[IN-DEPTH ANALYSIS] Switzerland: "Crazy" Trump Has Driven USD/CHF to Its Lowest Point; What Lies Ahead for CHF?

Executive Summary

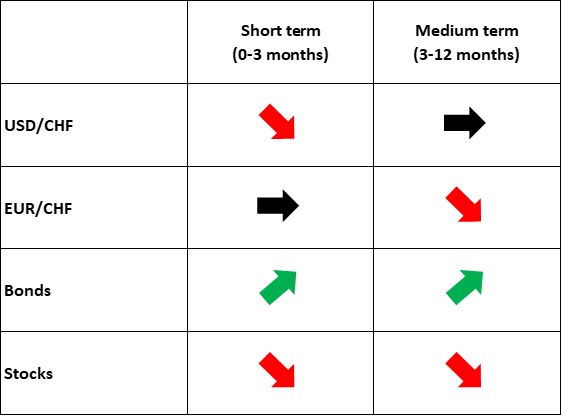

Swiss Franc vs. USD: The Swiss Franc (CHF) will be shaped by three key drivers: risk appetite, interest rate dynamics, and Swiss National Bank (SNB) interventions. The Trump administration’s high-tariff policies will reinforce the CHF’s safe-haven status. Limited room for further SNB rate cuts will constrain downward pressure on the CHF from monetary policy. However, increased SNB intervention in the foreign exchange market is likely to curb excessive CHF appreciation and alleviate pressure on Swiss exports. Consequently, we expect the CHF to appreciate modestly against the USD in the short term (0-3 months).

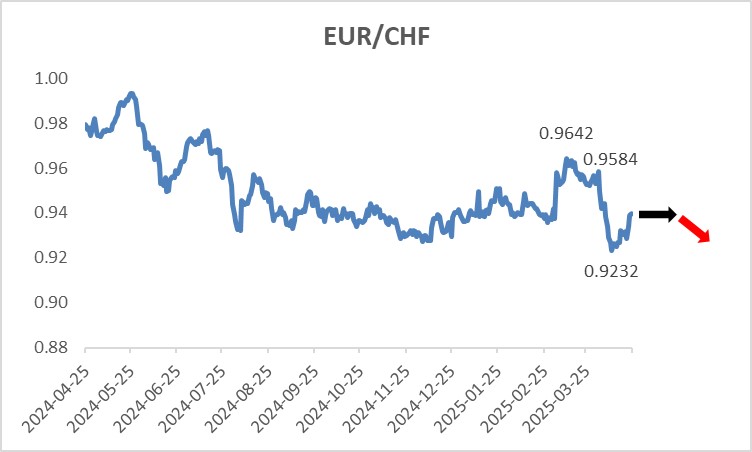

Swiss Franc vs. EUR: Influenced by Europe’s defence-oriented policies and Germany’s fiscal spending, we anticipate the EUR to strengthen against the USD in the short term. Given the expected CHF appreciation against the USD, we project the EUR/CHF pair to trade within a range.

Source: Refinitiv, Tradingkey.com

Source: Refinitiv, Tradingkey.com

Source: Refinitiv, Tradingkey.com

* Investors can directly or indirectly invest in the foreign exchange market, bond market and stock market through passive funds (such as ETFs), active funds, financial derivatives (like futures, options and swaps), CFDs and spread betting.

