Thailand: No Opportunity in the Stock Market, What About the Bond Market?

Executive Summary

1. Background

1.1 1945-1960s: Post-War Reconstruction and Import-Substituting Industrialization

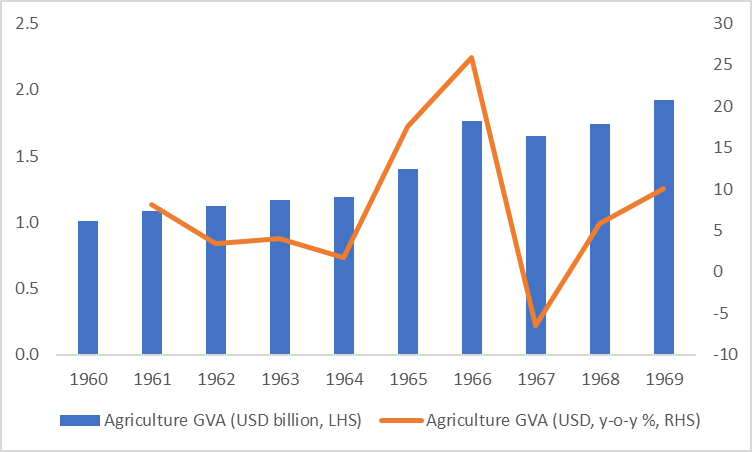

After the end of World War II, Thailand's economy was severely damaged with significant impacts on infrastructure and agricultural production. The government initiated efforts to revive the economy, focusing particularly on restoring agricultural output and rebuilding infrastructure (Figure 1.1). In the 1950s, Thailand adopted policies of Import-Substituting Industrialization (ISI) to reduce reliance on imported goods by developing domestic industries. These policies included tariff protections, subsidies and support for state-owned enterprises to spur industrial growth.

Figure 1.1: Thailand Agriculture GVA

Source: Refinitiv, World Bank, Tradingkey.com

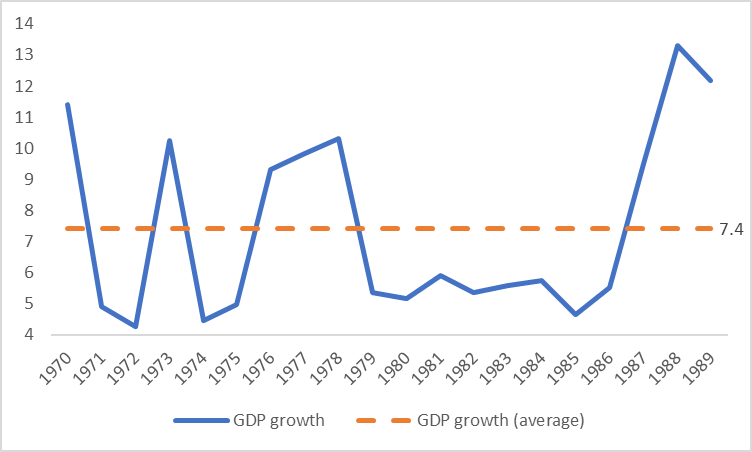

1.2 1970-1980s: Export-Oriented Economic Growth

In the 1970s, the Thai government shifted its economic policy towards an export-oriented growth model, promoting economic transformation by encouraging foreign investment and developing labour-intensive industries such as textiles, electronics and food processing. Entering the 1980s, Thailand's economy experienced a period of rapid growth, with an average annual GDP growth rate of 7.4% (Figure 1.2). Tourism and manufacturing became the main drivers of this economic expansion.

Figure 1.2: Thailand GDP growth, 1970-1989 (%)

