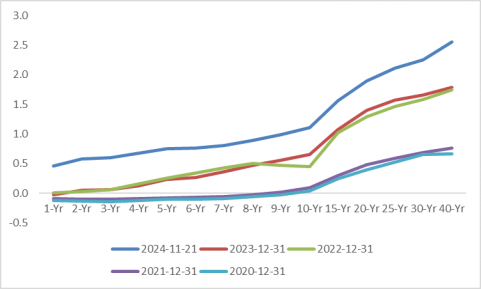

Asset Allocation in Developed Markets: Continue to be Bullish on US Stocks

Executive summary

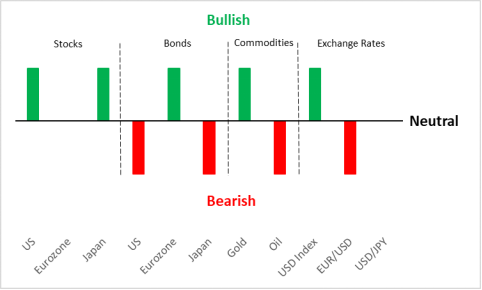

Short-term (<3 months) view

Source: Tradingkey.com

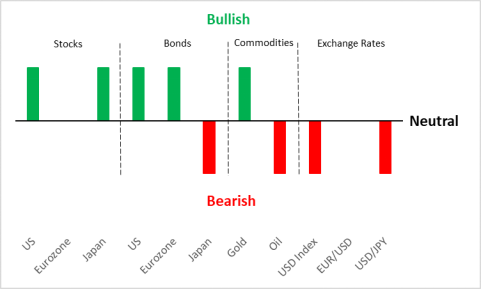

Medium-term (3-12 months) view

Source: Tradingkey.com

1. Macroeconomics

1.1 US

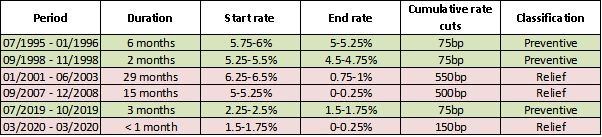

In terms of GDP growth, fixed investment growth may decrease and then rise in the remaining 2024 and 2025. The cooling of the labour market may de-escalate and consumption is expected to remain resilient. In addition, following his victory in the General Election, Trump’s tax cuts and other related policies may boost growth. Therefore, the US economy is expected to reach a "soft landing" or even "no landing". We expect US real GDP growth to be 2.7% in 2025, higher than the IMF's October forecast of 2.2%. In terms of inflation, US rent prices may remain elevated. Trump's policy of deporting illegal immigrants may push up wages, and the increase in tariffs is expected to cause the risk of re-inflation. In terms of fiscal policy, due to Trump’s tax cut policy, the US fiscal deficit is expected to increase significantly. This may drive up government net borrowing to 8% or above in 2025. In terms of monetary policy, driven by the "soft or no landing" and re-inflation, this cycle of rate cuts is expected to be preventive. From historical dynamics, the Fed had six rate cut cycles since 1995. The preventive interest rate cuts had slower paces, smaller reductions, and shorter durations (Figure 1.1). We expect the Fed policy rate to be cut by 25bps in December, and other 50bp reductions will be in next year. The final rate may terminate at 3.75%-4%, whose level is about 150 basis points higher than the neutral interest rate before the pandemic, and also higher than the consensus. In short, we forecast that the Fed's interest rate will remain high for longer.

