Here’s Why U.S. Treasury Yields Are Continuing to Climb

TradingKey - Entering 2025, the yield on the U.S. 10-year Treasury note has continued its upward trajectory. Following the release of two critical economic data points on Tuesday, long-term Treasury yields climbed further. In contrast, the tech-heavy Nasdaq Composite Index fell 1.9%, and the S&P 500 Index declined 1.1%.

Source: TradingView

Here are the main factors driving the continued rise in U.S. Treasury yields.

Strong Economic Data Lowers Rate Cut Expectations

The ISM Services Prices Index rose to 64.4 in December from 58.2 in November, while the JOLTS revealed job openings exceeded forecasts.

The ADP private payroll, due Wednesday, is expected to show a gain of 130,000 jobs in December. On Friday, the Bureau of Labor Statistics will release the December jobs report, including nonfarm payrolls and the unemployment rate.

Gennadiy Goldberg, Head of U.S. Rates Strategy at TD Securities, stated that the data gives the impression of a reaccelerating U.S. economy. However, positive seasonal factors may have overstated the strength, making this a key driver of Treasury market movements.

Strong labor market and services sector data have led investors to scale back expectations for Fed rate cuts this year, with markets now pricing in only one rate cut. This shift triggered a sell-off in equities on Tuesday and pushed government Treasury yields higher.

Rising yields pose challenges for existing Treasury holders, as they reflect more sellers than buyers in the market, leading to a decline in overall Treasury prices. Yields and Treasury prices move inversely

Policy Uncertainty Under Trump and Inflation Risks

With two weeks remaining until President-elect Donald Trump's inauguration, concerns are mounting over his proposed tariffs and their potential inflationary impact. Trump denied a report by The Washington Post on Monday, which claimed that his transition team might be considering scaling back tariffs. He said in a Truth Social post that the article “incorrectly states that my tariff policy will be pared back. That is wrong.”

Beyond tariffs, the bond market is also concerned about Trump’s campaign proposals, such as tax cuts and the elimination of the gratuity tax and Social Security payroll tax, which could lead to increased government borrowing to cover the gap between spending and revenue.

The nonpartisan Committee for a Responsible Federal Budget estimates that Trump’s fiscal proposals could add $7.8 trillion to the national debt over the next decade.

Weak Demand in Long-Term Treasury Auctions

One factor driving long-term Treasury yields higher is supply pressure, as demand for the first two of this week’s three Treasury auctions has been weak.

On Monday, the U.S. Treasury auctioned $58 billion in 3-year notes, which saw subdued demand. The awarded yield was 4.332%, 1 basis point higher than the yield in the secondary market prior to the auction. On Tuesday, the $39 billion auction of 10-year Treasuries also showed poor demand, with an awarded yield of 4.680%, the highest since August 2007. On Wednesday, the Treasury is set to auction $22 billion in 30-year Treasuries.

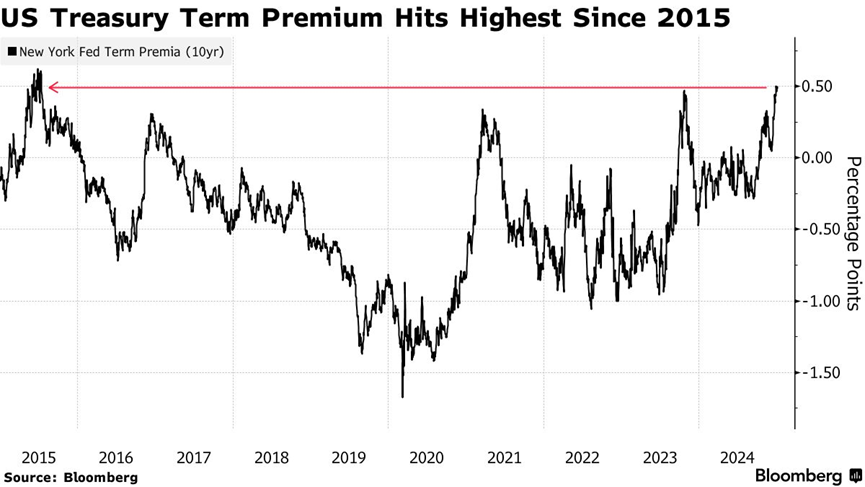

Term Premium Rises to Elevated Levels

Torsten Slok, Chief Economist at Apollo Global Management, warned that the rapid increase in Treasury yields could destabilize the bond market, raising concerns among investors.

The yield on the 10-year Treasury currently stands at 4.68%, its highest level since May 2024, with Wall Street analysts cautioning that a 5% yield is on the horizon.

Another sign of stress in the bond market is the rising term premium, an indicator that reflects the extra yield investors demand for holding long-term Treasuries rather than rolling over short-term securities as they mature. This metric has recently reached its highest level since 2015.

Source: Bloomberg