Asset Allocation in India and ASEAN-6: Bullish on Indonesian Stocks

By Jason Tang

Executive summary

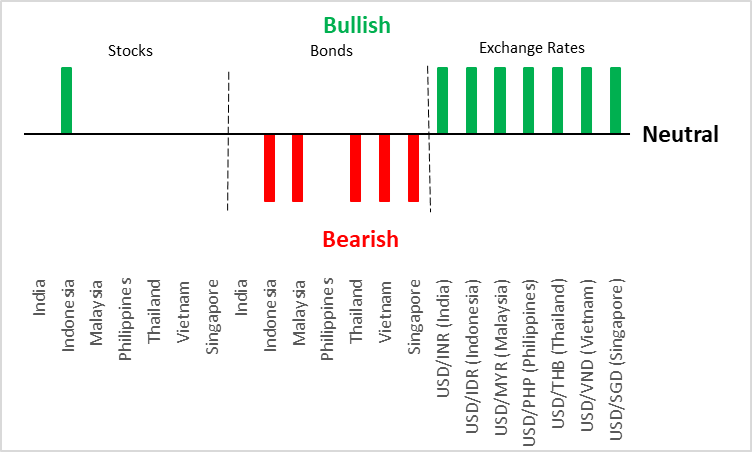

Short-term (<3 months) view

Source: Tradingkey.com

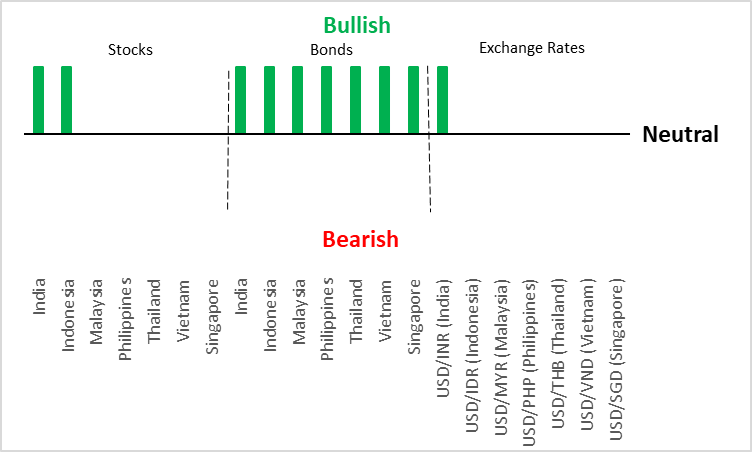

Medium-term (3-12 months) view

Source: Tradingkey.com

1. Macroeconomics

1.1 India

After several years of strong GDP growth, the Indian economic growth has moderated and the latest data has shown a mixed picture. Rural economic conditions have improved on the back of a better-than-expected monsoon. Fast-Moving Consumer Goods (FMCG) sales in rural areas have increased and this momentum is expected to continue in the near term. Higher government spending after the Indian election has boosted investment growth, and industrial credit has also grown rapidly. However, power demand and growth in mining and utilities have weakened as the weather has nominalized. While the aggregate demand in rural areas has increased, urban consumption, which accounts for two-thirds of national consumption, has recently shown a sign of weakness, mainly due to high inflation and a high base effect.

From the external perspective, the increase in the proportion of service exports has supported Indian total exports in recent years. After Trump’s election, the war in the Middle East is expected to ease. This may reduce oil prices, benefitting the oil-importing country. In addition, the US is likely to establish a stronger economic relationship with other large Asian countries, such as India and Japan, to reduce its reliance on Chinese goods.

Under the theme of "New India", the economic boom in the past few years was attributed to the development of the high-tech industries. After several years of rapid development, the growth of these industries is normalizing. Real GDP growth is gradually moving from around 8% to 6.5% (Figure 1.1.1). However, combined with a sound export environment, we believe that the slowdown in the Indian economy may not be bad news as the economy is expected to become more sustainable. In short, the Indian economy is structurally strong. Infrastructure modernization, self-reliance and "Make in India" will continue to be the pillars of Indian economic development.

