Asset Allocation in Emerging Europe: Any Investment Opportunity in This Region?

Executive summary: Short- and medium-term view

| Short term (0-3 months) | Medium term (3-12 months) |

Stocks |

|

|

Czech Republic | Neutral | Neutral |

Hungary | Bullish | Bullish |

Poland | Neutral | Neutral |

Romania | Bearish | Bearish |

Turkey | Neutral | Neutral |

|

|

|

Bonds |

|

|

Czech Republic | Bullish | Bullish |

Hungary | Neutral | Neutral |

Poland | Neutral | Neutral |

Romania | Bearish | Bearish |

Turkey | Bearish | Bearish |

|

|

|

Exchange rates |

|

|

USD/All Emerging European Currencies | Bullish | Neutral |

EUR/CZK (Czech) | Neutral | Neutral |

EUR/HUF (Hungary) | Neutral | Neutral |

EUR/PLN (Poland) | Bearish | Neutral |

EUR/RON (Romania) | Neutral | Neutral |

EUR/TRY (Turkey) | Neutral | Neutral |

1. Macroeconomics

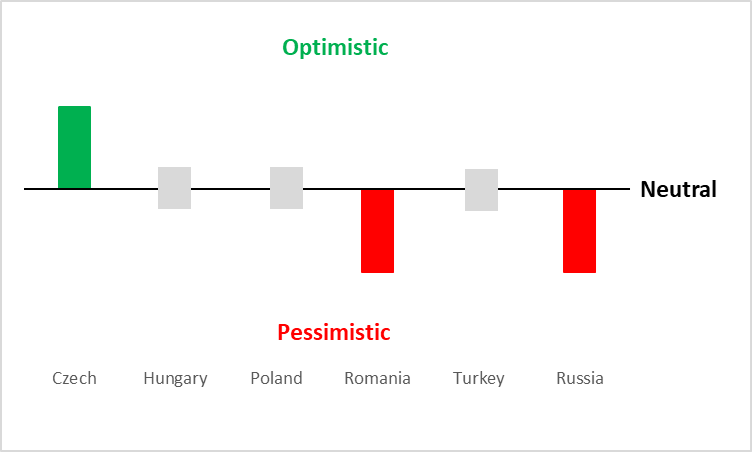

On 30 December 2024, we published a report titled "Emerging Europe Economics: Will the Region Experience a Stronger Growth in 2025?". In the report, we hold a positive macroeconomic outlook for the Czech Republic. In contrast, our outlook remains neutral for Hungary, Poland, and Turkey, while we are pessimistic about Romania and Russia (see Figure 1). This article builds on the previous report, delving into an analysis of the stock, bond, and foreign exchange markets in the region.

Figure 1: Emerging Europe macroeconomic outlooks

Source: Tradingkey.com

2. Stocks

2.1 Central and Eastern Europe (CEE)

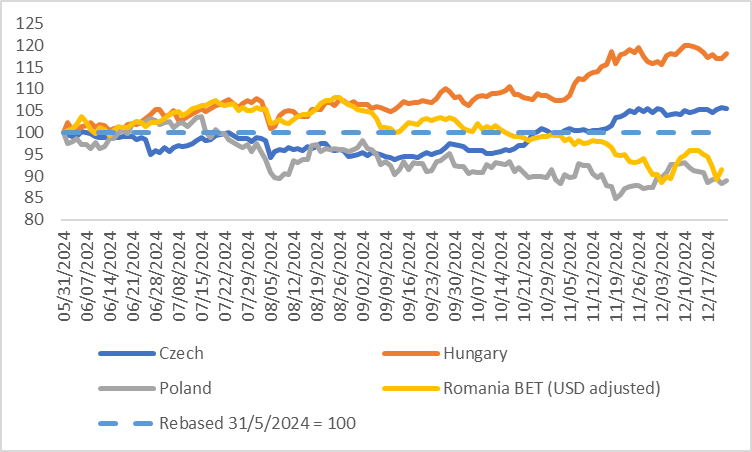

Since H2 2024, the performance of the four major countries in the MSCI index has diverged. As of today, Hungary and the Czech Republic have shown gains, while Romania and Poland have declined (Figure 2.1). Looking ahead, we are bullish on Hungary, neutral on the Czech Republic and Poland, and bearish on Romania.