1. Exchange Rate

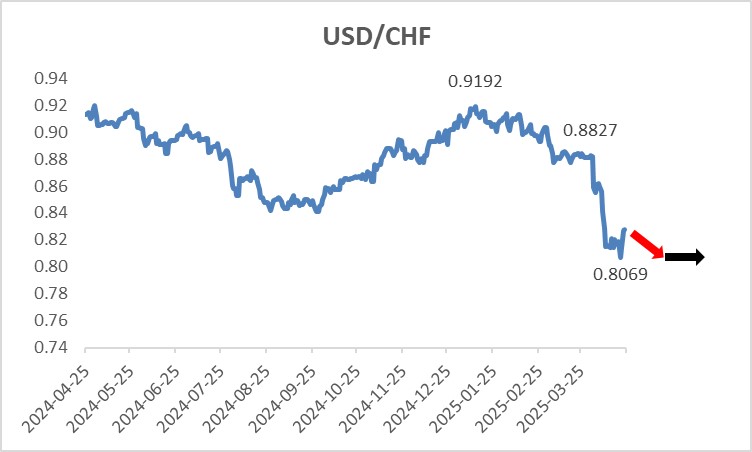

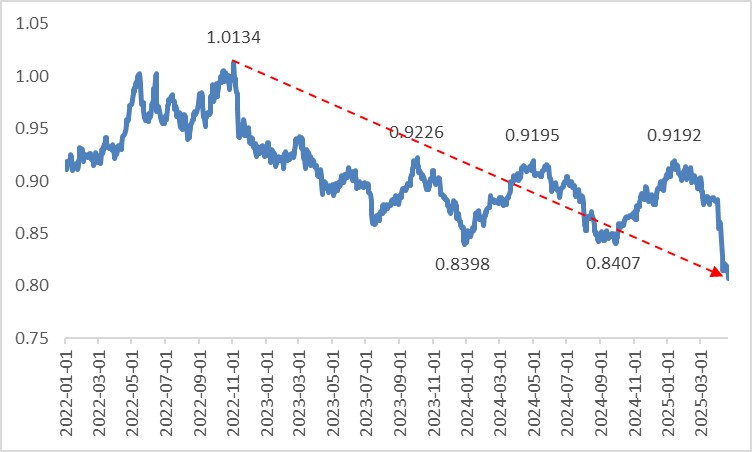

TradingKey - Switzerland’s neutral status, political and economic stability, financial confidentiality traditions, and SNB’s intervention capacity underpin the Swiss Franc’s (CHF) safe-haven appeal. Amid ongoing Russia-Ukraine tensions, Middle East instability, and U.S. policy uncertainty, the CHF has appreciated steadily since late 2022, with USD/CHF hitting a 10-year low (Figure 1). Trump’s 2 April 2025 “Liberation Day” announcement of “reciprocal tariffs”, followed by erratic policy shifts, triggered market volatility and fuelled the CHF’s latest rally.

Looking forward, the CHF will be driven by three factors: risk appetite, interest rates, and Swiss National Bank (SNB) interventions. On risk appetite, Trump’s tariff policies introduce both uncertainty (from frequent U.S. policy changes) and certainty (persistent high tariffs’ negative impact). This dual dynamic will sustain the CHF’s safe-haven demand, supporting its value. On interest rates, while the SNB could cut rates to 0% or negative territory, its limited policy space will restrict downward pressure on the CHF. Consequently, SNB intervention in the FX market is likely to intensify to temper sharp CHF appreciation and support exporters. Synthesizing these factors, we expect modest CHF appreciation against the USD in the short term (0-3 months).

For the USD side of the USD/CHF pair, while the USD retains some safe-haven appeal amid global uncertainty, a slowing U.S. economy and the Federal Reserve’s renewed rate cuts are likely to weaken the USD Index in the short term, further supporting CHF strength. However, in the medium term (3-12 months), we anticipate a USD Index rebound (see “[In-Depth Analysis] Trump Policies: Market Overreacted, Remain Bullish on Stocks”, published 17 March 2025), potentially stabilizing USD/CHF.

Against the EUR, driven by Europe’s defence spending and Germany’s fiscal stimulus, the EUR is expected to strengthen versus the USD in the short term. With CHF also appreciating against the USD, we foresee EUR/CHF trading in a range.

Figure 1: USD/CHF since 2022

Source: Refinitiv, Tradingkey.com

* To learn more about the current economic situation and outlook, refer to the final section, "Macroeconomics", in this article.