Figure 1.1.1: India real GDP growth (% y-o-y)

Source: Refinitiv, Tradingkey.com

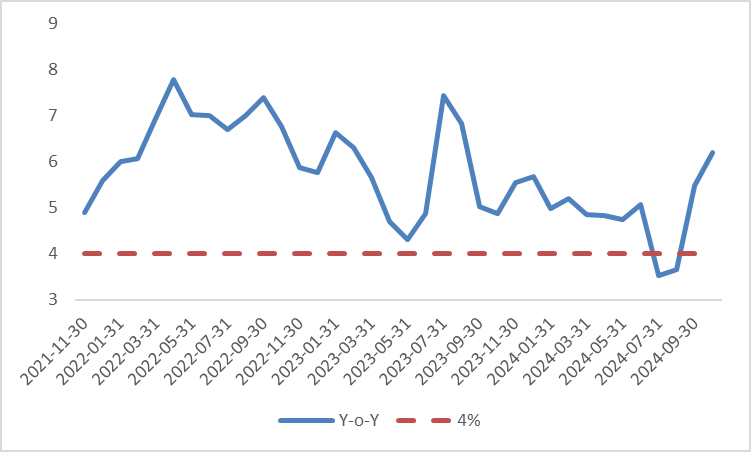

In terms of inflation, the CPI fell below 4% in the past few months, with falling spice prices being the main driving force. However, food inflation pushed up the CPI to 6.2% in October due to a sharp rise in vegetable and cereal prices (Figure 1.1.2). Despite the recent economic slowdown, the Reserve Bank of India (RBI) is unlikely to cut interest rates in December due to the central bank’s goal of keeping inflation below 4%. If food prices fall, we expect the RBI to start cutting interest rates in Q1 2025.

Figure 1.1.2: India CPI (% y-o-y)

Source: Refinitiv, Tradingkey.com

1.2 ASEAN-6

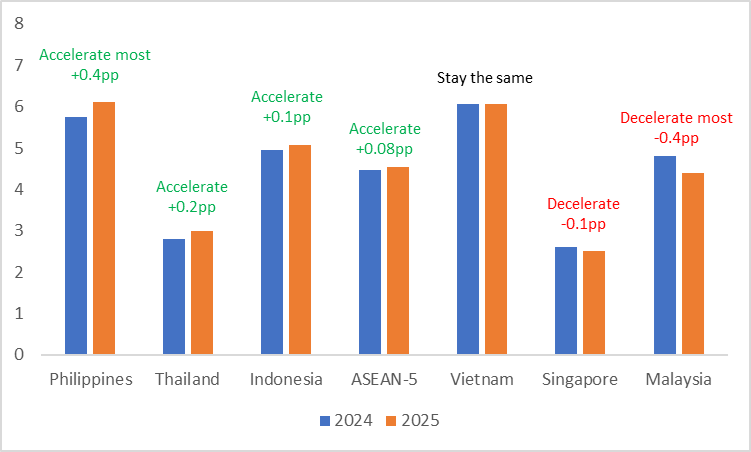

Since the beginning of this year, the ASEAN has seen continued growth in domestic demand. This, together with strong overseas demand for electronic products, has accelerated the regional economic expansion. Entering 2025, despite the rise of global trade protectionism, we believe that the ASEAN-6 economic growth will continue to show resilience. According to the forecasts of the IMF, the ASEAN-5 GDP growth will reach 4.5% next year, the same as this year. Compared with 2024, the Philippines' growth rate in 2025 will increase the most by 0.4 percentage points. Malaysia's growth rate will decrease the most, by -0.4 percentage points (Figure 1.2).

