Gold vs. Bitcoin: Which Is the Better Investment in 2025?

Federal Reserve Chair Powell stated that Bitcoin is not a competitor to the dollar but rather a competitor to gold. Bitcoin, now referred to as "digital gold," has attracted significant attention, especially after the elections. Some traditional institutions have already chosen to include Bitcoin in their investment portfolios. So, which one will be better investment in 2025? I will analyze this from the following perspectives:

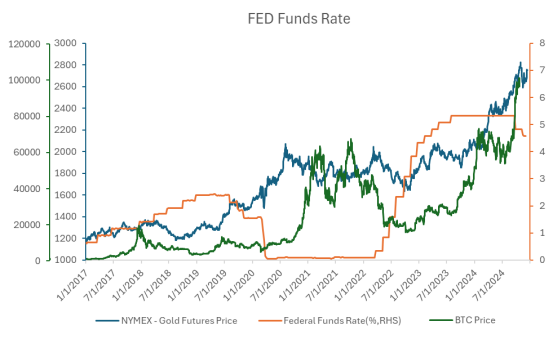

Favorable Macro Environment

The U.S. added 227,000 new jobs in November, marking the largest increase in six months, but the unemployment rate unexpectedly rose to 4.2%. While the job market remains robust, the rise in the unemployment rate has increased bets on a Federal Reserve rate cut in December. The market currently expects a 25 basis point rate cut in December, but Fed Chair Powell's tone may remain hawkish. Both gold and Bitcoin thrive in a loose monetary environment. If the Fed continues to cut rates or potentially pauses quantitative tightening (QT), this will increase market liquidity and boost risk appetite.

Source: Reuters, CoinCodex

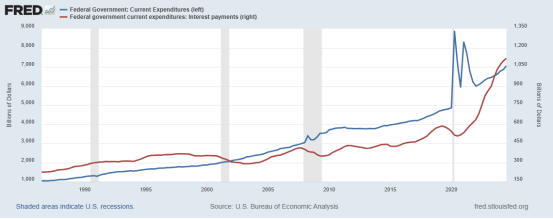

Additionally, U.S. government spending and interest expenses are rising rapidly, creating significant debt servicing pressure. Interest payments have become the second-largest item in the government's budget, and the Treasury is continuously issuing new bonds to repay old debts. Gold and Bitcoin benefit from this situation because they can act as hedges against fiat currency devaluation.

Source: FRED

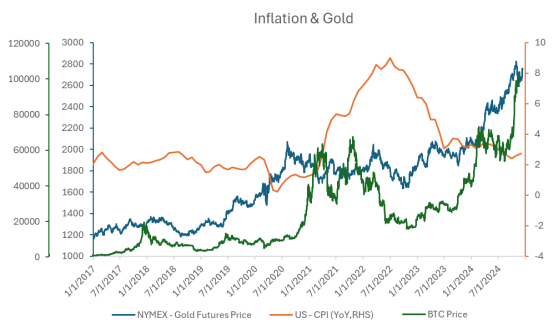

Inflation Hedge

The U.S. CPI for November showed a month-over-month increase of 0.3% and a year-over-year increase of 2.7%. Core CPI also rose by 0.3% month-over-month for the fourth consecutive month. In recent months, inflation cooling has largely stagnated. Goods inflation has reached its lower bound, and service inflation will become the focus of the Federal Reserve's efforts to reduce inflation. Rent remains the most stubborn component of inflation, rising 4.7% year-over-year in November.

The current market consensus expects the Federal Reserve to pause rate cuts in January next year, as inflation has not declined further, and the potential tariffs that President Trump plans to impose on countries like China could pose an upward risk to inflation. Both gold and Bitcoin can serve as hedges against inflation resurgence to preserve purchasing power, especially if the Fed does not aggressively tighten monetary policy. However, if the Fed tightens aggressively to combat inflation in the future, gold may outperform Bitcoin, as Bitcoin is highly volatile and significantly influenced by short-term market sentiment.

Source: Reuters, CoinCodex

Limited Supply

Both gold and Bitcoin are considered scarce resources, with the amount that can be mined decreasing year by year.

Gold:

1. Current Supply and Distribution:

• Total Mined Gold: Approximately 212,582 tonnes of gold have been mined according to World Gold Council.

2. Distribution:

• 45% used in jewelry.

• 22% in bars and coins

• 17% held by central banks.

3. Proven Reserves: Around 59,000 tonnes, which means only 20% of all gold on earth remains to be mined.

4. Annual Production:

• Gold producers mine approximately 3,000 tonnes of gold each year.

• Reserve Depletion: At this rate, gold reserves could be depleted in less than 20 years.

Bitcoin:

1. Total Supply:

• The maximum supply of Bitcoin is 21 million BTC, hard coded into the protocol.

