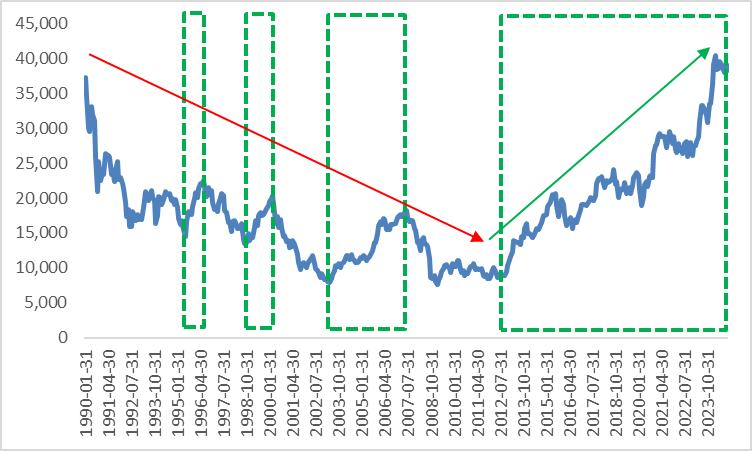

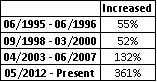

Since the Japanese economic bubble burst in 1990, the stock market endured the "Lost Decades" (1990–2010). During this 20-year period, Japanese stocks experienced a general downward trend, punctuated by three temporary bull markets. However, since May 2012, Japanese stocks have entered a sustained and significant bull market (Figures 2.3.1 and 2.3.2). Although the drivers behind these four bull markets were different, they share common contributing factors: 1) Domestic policy shifts; 2) Domestic economic improvements; 3) Overseas policy shifts; and 4) Overseas economic improvements.

Using history as a guide, let us examine the current state of the Japanese stock market.

· Domestic Factors: While expansionary fiscal policy and tightening monetary policy may counterbalance each other, Japan’s economic growth in 2025 is projected to significantly outpace that of 2024.

· Overseas Factors: Globally, central banks in major economies have entered an interest rate cut cycle, improving global financial conditions. The US economy remains resilient, while China's economy is expected to recover under the influence of a series of stabilization policies.

Given these dynamics, Japanese stocks are likely to sustain their current upward trend in the short to medium term.

Figure 2.3.1: Nikkei 225

Source: Refinitiv, Tradingkey.com

Figure 2.3.2: Nikkei 225 performance during the bull markets

Source: Refinitiv, Tradingkey.com

3. Bonds

3.1 US

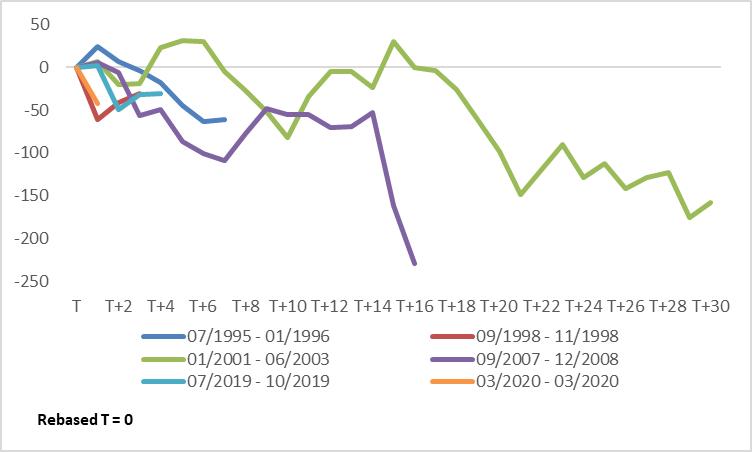

The 10-year US Treasury yield can be analysed by breaking it into three components: the 3-month real yield, CPI, and the term premium. The short-term real yield is primarily influenced by the Fed’s monetary policy. The CPI is shaped by factors such as money supply, wage growth, economic conditions, and external shocks. The term premium reflects the supply and demand for long-term US Treasury bonds and is mainly affected by economic growth. Since 1995, there have been six interest rate cut cycles (excluding this round):

· July 1995 – January 1996 and September 1998 – November 1998: The US economy faced minimal internal and external shocks, achieving a soft landing.

· January 2001 – June 2003 and September 2007 – December 2008: The bursting of the internet bubble in 2001 and the 2007–2008 Global Financial Crisis caused market panic and economic recessions.

· July 2019 – October 2019: Persistent disinflation raised concerns about the economic outlook.

· March 2020: The outbreak of the pandemic severely disrupted the global economy, exacerbating supply constraints.

Historically, in five of the six cycles, the term premium increased due to economic difficulties (1995 being the exception). However, the decline in short-term real yields, either alone or combined with a reduction in CPI, outweighed the rise in the term premium, leading to a drop in the 10-year Treasury yield across all six cycles (Figures 3.1.1 and 3.1.2).

For this round of rate cut cycle, in the near term, US yields may rise due to factors such as “Trump Trade”, re-inflation, and a stronger US dollar. However, in the medium term, this interest rate cut cycle is likely to reduce short-term real yields, following the pattern of the past six cycles. Inflation is expected to maintain its downward trajectory, and as the US economy is projected to achieve a soft landing, the rise in the term premium should remain limited. As a result, while the 10-year Treasury yield may experience a short-term increase, we expect it to decline in the medium term.