Figure 1.2: IMF ASEAN GDP forecasts

Source: IMF, Tradingkey.com

Among the six ASEAN countries, the Indonesian economy has the most advantages. It has a low dependence on the US for trade and investment, with exports to the US accounting for merely 1.7% of GDP, far lower than the other five countries. The newly established government has reduced political uncertainty and fiscal policy may remain supportive next year. Indonesian new president Prabowo has set an annual growth target of 8% by 2029. The target aims to ensure strong growth while addressing the issues of unemployment and inequality. Although the recent increase in value-added tax may weaken domestic consumption, the government's implementation of the "Free Lunch Program", expansionary public infrastructure spending and continued improvement in the private investment environment may promote economic resilience in 2025.

Malaysia's fiscal consolidation has performed better than expected, with the budget deficit being likely to narrow from 4.3% of GDP in 2024 to 3.8%. More specifically, on the one hand, the government is expected to implement stricter gasoline subsidies, expand the scope of the consumption and service tax, and charge a 2% dividend tax on large individual investors. On the other hand, Malaysia has launched its largest annual spending plan to support economic growth. Weaker exports of oil and electronic goods were the main reason for total Malaysia's exports to fall for the first time in the past six months, causing its manufacturing PMI to decrease. Looking forward, exports are expected to recover, supported by the global electronics upcycle. Private consumption may continue to grow due to the healthy labour market and higher wage growth. Investment may also maintain a strong expansion driven by large-scale infrastructure construction and industrial support plans. However, due to strong growth in 2024, the Bank Negara Malaysia (BNM) may start to cut interest rates as late as the end of 2025 or even the beginning of 2026. Therefore, we expect the Malaysian economy to grow at a relatively high rate in 2025, but lower than in 2024.

Due to stable inflation, the Bangko Sentral ng Pilipinas (BSP) took an earlier step than the Fed to start its rate-cut cycle in August this year. The BSP is expected to further cut interest rates by 25bp in December this year and 50bp next year. Since the beginning of this year, the economic growth of the Philippines has remained strong. Driven by the strong labour market, overseas remittances and consumer credit growth, private consumption has been the largest contributor to GDP growth. Meanwhile, the rebound in government consumption has also supported economic growth. The growth of investment is mainly due to the construction of large infrastructure projects. Net exports have also begun to recover since Q2 2024 due to the recovery of global goods trade. Looking forward, continued interest rate cuts may result in the 2025 growth rate being higher than in 2024.

The political turmoil delayed the implementation of the government's fiscal spending, dragging down Thailand's economic growth in the first three quarters of this year. Looking forward, we believe that the Thai economy will accelerate to recover. First, the implementation of the "Digital Wallet" scheme is expected to boost private consumption. The first phase of digital wallet funds was disbursed by the end of September, benefiting 14.55 million vulnerable individuals. The second phase of disbursement is in progress. Second, the interest rate cuts and the weakening of the Thai baht are likely to benefit exports and tourism. Third, the normalization of the fiscal budget in the new fiscal year is expected to boost government consumption and investment. The Thai government only spent 65% of the fiscal budget in FY2024. The rest is expected to be spent in the first half of FY2025. Finally, while inflation has started to pick up, the current weak economy may prompt the Bank of Thailand (BOT) to cut interest rates by 50bp next year. We expect Thai GDP growth to reach the BOT’s target of 2.9% in 2025.

With the support of fiscal policy, the steady expansion of consumption and investment has contributed to the recovery of Vietnam’s domestic demand. This, together with strong external demand, Vietnam's economic growth has accelerated since the start of 2024. At present, the State Bank of Vietnam (SBV) implements a flexible monetary policy. As the Fed has entered a rate-cut cycle, the SBV is expected to modestly cut the interest rate and reserve requirement ratio in 2025. This, combined with expansionary fiscal policies and accelerated inflows of FDI, Vietnam's GDP growth is expected to achieve the target of 7.0-7.5% set up by the Ministry of Planning and Investment (MPI) in 2025.