2. Bonds

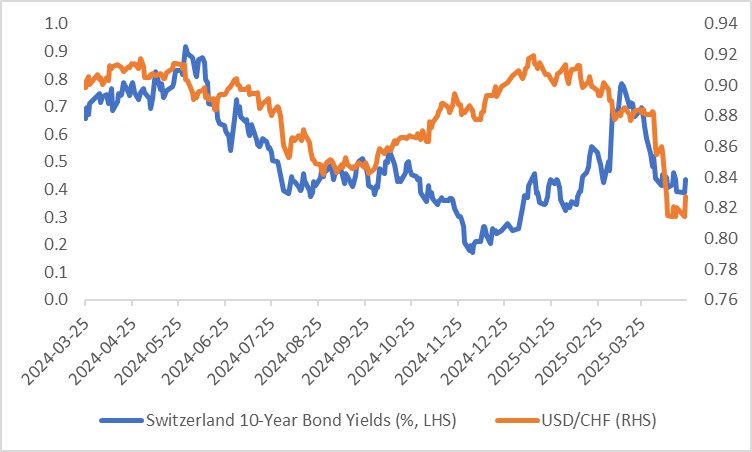

Unlike most countries where bond yields and currency strength are positively correlated, Switzerland’s safe-haven assets exhibit a significant inverse relationship between CHF and bond yields (Figure 2.1). We expect Swiss government bond yields to continue declining for three reasons:

- Anticipated CHF appreciation against the USD will exert downward pressure on yields.

- The SNB’s expected June 2025 rate cut will further depress yields.

- Escalating U.S. tariff policies will drive safe-haven capital flows into Swiss bonds, boosting bond prices and compressing yields.

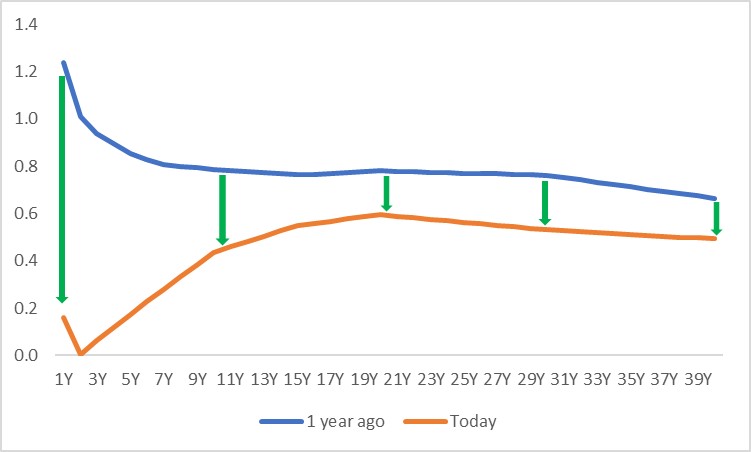

Regarding duration, the SNB’s rate cuts over the past year have primarily driven down short-end yields, steepening the yield curve (Figure 2.2). Moving forward, as the policy rate nears 0% with limited further easing potential, global economic uncertainty will become the primary driver of yield declines, flattening the yield curve.

Figure 2.1: Switzerland 10-Year Bond Yields and USD/CHF

Source: Refinitiv, Tradingkey.com

Figure 2.2: Switzerland Bond Yield Curve (%)

Source: Refinitiv, Tradingkey.com

* The Yield Curve is a curve that illustrates the relationship between bond yields and their maturities, commonly used to analyse interest rate levels across different bond terms. The horizontal axis represents the remaining maturity of bonds (e.g., 1 year, 10 years, 30 years), while the vertical axis shows the bond yields. Generally, if the curve's movement is driven by central bank policy rates, short-term (front-end) yields exhibit larger changes. Conversely, if driven by economic fundamentals, long-term (back-end) yields experience greater fluctuations.