Figure 2.1: MSCI CEE countries indices

Source: Refinitiv, Tradingkey.com

2.1.1 Czech Republic

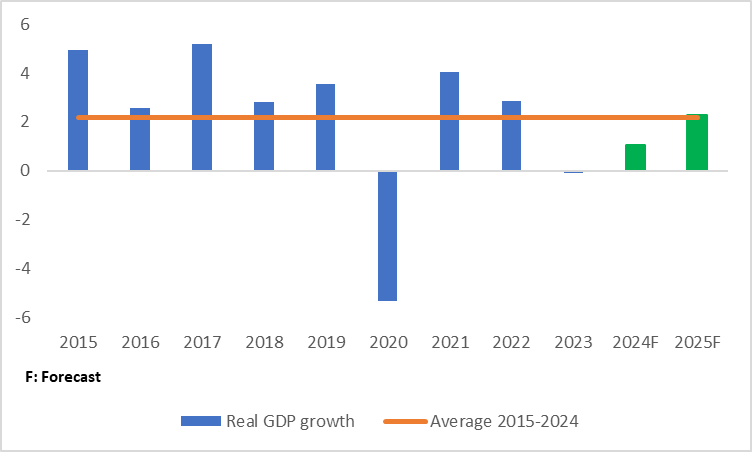

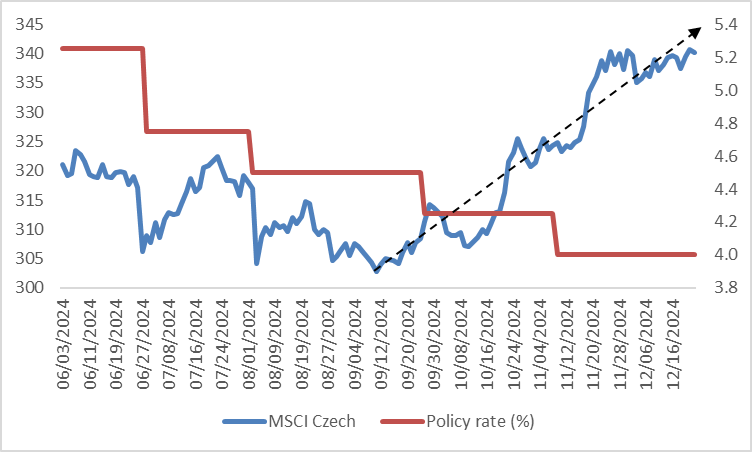

We maintain a neutral outlook on Czech stocks. On the positive side, improvements in consumption and fixed investment are expected to drive a continued economic recovery. Real GDP in the Czech Republic is projected to grow by 2.3% in 2025, significantly higher than those in 2023 and 2024, and slightly above the historical average of the past decade (Figure 2.1.1.1). This higher growth, combined with the loose monetary policy of the Czech National Bank (Česká národní banka, CNB), is likely to support the stock market (Figure 2.1.1.2).

However, the valuation of the Czech stock market is relatively high compared to other CEE countries, which may limit upside potential. Additionally, windfall taxes and stricter regulations are expected to weigh on the earnings of the utility sector, the largest component of the Czech stock index. The continued depreciation of the Czech koruna also dampens returns for US dollar investors. These factors collectively exert downward pressure on the market, offsetting potential support. As a result, we believe Czech stocks are likely to experience choppy trading.

Figure 2.1.1.1: Czech Republic real GDP growth (%)

Source: IMF, Tradingkey.com

Figure 2.1.1.2: MSCI Czech Index vs. Czech policy rate

Source: Refinitiv, Tradingkey.com

2.1.2 Hungary

In contrast to the Czech Republic, we are bullish on Hungarian stocks despite a neutral macroeconomic outlook. Four key factors support this view:

- The Hungarian economy entered a technical recession in mid-2024, prompting the government to implement a series of economic stabilization measures that could benefit the stock market.

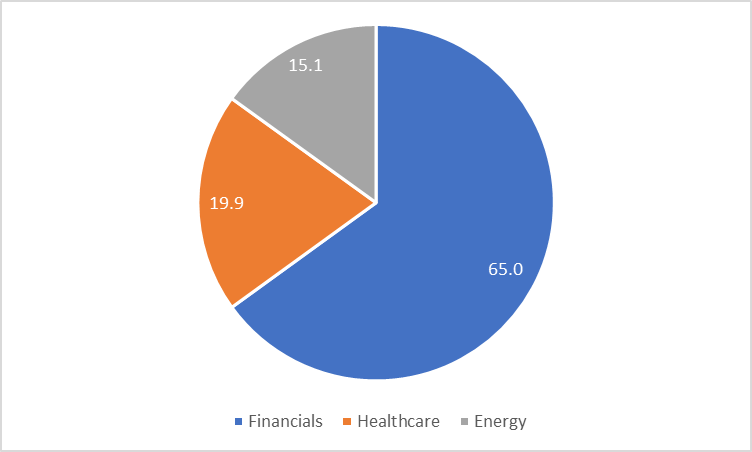

- The Hungarian National Bank (Magyar Nemzeti Bank, MNB) has recently adopted a more hawkish stance, which is particularly advantageous for the financial sector, the largest component of the Hungarian stock index, at least in the short to medium term (Figure 2.1.2).