In the first and second quarters of this year, private consumption and investment in Singapore grew steadily. In the third quarter, the global electronics industry began to enter an upward cycle, leading to a strong rebound in Singapore's electronics production and exports. These all were the main engines of Singapore's economic growth in the first three quarters of this year. In 2025, we believe that Singapore's economy will continue to grow at a rate close to its potential. In terms of monetary policy, the Monetary Authority of Singapore (MAS) has maintained the S$NEER policy unchanged six times since April 2023. Looking ahead to 2025, based on our baseline scenario – no sudden drop in the Singaporean GDP growth – the MAS will continue to maintain the monetary policy stance unchanged.

2. Stocks

2.1 India

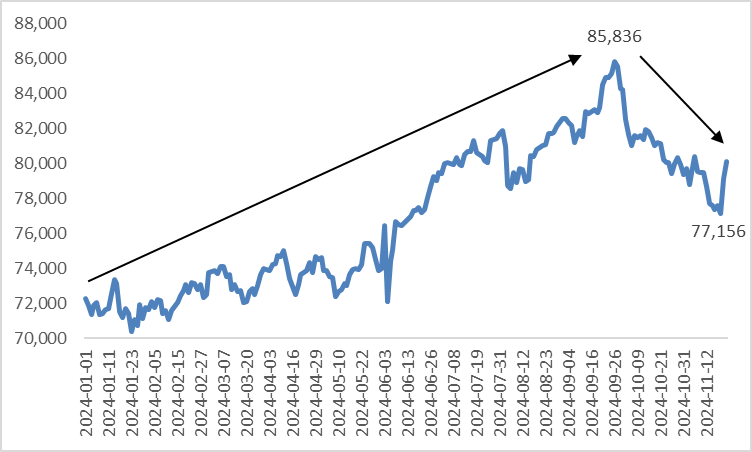

Indian stocks performed well in the first three quarters of 2024, but the prices have been on a downward trend since the end of September (Figure 2.1). Three reasons are as follows. 1) investors have taken profits after the Fed started the rate cut cycle; 2) China's economic stimulus has caused overseas institutional investors to switch from the Indian market to the Chinese. For example, foreign institutional investors in India have seen a total net outflow of about $15 billion so far this year. In October alone, the figure reached $11.2 billion; 3) Domestic consumption, especially urban consumption, has been weakening.

Looking forward, the largest headwind facing Indian listed companies is their earnings. Since 2020, the average annual earnings growth has reached as high as 25%, pushing up the stock prices. However, we expect the earnings growth rate to slow down. First, banks, the largest sector of the Indian stock market, have raised their deposit rates to attract customers’ savings, depressing their earnings. Second, the high-tech company’s earnings are expected to continue to slow down due to the normalization of the second-largest sector of the Indian market. Third, driven by the weakening of urban consumption, the earnings of the auto sector have been declining.

Despite the slowdown in earnings growth and the shift of overseas institutional investors to other emerging markets, the valuations of Indian stocks have fallen below their 5-year average after a recent market correction. In other words, the headwinds may have already been priced in. We expect the fall in the stock market to terminate, and the market may enter a stable range in the short term. In the medium term, as the Indian economy becomes more sustainable and the RBI cuts interest rates, Indian stocks are likely to rise.