3. Stocks

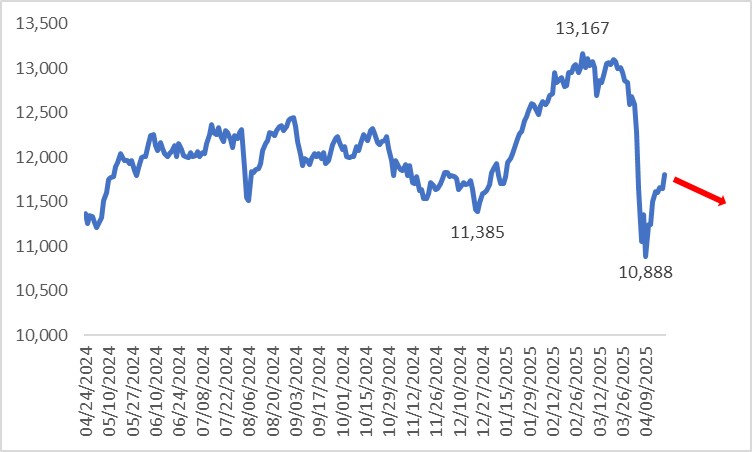

Influenced by global equity markets (particularly U.S. stocks), the Swiss Market Index (SMI) has fallen sharply from its 3 March 2025, peak of 13,167 (Figure 3). Domestic and external headwinds are likely to persist. Particularly, slowing economic growth and limited SNB rate-cut flexibility will weaken corporate earnings. However, Switzerland’s safe-haven status lends its equity market defensive qualities. Additionally, potential SNB FX interventions to prevent excessive CHF appreciation could mitigate export sector pressures. Therefore, we expect the Swiss stock market to decline modestly in 2025.