Source: World Bank, Tradingkey.com

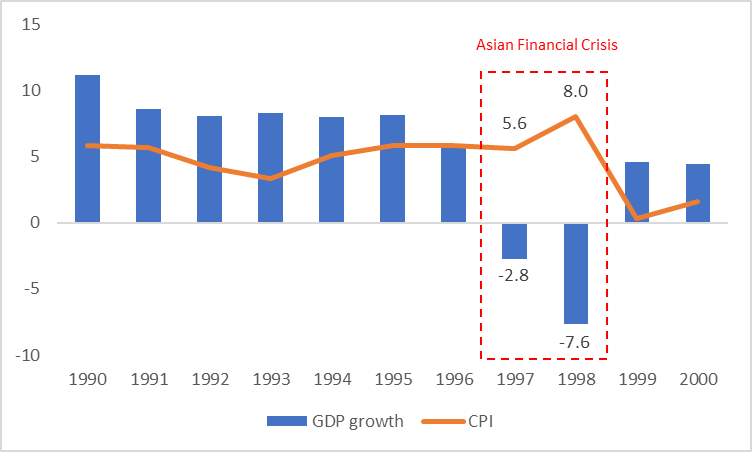

1.3 1990s: Economic Crisis and Recovery

In the early 1990s, Thailand's economy continued to grow rapidly, but asset bubbles and financial risks were accumulating. This culminated in the 1997 Asian Financial Crisis, where Thailand was hit hard; the Thai baht plummeted and both the stock and real estate markets collapsed (Figure 1.3). Post-crisis, with assistance from the International Monetary Fund (IMF), the Thai government implemented a series of economic reforms. These included financial system restructuring, corporate debt restructuring and fiscal austerity measures. In 1999, Thailand's economy began to recover.

Figure 1.3: GDP growth and CPI, 1990-2000 (%)

Source: World Bank, Tradingkey.com

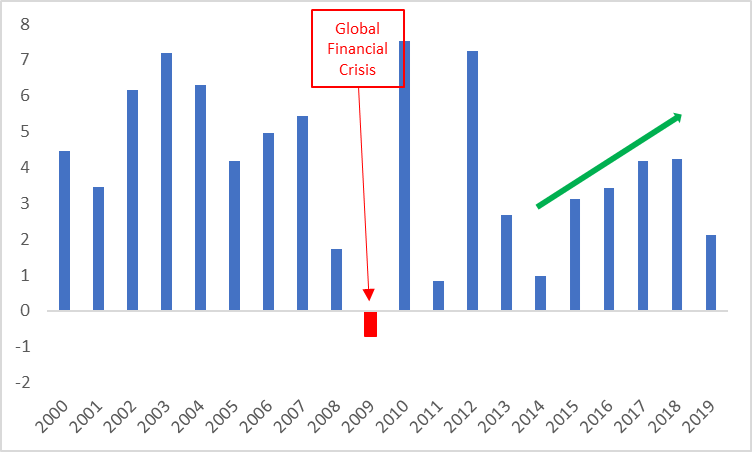

1.4 2000-2019: Globalization and Diversified Development

In the 2000s, Thailand actively engaged in globalization by signing numerous Free Trade Agreements (FTAs), promoting exports and attracting foreign investment. This made the automotive industry, electronics and agricultural products key pillars of the economy. Since the 2010s, the Thai government has further pushed for economic diversification, focusing on high-tech industries, services and a green economy. Tourism, medical tourism and creative industries have emerged as new drivers of economic growth. However, despite these advancements, Thailand faced challenges such as political instability, income inequality and external economic shocks. Following the 2014 military coup, the political situation stabilized, supporting the economic development (Figure 1.4).

Figure 1.4: GDP growth, 2000-2019 (%)

Source: World Bank, Tradingkey.com

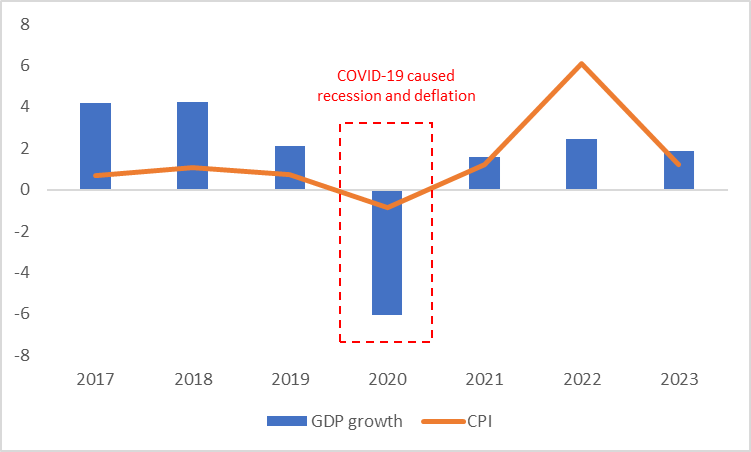

1.5 Post-2019: The COVID-19 Pandemic and Future Outlook

The COVID-19 pandemic had a significant impact on Thailand's economy, particularly affecting tourism and exports (Figure 1.5). In response, the government implemented various measures, including fiscal stimulus, monetary easing and enhanced public health protocols. Looking ahead, the Thai government is actively promoting the "Thailand 4.0" strategy, which aims to drive economic transformation through innovation and technology. Key areas of focus include the digital economy, smart manufacturing, biotechnology and green economics, all aimed at fostering long-term and sustainable economic development.