Figure 2.1: BSE SENSEX

Source: Refinitiv, Tradingkey.com

2.2 ASEAN-6

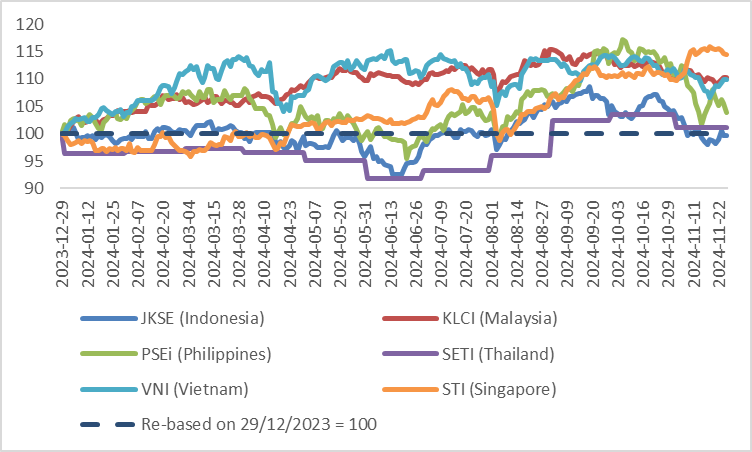

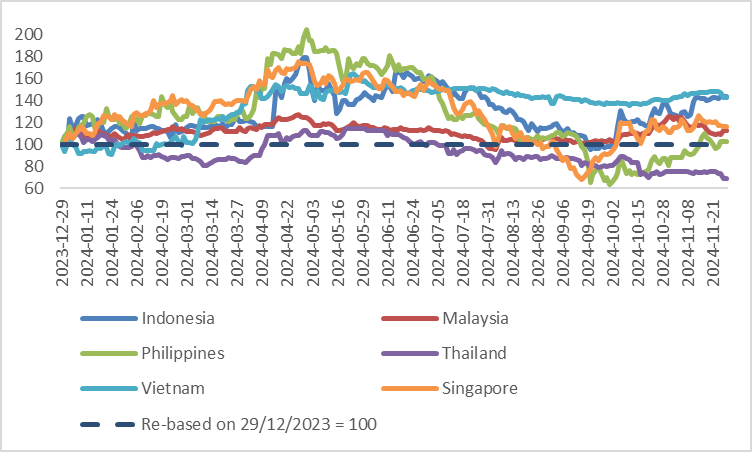

In the first three quarters of this year, the expectations of the US economy continued to switch between a "soft landing" and a "hard landing", leading to uncertainty about when the Fed would start its rate cut cycle and how much it would cut. This made investors more cautious. Except for Singapore, ASEAN stock markets have maintained net capital outflows. Since October, ASEAN stock prices have entered a downward trend due to negative external factors (Figure 2.2). Looking forward, we believe that the worst is behind us. In 2025, ASEAN stocks will be affected by internal and external factors. Externally, the resilience of the US economy and re-inflation may lead to a slowdown in the pace of the Fed’s interest rate cuts. The Trump administration is expected to increase tariffs on China, which is ASEAN's most important trading partner. As ASEAN stocks are sensitive to overseas economic conditions and capital flows, these external factors may put pressure on ASEAN stock prices. Internally, with supportive monetary and fiscal policies, the ASEAN economy is expected to perform well next year, which benefits the stock markets. Due to the offset of internal and external factors, ASEAN stocks, except Indonesia, are expected to enter a choppy market.

We are bullish on Indonesian stocks as the domestic effects may be stronger than the external. First, new President Prabowo announced that Indonesia needs to borrow more to develop the economy to achieve the 8% growth target. He can tolerate debt rising from the current 40% to 50% of GDP. Stimulating the economy through leverage benefits stock prices at least in the short term. Second, Indonesia is more dependent on its domestic demand than external. Trump's higher tariff policies may have a limited impact on the economy. Third, due to the resilience of the economy, listed companies' earnings are expected to continue to grow in 2025. Finally, the valuations of Indonesian stocks are well below their 10-year average.