Figure 3: Swiss Market Index

Source: Refinitiv, Tradingkey.com

4. Macroeconomics

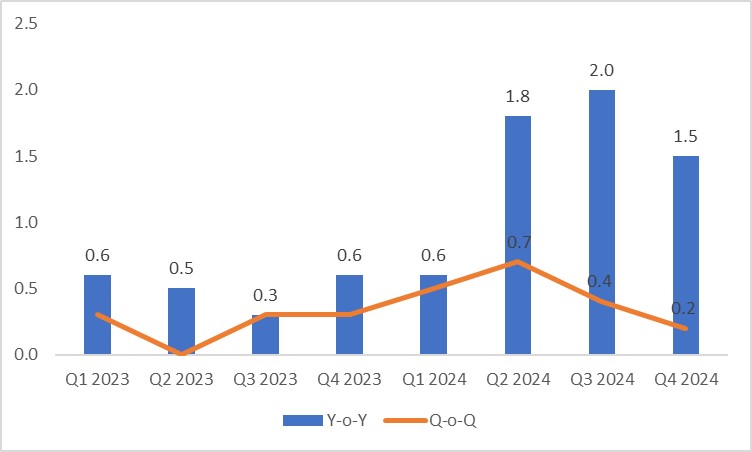

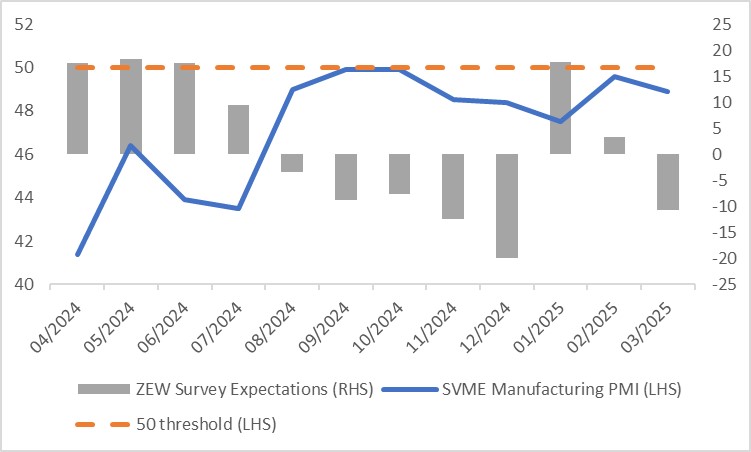

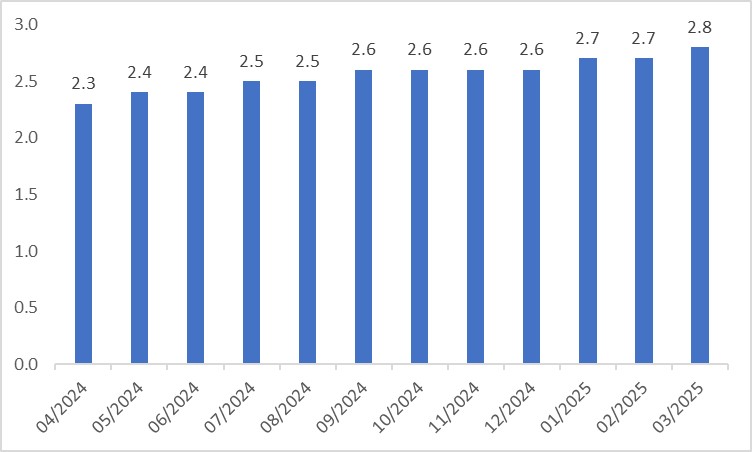

In Q4 2024, Switzerland’s real GDP growth slowed to 1.5% year-on-year, down 0.5 percentage points from Q3 (Figure 4.1), driven by global (especially EU) economic slowdown, weak domestic consumption, and subdued investment. High-frequency data in early 2025 indicate persistent economic softness. On the consumption side, February’s Real Retail Sales growth improved slightly from January but remained well below December 2024 levels (Figure 4.2). This weakness has spilt over to production, with the SVME Manufacturing PMI consistently below the 50 threshold and March’s ZEW Survey Expectations recording double-digit negative values (Figure 4.3). The labour market also shows signs of strain, with the unemployment rate rising from 2.3% a year ago to 2.8% (Figure 4.4).

Figure 4.1: Real GDP (%)

Source: Refinitiv, Tradingkey.com

Figure 4.2: Real Retail Sales (y-o-y, %)

Source: Refinitiv, Tradingkey.com

Figure 4.3: Manufacturing PMI and ZEW Survey Expectations

Source: Refinitiv, Tradingkey.com

Figure 4.4: Unemployment Rate (%)

Source: Refinitiv, Tradingkey.com

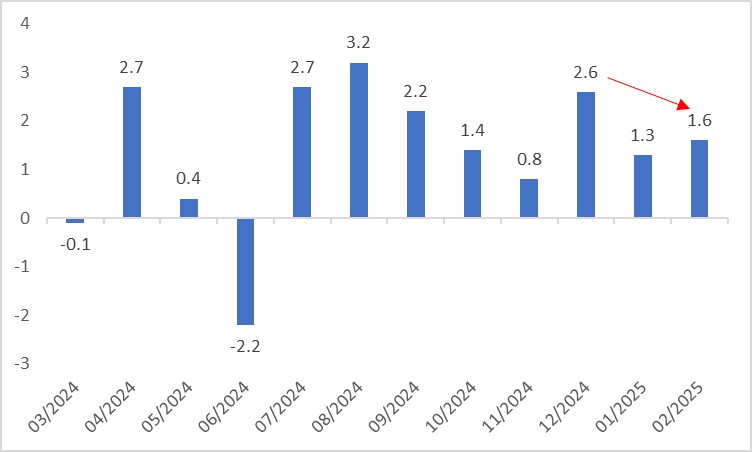

As a small, open economy, Switzerland is highly sensitive to global economic and policy developments, particularly from the U.S. Ahead of Trump’s “reciprocal tariffs”, March 2025 exports surged 22.2% month-on-month (Figure 4.5), driven primarily by chemicals and pharmaceuticals, likely reflecting pre-emptive shipments amid tariff uncertainty. Looking ahead, Trump’s tariffs will impact Swiss exports in two ways: directly, through potential tariffs on Swiss goods (e.g., pharmaceuticals, machinery, watches); and indirectly, by slowing global (especially EU) growth, dampening external demand. Together, these factors are expected to weaken Swiss exports, further dimming economic prospects.

