Here’s Why the US Fed Just Caused the S&P 500 Index to Plunge 3%

TradingKey - Interest rates have been the big topic of discussion in global stock markets over the past 18 months and that’s not going to change any time soon. As usual, the discussion is centred around the US Federal Reserve – the world’s biggest central bank – and its Fed Funds rate.

On Wednesday (18 December), the Fed concluded its latest two-day Federal Open Market Committee (FOMC) meeting. As expected, the central bank cut the Fed Funds rate by 25 basis points (bps), or 0.25%, to a range of 4.25% to 4.50%.

It was a near-unanimous decision, with 11 members of the 12-member FOMC voting in favour and only one voting against a cut.

Yet despite the action taken to cut, the S&P 500 Index ended the day down 3% after Fed Chairman Jerome Powell gave his press conference. Here’s why the stock markets had a tantrum at what the Fed Chair had to say about where interest rates are headed.

Fed adopts more hawkish approach

As most seasoned investors will know, stock markets are forward looking and the rate cut that took place on Thursday was already priced in by investors (i.e. they expected it). Markets generally react to the unexpected and that’s what was served up by Chairman Powell in his press conference.

Markets were bracing themselves for the possibility of a more “hawkish” tone from the Fed and that’s unfortunately what they got. Fed Chair Powell stated that the central bank had lowered its policy rate by a full percentage point from the peak and that “our policy stance is now significantly less restrictive”.

However, he went on to say that “we can therefore be more cautious as we consider further adjustments to our policy rate”. While he conceded that the Fed is “on track to continue to cut”, he did clarify that the Fed would have to see more progress on inflation before doing this.

Inflation and tariffs heading into Trump 2.0

The problem here is that inflation has been taking a lot longer than expected to come back down to the Fed’s 2% target. The latest Personal Consumption Expenditure (PCE) price index, the Fed’s preferred measure of underlying inflation, saw November’s PCE price index increase by 2.3% year-on-year.

However, the core PCE price index, which strips out more volatile food and energy items, was up 2.8% year-on-year and suggests inflation is still not as close to where the Fed wants it to be. That’s also complicated by potential trade tariffs by the incoming Trump administration.

Fed Chair was asked about potential tariffs from the incoming administration and responded by saying policymakers don’t know much about the actual policies that will be implemented. As a result, he conceded that “it’s very premature to try to make any kind of conclusion”.

While that’s true, it’s also an admission that the Fed is erring on the side of caution and will look to hold rates more steady until policies from “Trump 2.0” becomes clearer and, more importantly, what impact those policies will have on inflation.

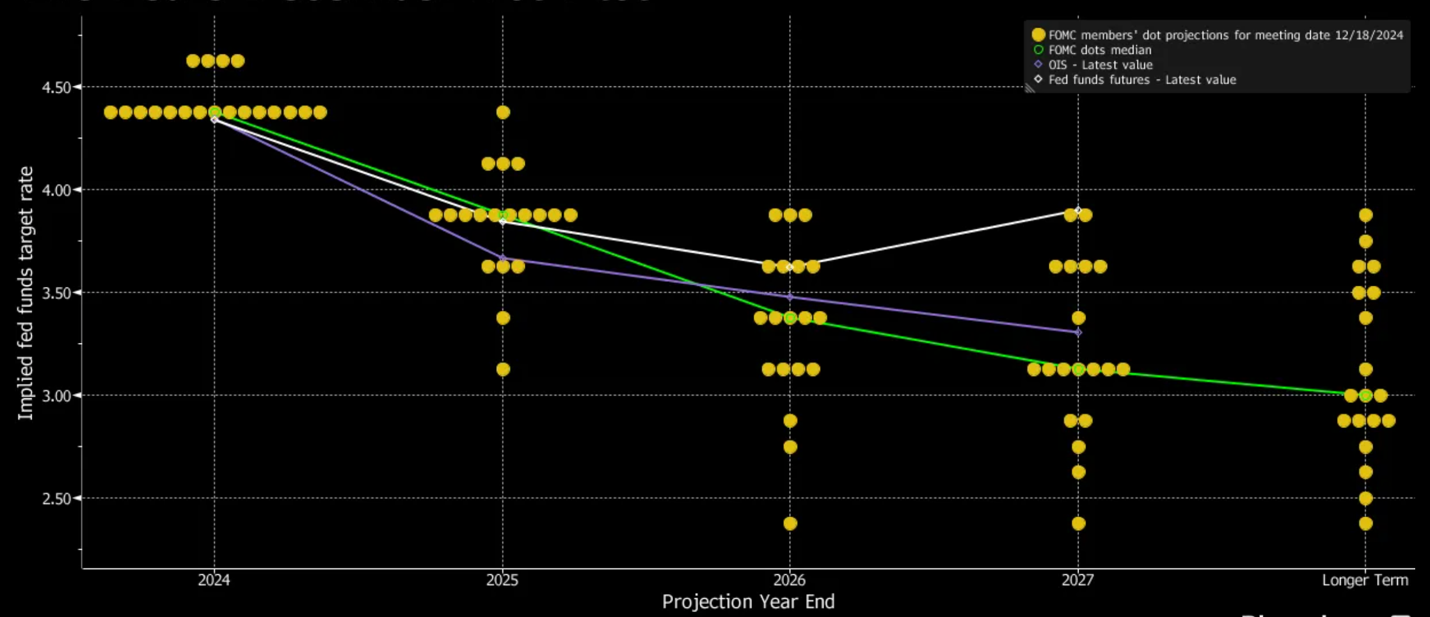

Fed’s dot plot suggests fewer rate cuts in 2025

That’s exactly how the Fed painted the picture for investors as the Fed’s “dot plot” (that is released quarterly to the public) showed fewer than expected rate cuts from the central bank. Inflation remains higher than the FOMC’s members want to see and employment still remains strong, albeit slightly weaker than earlier this year.

All the data, along with uncertainty on government policies, point towards the likelihood that the Fed is going to be much more conservative going forward.

The Fed’s December 2024 dot plot

Sources: Bloomberg, FOMC

So it might be surprising to find that the market itself was taken by surprise that the latest dot plot showed that the FOMC’s median Fed Funds rate projection for the end of 2025 now sits at 3.75%. That’s up from the 3.38% end-2025 projection in in September’s dot plot and implies just two interest rate cuts next year.

Significantly less than the market was hoping, the refreshed dot plot projections also accelerated the selloff in the S&P 500 Index after Chairman Powell’s press conference.

Where’s the neutral policy rate?

Longer term, the question of where the “neutral” rate lies was raised. This so-called neutral rate is where policy rates neither promote nor restrict growth and, thus, is considered a balance between the two.

Although hypothetical in context, the suggestion is that neutral rate has moved higher “post-pandemic” as the world moves into a new structural phase of de-globalisation and persistently higher prices. Officials at the Fed raised their projections of where the Fed Funds rate will settle over the long term at 3%, up slightly from 2.9%.

That’s significantly higher than what investors were used to in the post-GFC to pre-pandemic days (2009-2020). For investors who have been riding the recent all-time highs set by the S&P 500 Index and tech stocks, it suggests that it might not all be plain sailing in 2025 when it comes to interest rates and the Fed.