• Current Mining: As of December 2024, approximately 19.54 million Bitcoins have been mined according to Blockchain.com, leaving only 7% to be mined.

2. Distribution:

• Retail Investors: 40-50% held by retail investors.

• Institutional Investors: 10-20% held by institutional investors, with this number growing.

• Exchanges: 10-15% held by exchanges, such as Binance, which holds over 600,000 BTC.

• Whales: 10-15% held by large individual investors.

• Lost Bitcoins: approximately 20%.

3. Halving Mechanism:

• Bitcoin has a halving mechanism that reduces the supply of new Bitcoins over time.

• Mining Schedule: All Bitcoins are scheduled to be mined by 2140.

Increasing Demand

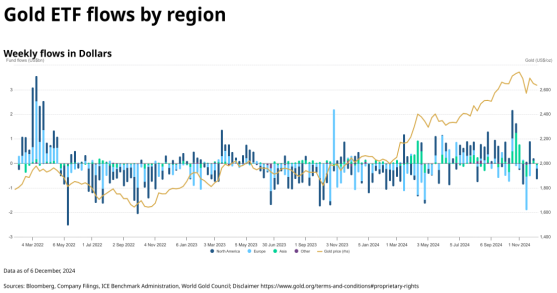

The inflows into gold ETFs reveal significant investor behavior trends. Asian investors have been highly enthusiastic about gold ETFs, with significant fund inflows beginning in April. Interestingly, the People's Bank of China (PBOC) stopped purchasing gold from April. This suggests that retail investors seemed to take over the relay of gold's upward momentum after the central bank halted its purchases. The PBOC restarted gold purchases in November after a period of price correction, which boosted investor confidence and led to a rebound in gold prices. Besides China, India, Turkey, and Poland have also been major buyers of gold, reaching a peak in purchases in October. It is expected that central banks in these countries will continue to purchase gold. The global central banks have been buying over 1,000 tons of gold for two consecutive years, a trend that could continue, supporting long-term demand.

U.S. investors had relatively large inflows into gold ETFs helping the price of gold exceed $2,200, and continued large inflows after August. European investors have been more pessimistic about gold, with only a small number of net inflows in the third quarter, with huge amount of outflows in November.

Source: World Gold Council

According to the World Gold Council, weekly net inflows into gold ETFs typically range around 1 billion dollars, with the highest weekly inflow exceeding 2 billion.

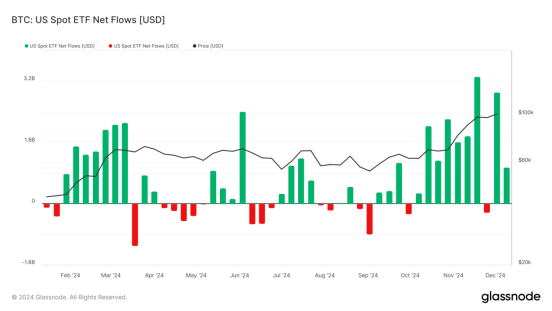

The approval of Bitcoin ETFs by the U.S. Securities and Exchange Commission (SEC) has opened new avenues for retail investors to participate in Bitcoin investment through traditional securities markets. This development has made it more convenient for funds to flow into Bitcoin, as investors can now access Bitcoin through familiar and regulated platforms. Data from Bitcoin spot ETFs indicates that there have been 16 weeks with net inflows exceeding 1 billion dollars, with the highest weekly inflow surpassing 3 billion.

Source: Glassnode

Bitcoin ETFs have seen significantly higher weekly inflows compared to gold ETFs, indicating strong investor interest and potentially higher liquidity. BTC spot ETFs are primarily driven by U.S. investors, who show higher enthusiasm for Bitcoin compared to gold. This is particularly evident around the U.S. elections, where higher liquidity provides more opportunities for speculation.

President Trump has proposed building a national Bitcoin reserve. If more countries follow this approach, it could lead to a significant shift in how Bitcoin is viewed and utilized.

Growth Potential

Both gold and Bitcoin offer unique growth potential and risk profiles, making them suitable for different types of investors. Historically, gold has grown at a compounded rate of 10% annually over 20 years. Based on this historical growth rate, gold could reach a price of $3,000 next year. Gold's maturity and lower volatility make it a stable asset, ideal for preserving wealth during uncertain times.

Bitcoin’s historical annualized growth rate is 70% for the last 10 years, but this might slow down as more institutional investors join. It would not be a surprise if BTC reaches $150000 next year. Bitcoin is highly popular among younger generations, with exponential growth potential.

The regulatory environment for cryptocurrencies, particularly under Trump presidency, will become more favorable, enhancing Bitcoin's legitimacy and demand. Gold's upside is relatively limited compared to Bitcoin. For investors with a long-term horizon and high-risk tolerance, Bitcoin could outperform gold.

.jpg)