Figure 1.5: GDP growth and CPI, 2017-2023 (%)

Source: World Bank, Tradingkey.com

2. Recent Macroeconomics

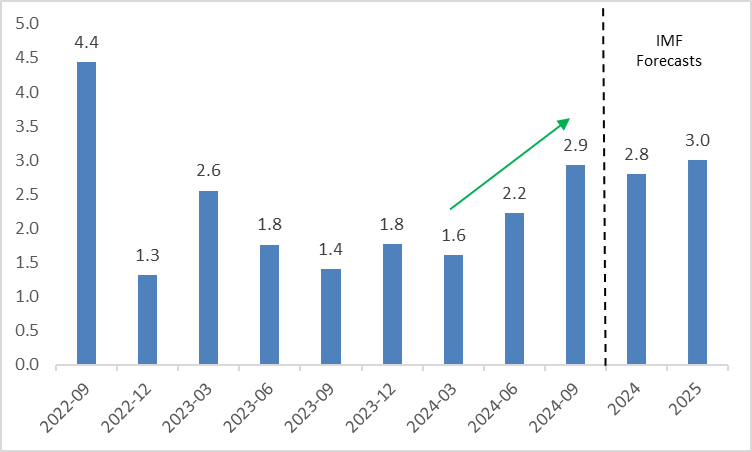

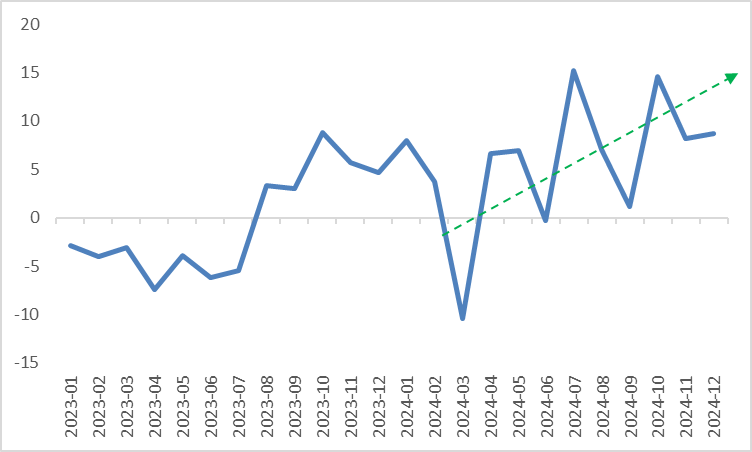

After experiencing economic weakness from the second half of 2023 to the first half of 2024, Thailand's economic growth gradually recovered, with GDP growth in the third quarter of 2024 rebounding to 2.9% year-on-year (Figure 2.1). This recovery was primarily driven by three key factors. First, the gradual recovery of demand from China, coupled with global importers frontloading purchases to avoid potential US tariffs, led to a significant increase in Thailand's goods exports. Second, the rise in tourist arrivals boosted service exports (Figure 2.2). Third, fiscal stimulus measures, including the completion of the first phase of the Digital Wallet Scheme and cash handouts to low-income and disabled citizens, contributed to the economic recovery.

Looking ahead, although potential tariffs may introduce uncertainty to Thailand's foreign trade, fiscal spending is expected to continue supporting the economy. This includes the implementation of the second and third phases of the Digital Wallet Scheme as well as price caps on electricity and diesel. The IMF projects Thailand's GDP growth to reach 3% in 2025, higher than in 2024.

Given the support from fiscal policy and the steady economic recovery, we do not expect the Bank of Thailand (BoT) to cut interest rates in the short to medium term. This is because Thailand's household debt, at around 90% of GDP, is significantly higher than that of other ASEAN countries. Premature rate cuts could exacerbate the household debt issue.