Figure 3.1.1: 10-year US treasury yield during interest rate cut cycles (bps, monthly data)

Source: Refinitiv, Tradingkey.com

Figure 3.1.2: 10-year US treasury yield breakdown during interest rate cut cycles (change, bps)

Source: Refinitiv, Tradingkey.com

3.2 Eurozone

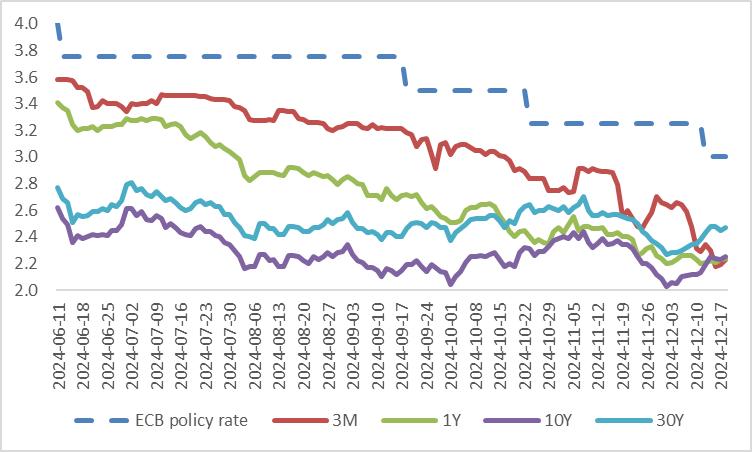

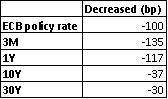

Since 12 June, the ECB has entered a rate-cutting cycle, reducing interest rates by a total of 100bp so far. This has led to a decline in German government bond yields across all maturities. Notably, the drop in short-term (front-end) yields has been more pronounced than that in long-term (back-end) yields (Figures 3.2.1 and 3.2.2). The disparity arises because front-end yields are primarily influenced by changes in policy rates, while long-end yields also reflect broader economic fundamentals, which tend to respond more gradually to policy rates.

Looking ahead, the ECB is expected to continue cutting rates significantly, likely causing a downward shift in the entire German yield curve. Front-end yields are expected to decline more sharply than long-end yields, resulting in a steeper yield curve. Yields on French and Spanish government bonds are also likely to decline alongside German yields. However, French-German bond spreads may widen due to heightened political uncertainty in France.

Figure 3.2.1: ECB policy rate vs. German government bond yields (%)

Source: Refinitiv, Tradingkey.com

Figure 3.2.2: ECB policy rate vs. German government bond yields from 11 June 2024 (decreased, bps)

Source: Refinitiv, Tradingkey.com

3.3 Japan

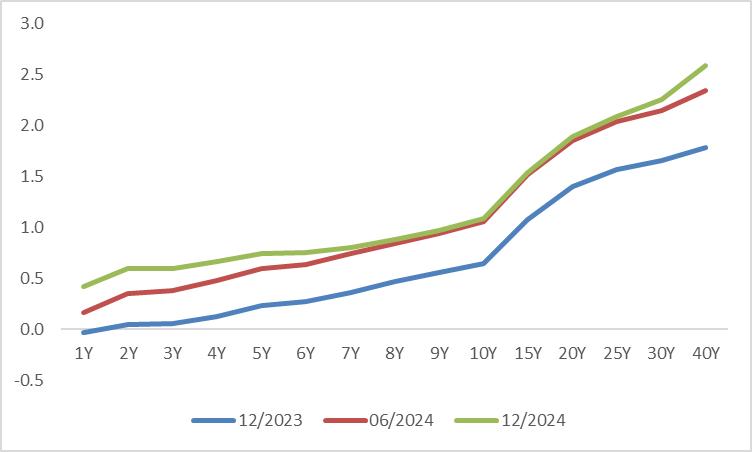

Amid Japan's economic recovery, inflation remaining above 2%, and the BoJ’s ongoing monetary policy normalization, we expect Japanese government bond (JGB) yields to continue rising in 2025, consistent with this year’s trend (Figure 3.3). In terms of front-end yields, these are more directly influenced by changes in policy interest rates and are likely to experience a more pronounced increase. In terms of long-end yields, gains in long-term rates are expected to be more limited. In the second half of 2024, many insurance companies indicated plans to increase their investments in domestic bonds, particularly 20- to 30-year JGBs. This stronger demand is expected to exert downward pressure on long-end yields. As a result, we anticipate that the JGB yield curve will likely flatten in the coming quarters.

Figure 3.3: Japanese government bond yield curves (%)

Source: Refinitiv, Tradingkey.com

4. Commodities

We remain bullish on gold and maintain a neutral stance on crude oil. Several factors continue to support gold prices: 1) The Fed’s rate-cutting cycle; 2) High levels of US government debt; 3) Continuous inflows into gold ETFs; 4) The People's Bank of China's (PBOC) resumption of gold purchases in November. These dynamics collectively create a favourable environment for gold investment.

US crude oil production is expected to decline slightly in 2025 compared to 2024. Coupled with OPEC's decision to postpone its production increase, the resilience of the US economy, and the recovery of the Chinese economy, a sharp decline in oil prices appears unlikely. For more detailed analysis, refer to our reports “Gold vs. Bitcoin: Which Is the Better Investment in 2025? published on 16 December” and “Commodities Outlook: Macroeconomic Policies Will Improve Commodity Demand released on 12 November”.

5. Exchange rates

In terms of time horizon, we are bullish on the USD Index in the short term and bearish in the medium term. Regarding specific currency pairs, we are bearish on EUR/USD and USD/JPY. As a result, we recommend taking a short position on the EUR/JPY. For more details, please refer to our report “Exchange Rate Outlook: Time to Go Short the EUR/JPY Pair published on 16 December”.