Figure 2.2: ASEAN stocks

Source: Refinitiv, Tradingkey.com

3. Bonds

3.1 India

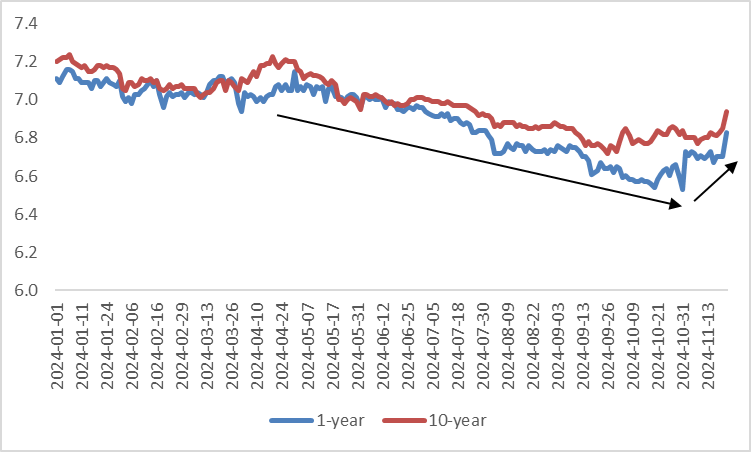

Even against the backdrop of higher US yields and the dollar, the prices of Indian government securities (Gsec) have shown resilience since late October and early November, with the 1-year and 10-year yields rising by merely 30bp and 17bp respectively (Figure 3.1). The current yields are still significantly lower than those at the beginning of this year. Looking ahead, we are neutral on Gsec in the short term due to the continued outspread of elevated US yields. In the medium term, we are bullish on Gsec. This is because while the RBI is not expected to cut interest rates in December, continued high inflation may force the central bank to start a rate cut cycle in Q1 2025, lowering Gsec yields. In addition, the RBI has suspended the sale of Gsec in the secondary market and the Indian government has repurchased a large number of Gsec maturing in FY25/26. This will reduce the net supply of Indian government bonds, pushing up prices (and driving down yields).

Figure 3.1: Gsec yields (%)

Source: Refinitiv, Tradingkey.com

3.2 ASEAN-6

US Treasury yields are an important factor affecting the yield trend of ASEAN government bonds. Our report on Asset Allocation in Developed Markets: Continue to be Bullish on US Stocks has described the reasons why we expect US yields to go up in the short term and go down in the medium term. Based on our baseline scenario of the US yields, government bond yields in the ASEAN countries are likely to follow the US to rise in the short term. In the medium term, the rise of the global trade war may force the ASEAN central banks to shift their monetary policies to a more relaxed stance. Therefore, ASEAN yields may, once again, follow the US to fall.

From the short-term perspective, the Philippines is a special case. Unlike the other ASEAN countries, whose yields are expected to increase, we believe that Philippine government bond (RPGB) yields will enter choppy trading. On the one hand, BSP Governor Remolona indicated in November that the fluctuation of the domestic currency will not affect monetary policy. This, together with low inflation, may result in the central bank cutting interest rates by another 75bp by the end of next year, making it one of the fastest rate-cut countries in the ASEAN region. On the other hand, to finance the government’s infrastructure, the net borrowing of the Philippine government is most likely to increase in FY2025. This is expected to cause the net issuance of RPGB to increase from PHP700 billion in FY2024 to PHP994 billion in FY2025. The increased net issuance will put pressure on the prices of RPGB, increasing their yield. In addition, amid the uncertainty of the external environment, overseas investors remain cautious. This has led the Philippines' foreign capital outflows to be $289 million and $175 million in October and November, respectively. Under the combined effects of positive and negative factors, RPGB yields are not expected to rise or fall sharply.