Figure 1.1: Historical Fed interest rate cut cycles

Source: Fed, Tradingkey.com

1.2 Eurozone

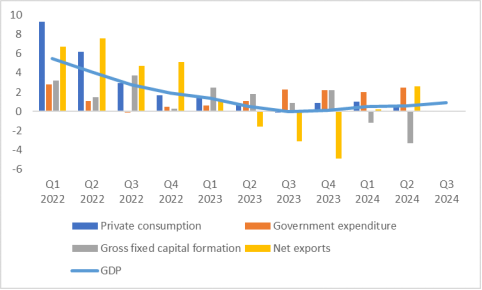

The eurozone economy has been recovering modestly in 2024. From the expenditure side, GDP growth was mainly contributed by external demand, and domestic investment was a drag (Figure 1.2.1). The main reason for weak domestic demand was that the uncertainty caused by Europe's structural challenges constrained the recovery of consumption and investment. Looking forward, due to the positive and negative factors offsetting each other, we expect the eurozone to continue recovering slowly in the coming quarters. On the positive side, despite negotiated wages rising 5.4% y-o-y in Q3 2024, the largest increase since 1993, high inflation in the eurozone may be a thing of the past. The CPI is expected to remain at around 2% in 2025. This, together with current weak growth, will lead to the ECB continuing to cut interest rates. We forecast that the central bank will cut its rates by 25bps in December and 100bps cuts in 2025. Continued rate cuts will have a stimulating effect on both investment and consumption. When the rate cut cycle is gradually taking effect, credit growth in the eurozone may continue to increase. Mortgages, which are most sensitive to interest rates, may show a stronger recovery. An increase in fixed asset investment driven by lower interest rates may also drive up corporate credit demand. These all are likely to boost domestic demand. On the negative side, the resurgence of protectionism may be a headwind for global trade. More specifically, the Trump administration's tariff policy may have a significant impact on the eurozone. In short, the "domestic demand < external demand" in 2024 will turn into "domestic > external" in 2025.

Figure 1.2: Eurozone GDP growth by expenditure (% y-o-y)

Source: Eurostat, Tradingkey.com

1.3 Japan

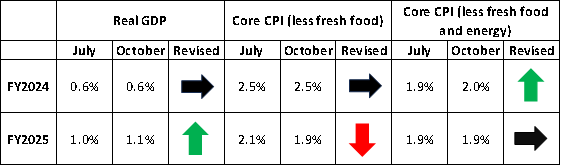

Exports are the main driver of Japanese economic growth from H2 2023 to Q1 2024. Since Q2 2024, Japan has begun to show signs of a rebound in domestic demand. We expect the Japanese economy to continue to recover in 2025. Three reasons are as follows. The first is consumption. Positive growth of real income is expected to drive the recovery of Japan's domestic demand. From April 2022 to May 2024, real wage growth was negative due to higher inflation, which dragged down consumption. Since June 2024, the growth rate of real wages has turned positive. In addition, in October, the Japanese Trade Union set the 2025 Shuntō wage increase target at more than 5%, which is the same as in 2024. Looking forward, given the backdrop of nominal wage growth continuing to exceed inflation, positive real wage growth is expected to support Japanese domestic demand. The second is investment. Investment may continue to increase driven by insufficient labour force, green and digital transformation as well as the continued expansion of corporate revenues. The third is exports. The global rate cut cycle, the US "soft landing" and China's stimulus plan have been stabilizing global manufacturing PMI. Country-wise, the Japanese manufacturing industry has a large overlap with China. This means Japan may benefit from the US-China trade war, as the US may switch its import place from China to Japan. For these reasons, at the Monetary Policy Meeting in October, the Bank of Japan (BoJ) raised the GDP forecast by 0.1 percentage point to 1.1% in FY2025, higher than 0.6% in FY2024 (Figure 1.3). In terms of inflation, due to the victory of the Shuntō in 2024 and the possible continued wage increase in the 2025 Shuntō, a "wage-inflation" spiral is expected to continue. The BoJ expects the core CPI to stabilize at 1.9% in 2025 (Figure 1.3). Due to higher growth and inflation, we expect the central bank to raise interest rates once in December this year and twice in 2025.

