Alibaba's Stock Soars After Q3 Earnings Report, Significant Upside Potential Ahead!

TradingKey - Alibaba shares continue with their rally after strong Q3 results, riding on the AI frenzy.

- Net Income: 48.95 RMB bn vs. 40.60 RMB bn expected (+240% year-over-year)

- Revenue: 280.154 RMB bn vs. 279.340 RMB bn expected (+8% year-over-year)

Cloud revenue was up 13% year-over-year, with the AI product within the business growing at triple digits. In the AI field, the Alibaba language model Qwen is gaining traction, along with Apple's cooperation within the country.

Similar to what US tech giants are currently doing, BABA will support the further development of the AI-related tools and infrastructure by increasing the capex and R&D expenses significantly. The investments in the coming three years are set to exceed the amount invested in the last ten years, likely to be distributed in three equal parts.

In the core e-commerce business, BABA achieved 5% growth in its domestic platforms, Taobao and Tmall, and 32% in its overseas businesses such as Lazard and AliExpress. Both of these figures were higher than in previous quarters. This can be attributed to the introduction of AI tools like Quanzhantui and aggressive user acquisition overseas.

Profitability also improved as the total operating margin improved to 15% from 9% in the 2024 Q3. A large contribution here is the improved operating performance of Local Services Group with Amap and Ele.me getting closer to breakeven.

The outlook for Alibaba hasn’t been more optimistic in the last five years. With the expectation of more government support and fast-growing AI, Alibaba is well-positioned to be the Chinese answer to Amazon. Considering the PE ratio of Alibaba is just 28x compared to Amazon’s 40x, there is still plenty of room for growth.

Related Articles

Rivian Reaches Key Milestones, Yet Faces Headwinds Ahead

TradingKey - Rivian has announced an important milestone in february 20, reporting its first-ever "positive gross profit" for the fourth quarter of 2024.

Walmart Stock Drops 6% After Q4 FY2025 Earnings: 5 Key Takeaways for Investors

TradingKey - The US consumer has remained strong over the past few years, despite higher inflation and higher interest rates. That may have surprised some market watchers but certain listed companies have cashed in on this strength in the US consumer.

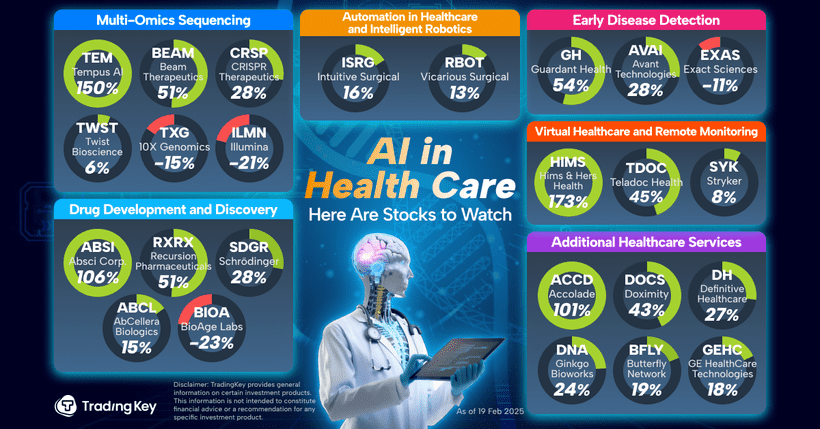

What Are the Catalysts Driving the Surge in AI Healthcare Stocks?

TradingKey - The healthcare sector is experiencing a resurgence in 2025 after two years of underperformance, primarily driven by advancements in artificial intelligence (AI).

Thailand: No Opportunity in the Stock Market, What About the Bond Market?

Looking ahead, although potential tariffs may introduce uncertainty to Thailand's foreign trade, fiscal spending is expected to continue supporting the economy.

6 Key Takeaways From Amazon’s Q4 2024 Earnings

TradingKey - For tech investors, no other company exemplifies sheer size than Amazon.com Inc (NASDAQ: AMZN). The company pulls in over US$150 billion in sales per quarter due to its massive e-commerce business and cloud computing arm.