- Two-thirds of the revenues of Hungarian listed companies are derived from overseas markets, and with global economic resilience expected to continue in 2025, these firms are likely to benefit.

- The Hungarian stock market remains one of the cheapest among all emerging markets, offering an attractive valuation.

Figure 2.1.2: MSCI Hungary Index sector breakdown (% of total)

Source: MSCI, Tradingkey.com

2.1.3 Poland

We expect Polish stocks to experience choppy trading as positive and negative factors balance each other out. On the positive side, Poland's higher-than-average wage growth and lower-than-average unemployment rates are likely to boost private consumption. Moreover, Poland is set to receive over €22 billion in EU funds by the end of 2025, which should support domestic fixed investment and, in turn, the stock market.

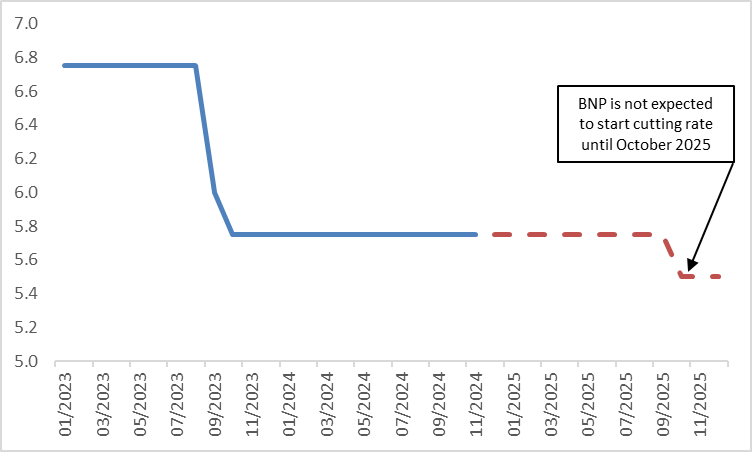

On the negative side, the fiscal deficit is worse than previously anticipated, leading to a significant rise in public debt. Geopolitical risks further cloud the outlook. Additionally, the National Bank of Poland (Narodowy Bank Polski, NBP) is unlikely to cut interest rates until October 2025, much later than other CEE central banks (Figure 2.1.3). While delayed rate cuts may benefit the financial sector, they could negatively impact the non-financial sector, creating mixed outcomes for the overall market.

Figure 2.1.3: Tradingkey’s forecast of Polish policy rate (%)