Figure 1.3: Bank of Japan forecasts (July vs. October 2024)

Source: Bank of Japan, Tradingkey.com

2. Stocks

2.1 US

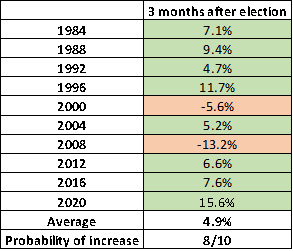

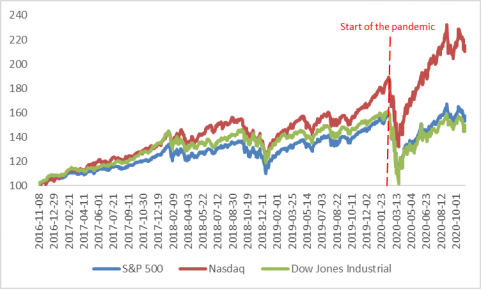

In the short and medium term, US stocks are mainly driven by two factors: Trump's election and the Fed’s rate cut cycle. The two factors both point that US stocks may go up. First, from historical dynamics, there were ten elections over the past 40 years. Three months after the elections, stock prices increased eight times out of ten, with an average rise of 4.9%. Two reasons for the increases are: 1) The promised growth-supportive policies started to be launched; 2) The election-related uncertainties faded. In addition, Trump's tax cut policy benefits US stocks. In his first term in office, stock prices went up by 7.6% three months after Trump obtained the presidency in 2016 (Figure 2.1.1). We extend the time horizon from three months to four years – 8 November 2016 to 3 November 2020, when he lost the election. While most of the period was in the Fed's rate hike cycle and affected by the pandemic, the S&P 500, Nasdaq and Dow Jones Industrial Average rose by 57.5%, 114.9% and 49.9% respectively, which were higher than the historical average (Figure 2.1.2). Looking forward, compared with his first term, Trump is expected to continue to promote more radical corporate tax cuts. Meanwhile, the Republican Party is expected to pay more attention to market efficiency than the Democratic Party, supporting digital currency and abolishing AI restrictive laws. These all are likely to benefit US stocks.

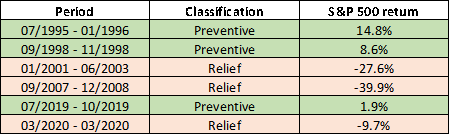

Second, in terms of the relationship between rate cut cycles and US stock performance, the impact on stocks depends on what drives the rate cuts. According to the dividend discount model (DDM), stock price = corporate earnings/market interest rate. The numerator, corporate earnings, are mainly affected by economic growth and corporate fundamentals. The denominator is partly affected by monetary policy. The performance of the stock market depends on the interaction between growth and interest rate cuts. Over the historical six cycles of rate cuts, in the three relief rate cut cycles, the economy experienced substantial recessions. The negative effect of recessions was larger than the positive effect of rate cuts, driving down stock prices. In the three preventive rate cut cycles, growth slowed down but was still positive. The effect of rate cuts was greater than the growth effect, raising the stocks (Figure 2.1.3). As discussed in the macroeconomics section, we expect this cycle of rate cuts to be preventive, so US stocks are more likely to increase.

Figure 2.1.1: S&P 500 performance three months after elections

Source: Fed, Tradingkey.com

Figure 2.1.2: US stock performance during Trump’s first term

Source: Fed, Tradingkey.com

Note: Re-based 8 November 2016 = 100

Figure 2.1.3: S&P 500 return during rate cut cycles

Source: Fed, Tradingkey.com

2.2 Eurozone

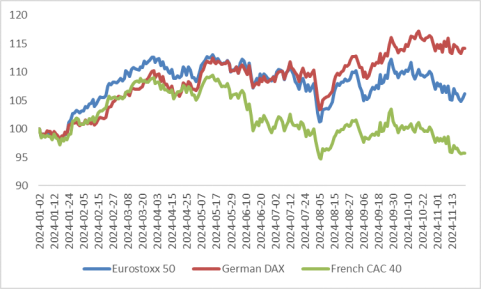

Eurozone stocks face both external negative and internal positive factors. In terms of external factors, the Trump administration is likely to increase tariffs on EU goods. This may further slow down the eurozone's growth, reducing European companies' revenues and profits. Among all the sectors, autos, industrials, and sporting goods are likely to be hit the hardest. In addition, if the US imposes a 60% tariff on Chinese goods, China may shift its export destination to the EU. This may cause European companies to face greater competitive pressure from Chinese companies. What is more, if the Trump administration relaxes corporate regulations, this may promote mergers, acquisitions and consolidations of US companies. European companies may then face greater threats from US competitors. In terms of internal factors, the ECB's substantial interest rate cuts will reduce the financing costs of European companies and raise the valuations of European stocks. Due to the offsetting of internal and external factors, we expect eurozone stocks to enter a period of choppy trading (Figure 2.2).