Figure 4.5: Exports (m-o-m, %)

Source: Refinitiv, Tradingkey.com

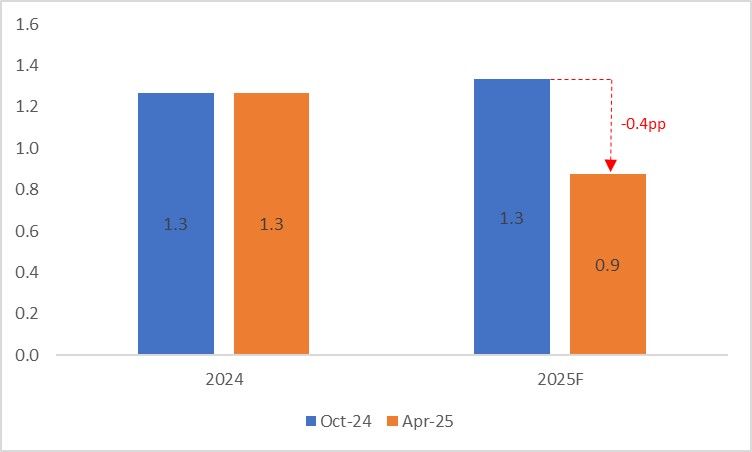

Although global economic uncertainty is expected to drive capital inflows into the safe-haven Swiss banking sector, these positive effects are unlikely to offset the aforementioned negative factors. As a result, a slowdown in the Swiss economy over the next few quarters is highly probable. The IMF’s April 2025 forecast lowered Switzerland’s 2025 GDP growth by 0.4 percentage points to 0.9% compared to October 2024 (Figure 4.6).

Figure 4.6: IMF GDP Forecasts (%)

Source: Refinitiv, Tradingkey.com

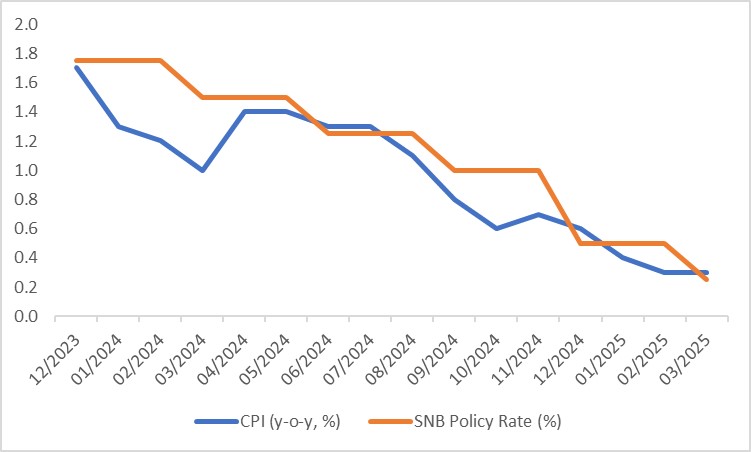

On inflation, weak domestic demand has driven CPI growth down to 0.3% in March 2025, raising deflation risks. Against this backdrop, the SNB cut its policy rate by 25 basis points to 0.25% on 20 March 2025 (Figure 4.7). We expect the SNB to lower rates to 0% at its June 2025 meeting.

Figure 4.7: CPI and SNB Policy Rate

Source: Refinitiv, Tradingkey.com