Figure 3.2: ASEAN 10-year government bond yields (bp)

Source: Refinitiv, Tradingkey.com

4. Exchange rates

4.1 USD/INR (India)

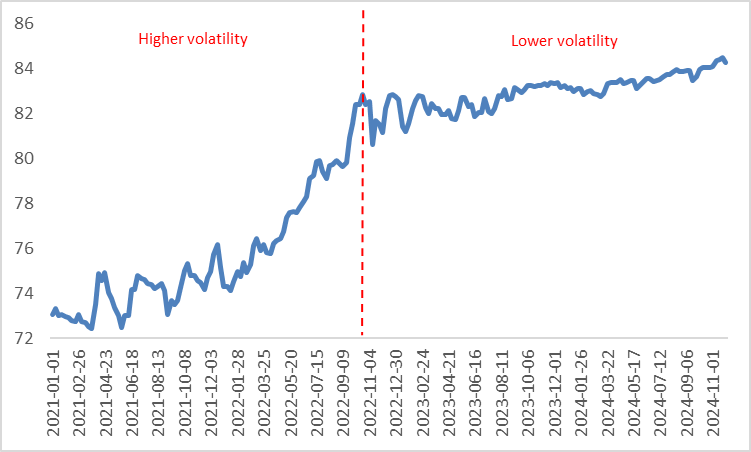

Since the end of 2022, the USD/INR has increased in a narrower range (Figure 4.1). Compared to the pair before the end of 2022, the lower volatility may be attributed to the intervention of the RBI to accumulate foreign reserves. Looking forward, we believe that the USD/INR may continue the current trend to go up, with low volatility. There are both internal and external reasons for the depreciation of the Indian rupee. On the internal side, the weakening of the Indian economy may prompt the RBI to cut interest rates at the beginning of next year. From the Balance of Payments dynamics, India's current account is expected to deteriorate. The IMF predicts that the current account deficit will increase from $44.6 billion in 2024 to $56 billion in 2025 (from 1.15% of GDP to 1.31%). On the external side, the "Trump Trade" may continue to push the dollar higher, at least in the short term.

Figure 4.1: USD/INR

Source: Refinitiv, Tradingkey.com

4.2 USD/ASEAN currencies

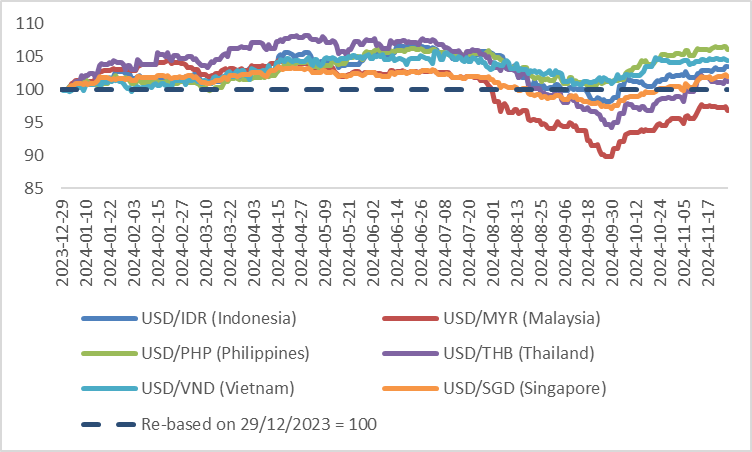

Since October, the USD/ASEAN currencies have increased sharply. When calculating the currency performance from the beginning of this year, only the Malaysian ringgit has appreciated and the Thai baht has depreciated slightly (Figure 4.2). The appreciation of the Malaysian ringgit is mainly due to the BNM's increased intervention in the foreign exchange market. Thailand is an important gold exporter in the ASEAN region. The rise in gold prices this year has supported the currency. Looking forward, in the short term, due to the continued appreciation of the USD index (For details, please read our report on Exchange rate outlook: Bullish on USD and bearish on EUR), we expect all ASEAN currencies to continue to decline. Among them, the currencies of export-oriented countries (such as the Singapore dollar and the Thai baht, assuming that the gold price will not rise sharply in 2025 to support the Thai baht) are under more downward pressure than the currencies of domestic-driven countries (such as the Indonesian rupiah and the Philippine peso). In the medium term, as the USD index is expected to turn in a downward trend, the currencies of ASEAN countries may stabilize.

Figure 4.2: USD/ASEAN currencies

Source: Refinitiv, Tradingkey.com