Figure 2.2: Major stock indices in the eurozone

Source: ECB, Tradingkey.com

Note: Re-based 2/1/2024 = 100

2.3 Japan

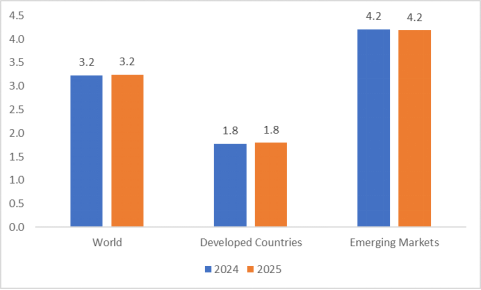

Japanese stocks have been volatile over the past four months due to the political chaos. However, the stocks benefited from corporate earnings data, and the prices showed resilience during the period of volatility. Looking forward, due to the financial restructuring of Japanese companies, the amount of the share repurchase in 2024 is expected to exceed the previous years, benefitting Japanese stocks. In addition, most of the revenue and profits of Japanese-listed companies come from overseas rather than domestic. This means the overseas economy is the key to determining the profitability of these companies. The IMF forecasts that real GDP growth of the world, developed countries, and developing markets will be 3.2%, 1.8% and 4.2% respectively in 2025, the same as in 2024 (Figure 2.3). This means that the EPS growth of Japanese companies in 2025 is likely to remain as high as that in 2024. What’s more, Japanese stocks are likely to provide superior risk-adjusted returns as their valuations are still lower than those of US stocks. Therefore, we are bullish on Japanese stocks.

Figure 2.3: IMF real GDP growth forecasts (%)

Source: IMF, Tradingkey.com

3. Bonds

3.1 US

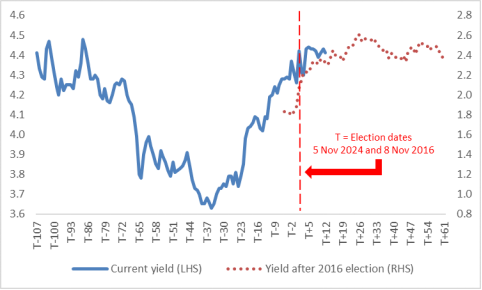

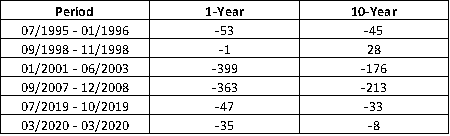

On 8 November 2016, Trump was elected as the US President. Due to his political propositions, US Treasury yields rose in the early period of the Trump 1.0 era. Looking forward, in the short term, due to Trump’s policy, elevated fiscal deficit, potential higher tariffs and re-inflation may cause the yields to continue to rise (Figure 3.1.1). US Treasury yields and the Fed's policy rate are highly correlated. From historical dynamics, the 1-year yield fell in all the past six rate cut cycles. The 10-year yield declined in five cycles, except for the 1998 cycle when the yield rose slightly by 28bp (Figure 3.1.2). Among all types of US bonds, shorter-duration and higher-grade bonds are more affected by the Fed’s rate cuts. Therefore, in the medium term, when the impact of the "Trump Trade" fades and the rate cut effect continues, US Treasury yields are likely to fall.

Figure 3.1.1: US 10-year government bond yield (current vs. after 2016 election, %)