Figure 2.1: Thailand GDP growth (y-o-y, %)

Source: Refinitiv, IMF, Tradingkey.com

Figure 2.2: Thailand exports (y-o-y, USD %)

Source: Refinitiv, Tradingkey.com

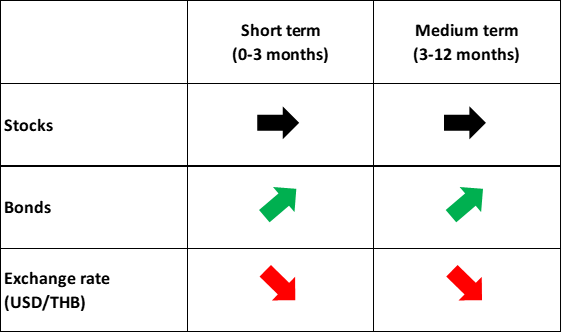

3. Stocks

Over the past three years, political turmoil has led to a risk-off sentiment among investors, resulting in poor performance in the Thai stock market (Figure 3.1). Looking ahead, the Thai stock market faces both positive and negative factors. On the positive side, with Paetongtarn Shinawatra becoming the new Prime Minister, political headwinds have eased. The Thai economy has passed its worst period since the second half of 2023 and GDP growth is gradually recovering. A more stable political environment coupled with economic recovery is expected to support corporate earnings growth, providing upward momentum for the stock market.

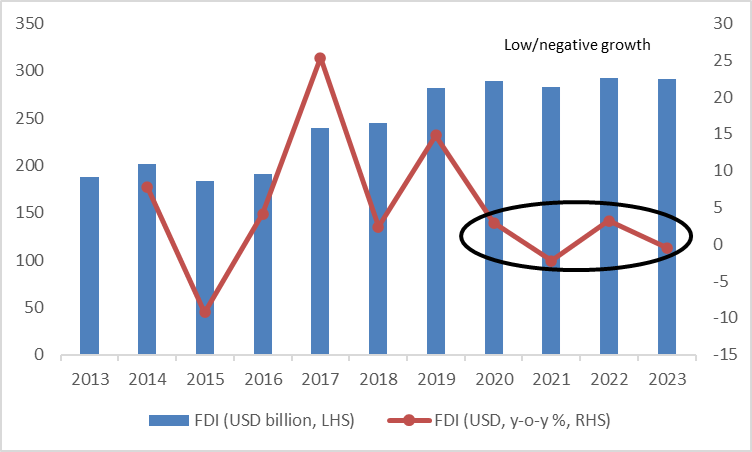

On the negative side, unlike most ASEAN central banks adopting accommodative monetary policies, the BoT has paused its rate-cutting cycle to curb further leverage buildup in the household sector. A relatively tighter monetary policy, combined with weakened foreign direct investment (FDI) attraction due to political instability (Figure 3.2), is exerting downward pressure on the stock market.

With upward and downward forces offsetting each other, we believe the Thai stock market may enter a choppy phase in the short to medium term.

