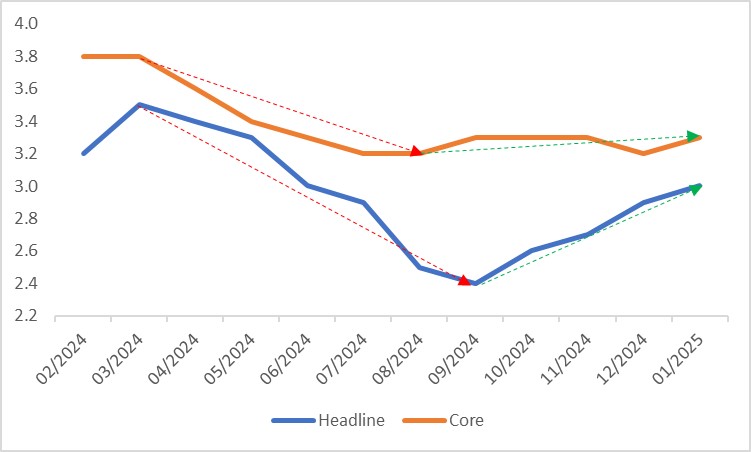

U.S. February CPI Preview: Is the Era of Stagflation Approaching?

On 12 March 2025, the United States will release the Consumer Price Index (CPI) data for February. Market consensus predicts that the year-over-year growth rates for Headline CPI and Core CPI will reach 2.9% and 3.2%, respectively, both lower than the previous figures of 3.0% and 3.3% (Figure 1). We align with this market outlook.

Figure 1: U.S. CPI forecasts

Source: Refinitiv, Tradingkey.com

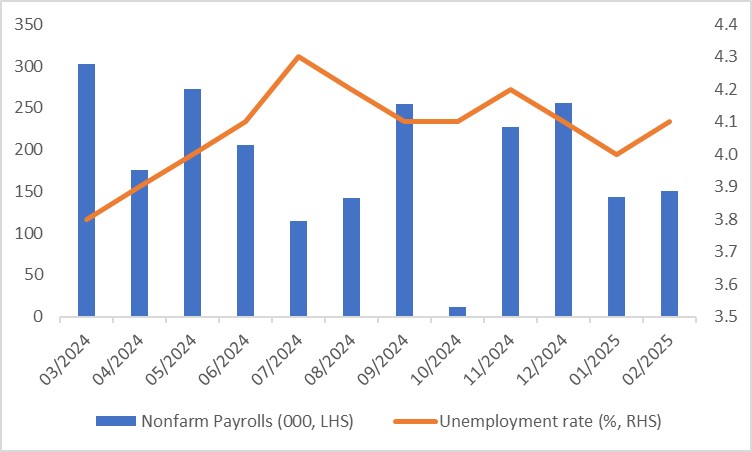

Since September of last year, U.S. inflation has been gradually rising due to the Federal Reserve slowing its pace of rate cuts, the subsequent pause in rate reductions and the impact of Trump’s high tariffs (Figure 2). The primary driver behind the anticipated decline in February’s CPI is the softening U.S. labour market. Recent February non-farm payroll data fell short of expectations, dragged down by weaker employment in government and retail sectors, while the unemployment rate for the same month edged higher (Figure 3). Combined with the recent economic slowdown in the U.S., these factors are expected to exert downward pressure on February’s CPI.

Figure 2: U.S. CPI (%)

Source: Refinitiv, Tradingkey.com

Figure 3: U.S. labour market

Source: Refinitiv, Tradingkey.com

However, persistent inflation in sub-categories such as food, used cars and trucks limits the likelihood of a significant drop in February’s inflation. Therefore, a modest decline of 0.1 percentage points in both Headline CPI and Core CPI year-over-year, compared to January, appears reasonable.

Looking ahead, inflation faces opposing forces: downward pressure from the economic slowdown and upward pull from high tariffs. If the former prevails and inflation continues to decline—a scenario we consider highly probable—the Federal Reserve is likely to implement more substantial rate cuts. Conversely, if inflation rebounds, the U.S. could enter a period of stagflation, placing the Fed in a challenging dilemma.

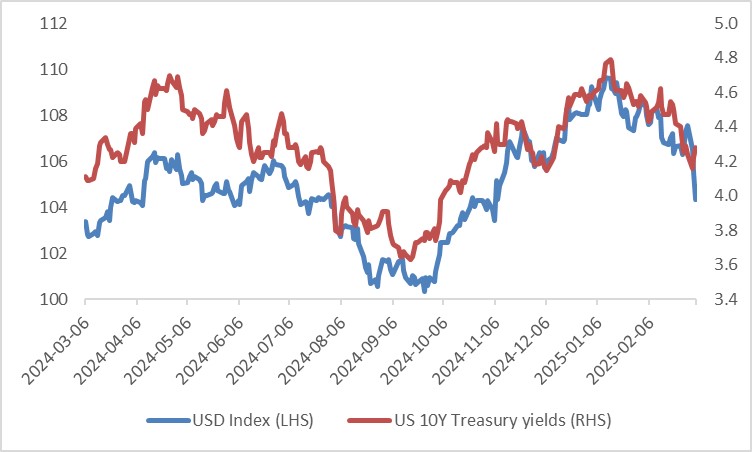

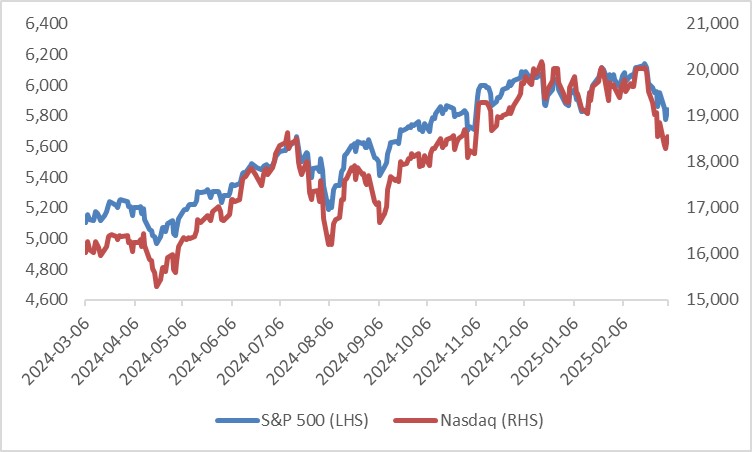

Assuming our projections and the market consensus are correct, the anticipated 0.1 percentage point drop in February’s inflation is already priced in. As a result, when the data is released, we expect limited volatility in the foreign exchange, bond, and stock markets (Figures 4 and 5).

Figure 4: USD Index and US 10-year Treasury yields

Source: Refinitiv, Tradingkey.com

Figure 5: U.S. Stocks

Source: Refinitiv, Tradingkey.com