Source: Fed, Tradingkey.com

Figure 3.1.2: US government bond yields during rate cut cycles

Source: Fed, Tradingkey.com

3.2 Eurozone

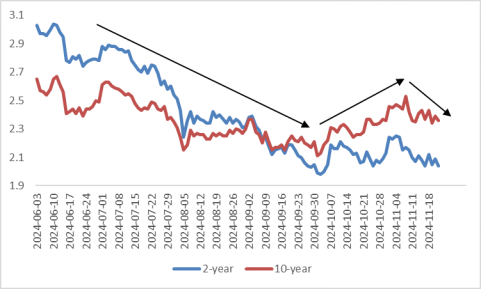

German 10-year government bond yield increased in October, mainly driven by political uncertainty after the collapse of the coalition in the country (Figure 3.2). However, we believe that most of the negative factors have been priced in, and the yield has started to fall since early November. Looking forward, German yields are expected to continue to fall. Due to the internal structural challenges in the region, the eurozone economy may experience a weak recovery. Trump's potential tariff increase is likely to pose a large threat to the already weak economy. Both may result in the ECB easing its monetary policy. We expect the central bank to cut interest rates by 125bp by the end of 2025, decreasing the bond yields. For the same reasons, we also expect the government bond yields of France and Spain to fall. However, compared with Germany and Spain, French yields may fall less (and the bond prices may increase less) due to its political tail risk.

Figure 3.2: German 2-year and 10-year government bond yields (%)

Source: ECB, Tradingkey.com

3.3 Japan

Due to the tightening of monetary policy, the Japanese bond yield curve has continued to move upward in the past few years (Figure 3.3). Looking forward, the move of Japanese bond yields depends on both internal and external factors. In terms of internal factors, growth recovery, higher inflation and the normalization of the BoJ's monetary policy may continue to push up the yields. External factors mainly contribute to the overspread of the "Trump Trade" and rising US Treasury yields. Trump's election in 2016 caused a significant increase in US Treasury yields, which also promoted Japanese bond yields to go up. In that year, the 10-year yield hit the 0.1% interest rate cap set by the BoJ under its YCC policy. In the current Trump 2.0 era, re-inflation has reduced expectations for the scale of the Fed’s rate cut cycle. This may support the BoJ to normalize its monetary policy more quickly and further, pushing up Japanese bond yields. In addition, the impact of the "Trump Trade" on US bond yields is mainly reflected in the increase in long-term rates. Due to the strong correlation between sovereign bonds in developed countries, Japan's long-term bond yields may rise more than the short-term ones, making the Japanese bond yield curve steeper.

Figure 3.3: Japanese government bond yield curves (%)

Source: BoJ, Tradingkey.com

4. Commodities

4.1 Gold

In October, as the market expectations of the Trump victory and the Republican sweep heated up, investors flocked to precious metals to hedge against the US fiscal deficit, inflation concerns, and geopolitical tensions. After the market correction in the first half of November, we expect gold prices to increase. The reasons are as follows. First, the prices of safe-haven assets may increase due to the escalation of the Russia-Ukraine conflict. Second, Trump's massive spending plan may further exacerbate the pressure on US public finances as well as higher tariff rates and tightening immigration policies may cause re-inflation. Third, due to the accelerating of the US debt expansion, central banks in the major economies are likely to re-start to purchase the precious metal.

4.2 Crude oil

Crude oil prices are expected to have more downside risk than upside potential. On the downside, electric vehicle sales in China have increased significantly over the past few years, accounting for nearly 50% of total car sales in October. This, together with an increase in LNG truck registrations, is likely to continue to reduce diesel consumption, which in turn may decrease the demand for crude oil. On the upside, the Biden administration lifted the restriction on Ukraine using US-provided weapons to strike deep into Russia, worsening the Russia-Ukraine conflict. In our baseline forecast, as the downside and upside factors partly offset each other, oil prices are unlikely to decrease sharply in the short and medium term. However, investors should pay attention to the OPEC+ meeting in December. The oil producers are expected to further delay their production increases. However, if they decide to increase their production to increase revenues, oil prices will drop significantly.

5. Exchange rates

Given the scenario of resilient growth, re-inflation and the hawkish Fed, we expect the USD index to appreciate, driving down the EUR/USD in the short term. Due to the positive and negative factors offsetting each other, the USD/JPY is likely to enter a short period of choppy market. In the medium term, the effect of “Trump Trade” will fade. With the backdrop of the Fed’s rate cut cycle, the trend of the dollar's volatility and weakening may not revert. For details, please read our report on Exchange rate outlook: Bullish on USD and bearish on EUR.

.jpg)