Source: Refinitiv, Tradingkey.com

2.1.4 Romania

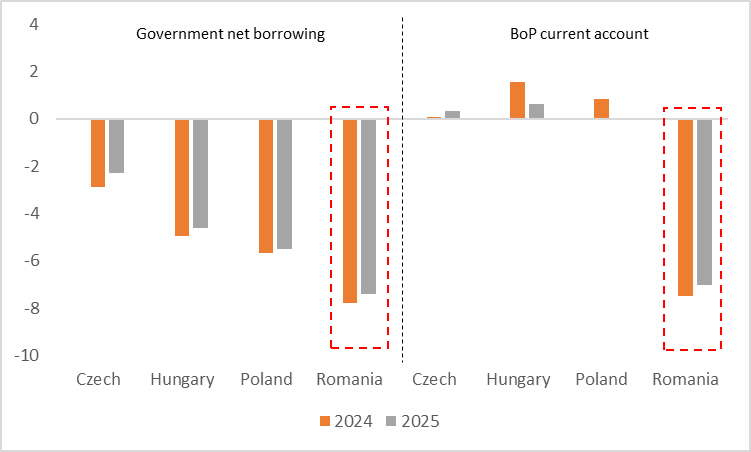

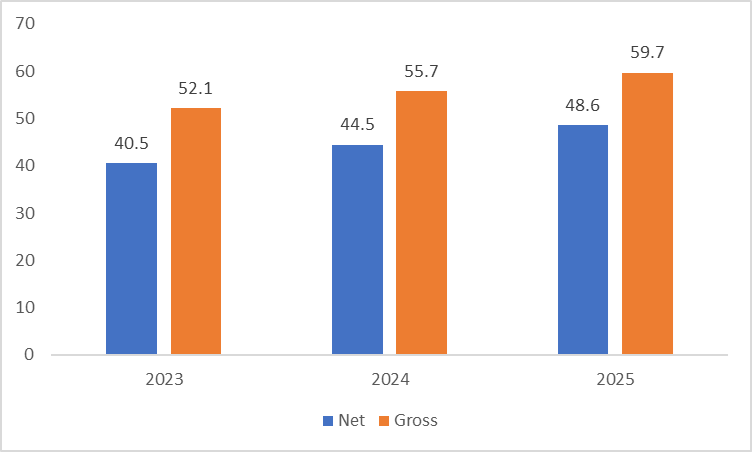

The MSCI Romania stock index has declined by approximately 10% since mid-year 2024. Persistent twin deficits (fiscal and balance of payments) pose significant challenges (Figure 2.1.4.1), with the IMF forecasting general government gross debt to rise from 52.1% of GDP in 2023 to 55.7% in 2024 and 59.7% in 2025 (Figure 2.1.4.2). These structural vulnerabilities increase Romania’s economic fragility.

Moreover, high inflation has constrained the National Bank of Romania (Banca Națională a României, BNR) from cutting interest rates, delaying improvements in financial conditions. Given these factors, we recommend underweighting Romanian stocks in the short to medium term.

Figure 2.1.4.1: IMF forecast of Romanian government borrowing and BoP current account (% of GDP)

Source: IMF, Tradingkey.com

Figure 2.1.4.2: IMF forecast of Romanian government debt (% of GDP)

Source: IMF, Tradingkey.com

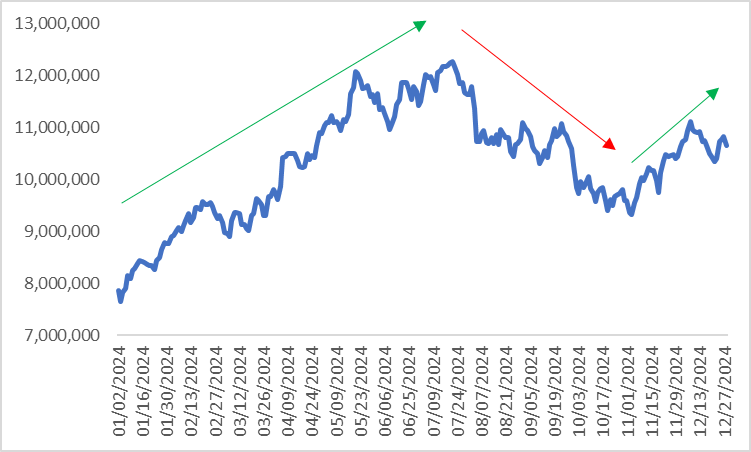

2.2 Turkey

In the summer and autumn of 2024, Turkish stocks declined due to increased global economic uncertainty and the domestic economy entering a technical recession. However, since November, the stock market has rebounded as high-frequency indicators, such as credit growth, PMI, housing sales, and the current account deficit, showed improvement (Figure 2.2).

Looking ahead, we assign a neutral outlook to the Turkish stock market, as positive and negative factors appear balanced. On the positive side, high-frequency data are expected to continue improving in the coming quarters, boosting investor appetite for domestic risk assets. On the negative side, Turkey's CPI remains elevated at over 40%, with little chance of falling to single digits in the short to medium term. Consequently, the Central Bank of the Republic of Türkiye (CBRT) is likely to maintain a hawkish monetary stance, which could weigh on the stock market.