Figure 3.1: SET Index

Source: Refinitiv, Tradingkey.com

Figure 3.2: Thailand's inward FDI stocks

Source: Refinitiv, Tradingkey.com

4. Bonds

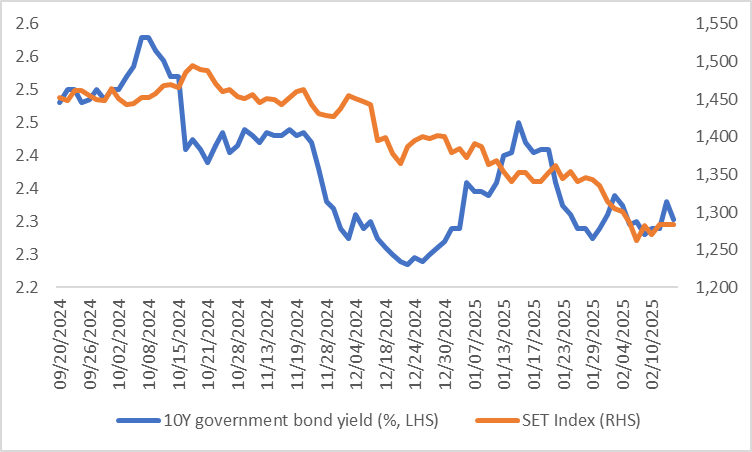

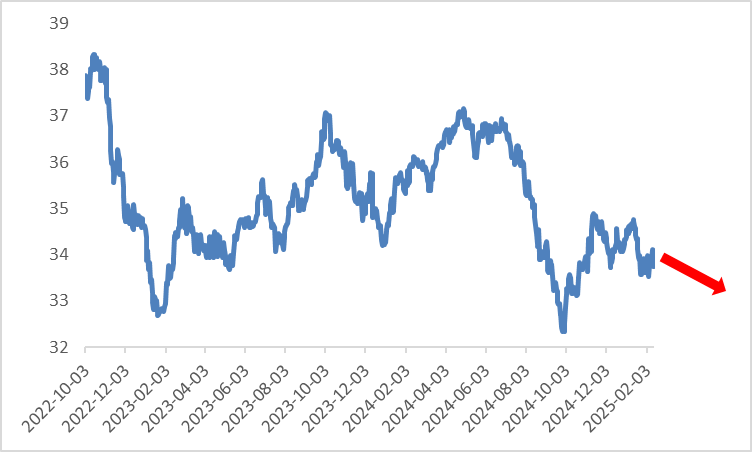

Since late September 2024, the yield on 10-year Thai government bonds and the Thai stock market have generally shown a downward trend, reflecting the equity-bond rotation effect in Thailand's financial markets (Figure 4.1).

Looking ahead, Thai bond yields will be primarily driven by three factors. First is the continuation of the rotation effect. As mentioned earlier, we expect the Thai stock market to enter a range-bound phase, so the flow of funds between equities and bonds is expected to have a limited impact on the bond market. Second is the influence of the BoT’s policy rate. The central bank is unlikely to cut rates further in the short to medium term and the pause in rate cuts has already been priced in by the market, so its impact will also be limited. Third, unlike the upward trend seen from FY2021 to FY2024, bond issuance in FY2025 (October 2024 to September 2025) has been relatively low so far, which is expected to push bond prices higher and yields lower.

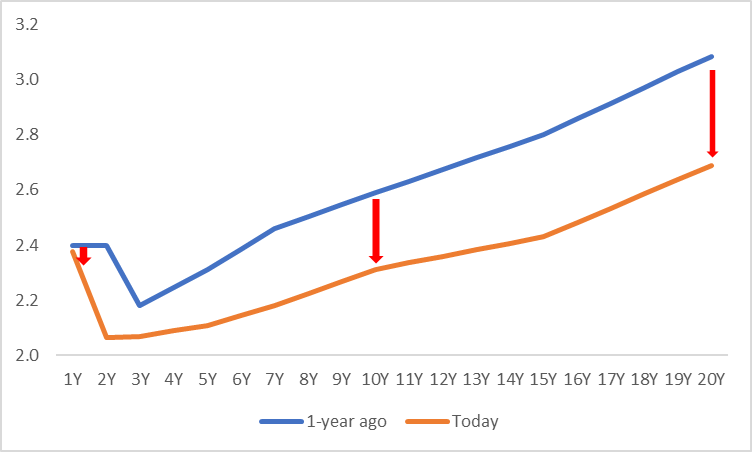

In terms of duration, the issuance of long-term bonds has been even lower. Therefore, we believe that the Thai government bond yield curve will shift downward while becoming flatter, making the purchase of long-term Thai government bonds a potentially rational investment decision (Figure 4.2).

Figure 4.1: Thailand 10Y government bond yield vs. stock market

Source: Refinitiv, Tradingkey.com

Figure 4.2: Thailand government bond yield curve (%)

Source: Refinitiv, Tradingkey.com

5. Exchange Rate

Similar to other currencies, the value of the Thai baht (THB) is influenced by factors such as macroeconomic conditions, the international environment as well as fiscal and monetary policies. Looking ahead, in the short term (0-3 months), gold prices are expected to be the primary driver of the baht's performance. We anticipate that gold prices will continue to rise. Given Thailand's role as a key gold trading hub in Southeast Asia, higher gold prices could boost gold export revenues, thereby supporting the baht. In the medium term (3-12 months), the gradual decline of the USD Index is expected to further strengthen the THB's exchange rate (Figure 5).

Figure 5: USD/THB

Source: Refinitiv, Tradingkey.com