Figure 2.2: MSCI Turkey Index

Source: Refinitiv, Tradingkey.com

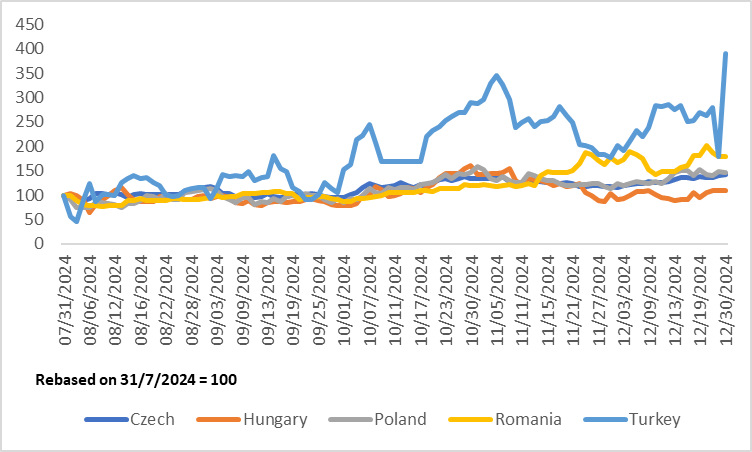

3. Bonds

Since August 2024, Turkey's government bond yields have seen the sharpest increase among Emerging European economies, driven by high inflation and interest rate hikes. In the CEE region, Romania has also experienced a significant rise in yields, primarily due to its persistent twin deficits (Figure 3). Looking ahead, these internal challenges are likely to continue exerting upward pressure on yields in both countries. Meanwhile, Hungary and Poland are expected to face volatile bond markets, influenced by a neutral macroeconomic outlook, supportive fiscal policies, and hawkish monetary stances.

Among major Emerging European economies, we only hold a mildly bullish view on Czech government bond prices. Relatively loose monetary policy is expected to apply downward pressure on yields. However, if Andrej Babiš secures victory in the parliamentary election in autumn 2025, increased government spending and investment aimed at economic recovery could lead to a higher supply of government bonds, potentially pushing yields upward. We anticipate that the downward pressure will outweigh the upward push, resulting in a slight decline in yields.

Figure 3: Emerging Europe government bond yields (bps)

Source: Refinitiv, Tradingkey.com

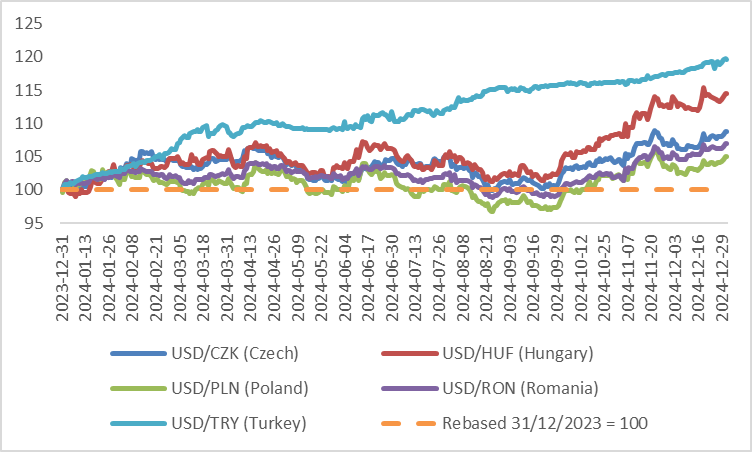

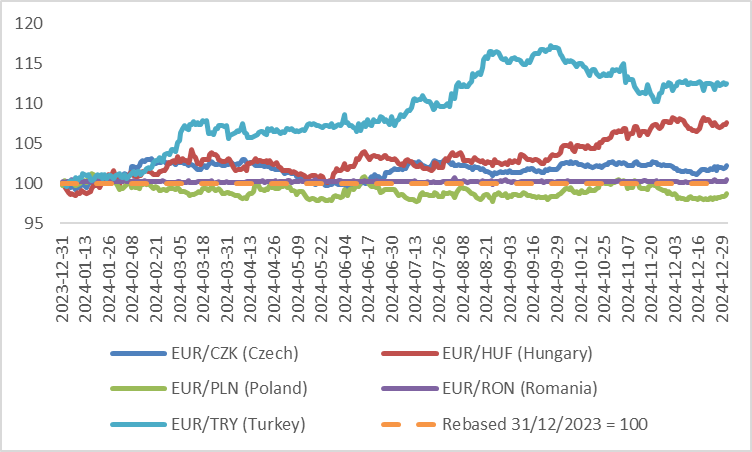

4. Exchange rates

In the report “Asset Allocation in Global Developed Markets: Bullish on Japanese Stocks” published on 24 December 2024, we expressed a bullish outlook on the USD index in the short term. As a result, all Emerging European currencies are expected to depreciate against the dollar. In the medium term, the decline of Emerging European currencies against both the dollar and the euro may stabilize, as the dollar and the euro are expected to weaken (Figures 4.1 and 4.2).

Notably, in the short term, the Polish złoty may appreciate against the euro. This is primarily due to the NBP slowing down its pace of rate cuts. On 5 December 2024, NBP Governor Adam Glapiński announced in a press conference that the first-rate cut would be postponed from March to October 2025. This delay could provide upward support for the złoty in the near term.

Figure 4.1: USD/Emerging European currencies

Source: Refinitiv, Tradingkey.com

Figure 4.2: EUR/Emerging European currencies

Source: Refinitiv, Tradingkey.com

.jpg)