2026 Global Top Seven Storage Giants Ranking: Kioxia and SanDisk Lead Gains, Who Is Strongest in the AI Storage Supercycle?

The 2026 AI memory supercycle has driven historic gains across the sector. SK Hynix leads in HBM market share (58%), while Samsung and Micron remain key competitors. NAND providers Kioxia and SanDisk have seen exponential growth following valuation re-ratings. HDD manufacturers, including Seagate and Western Digital, benefit from persistent cold storage demand. Despite strong Q1 performance and supply shortages projected through 2027, the sector faces significant risks: record-high pricing, potential technological hurdles in HBM4 development, and elevated valuations. Investors should exercise caution, as any negative earnings surprise or demand shift could trigger sharp, volatile market corrections.

TradingKey - Since the start of 2026, the Philadelphia Semiconductor Index (SOX) has surged by over 95%, with memory chips serving as the primary driver. Against the backdrop of the index's upward trajectory, the market capitalizations of the three major DRAM giants have successively surpassed $1 trillion. In the NAND sector, two individual stocks have seen gains of over 47-fold over the past year, while mechanical hard drive manufacturers are also undergoing a valuation rerating driven by AI data storage demand. So, who is the strongest performer in this round of the AI memory supercycle?

Comparison of Core Metrics for the Seven Major Memory Manufacturers (as of June 19)

Company | YTD Gain | 1-Year Gain | Market Cap | Core Business |

Samsung Electronics | Approx. 194% | Approx. 485% | Approx. $1.52 trillion | DRAM+HBM+NAND |

SK Hynix | Approx. 324% | Approx. 1020% | Approx. $1.32 trillion | DRAM+HBM+NAND |

Micron Technology | Approx. 284% | Approx. 840% | Approx. $1.28 trillion | DRAM+HBM+NAND |

Kioxia | Approx. 856% | Approx. 5200% | Approx. $307 billion | NAND+SSD |

SanDisk | Approx. 796% | Approx. 4750% | Approx. $323.5 billion | NAND+SSD |

Western Digital | Approx. 321% | Approx. 1170% | Approx. $257.2 billion | HDD+NAND |

Seagate Technology | Approx. 279% | Approx. 710% | Approx. $240 billion | HDD |

The HBM Big Three: SK Hynix Leads, Samsung Catches Up, Micron Seeks Breakthrough

HBM is currently the subsector within the memory space with the highest profit margins and the strongest technical barriers.

Company | HBM Shipment Market Share | Q1 2026 Operating Profit | P/E Valuation |

Samsung Electronics | Approx. 21% | Approx. 57.2 trillion KRW | P/E ratio of approx. 25x; forward P/E of only approx. 7x |

SK Hynix | Approx. 58% | Approx. 37.6 trillion KRW | P/E ratio of approx. 19x; forward P/E of approx. 5.5x |

Micron Technology | Approx. 21% | Market expects its Q3 FY2026 EPS to be $19.72 | P/E ratio of approx. 48x; forward P/E of approx. 10x |

SK Hynix (000660): Firmly holds the top spot with an approximate 58% shipment market share, boasting an operating margin of up to 72%, and publicly showcased 12-layer 48GB HBM4E samples in June. Its leadership stems from securing an early position in Nvidia's HBM3E supply chain, though it must remain vigilant against Samsung's potential counterattack in the HBM4 generation.

Samsung Electronics (005930): Its Q1 2026 operating profit of approximately 57.2 trillion KRW set a single-quarter record for South Korean enterprises, with an HBM market share of around 21%. On May 29, it became the first to deliver its initial batch of 12-layer 48GB HBM4E samples to global customers, showcasing the unique advantages of its integrated IDM model in terms of synergistic effects.

Micron Technology ( MU ): Its Q1 2026 DRAM revenue grew 81.6% quarter-on-quarter, leading the three giants, with an HBM market share of about 21%, and its HBM4 mass production milestone is set for Q2 2026, later than its Korean rivals. While Micron's 2026 HBM capacity is already sold out, the capital market is split on whether it can close the gap in the HBM4E generation. Its current year-to-date gain of approximately 250% already factors in a high degree of optimism, making its Q3 fiscal earnings report on June 24 a crucial test. If calculated based on the current market consensus EPS of $19.72 and Micron's approximately 1.14 billion shares outstanding, the corresponding non-GAAP net profit would be about $22.5 billion.

The New Rising Star of NAND Flash: The King of Global Gains Fueled by AI Data Centers

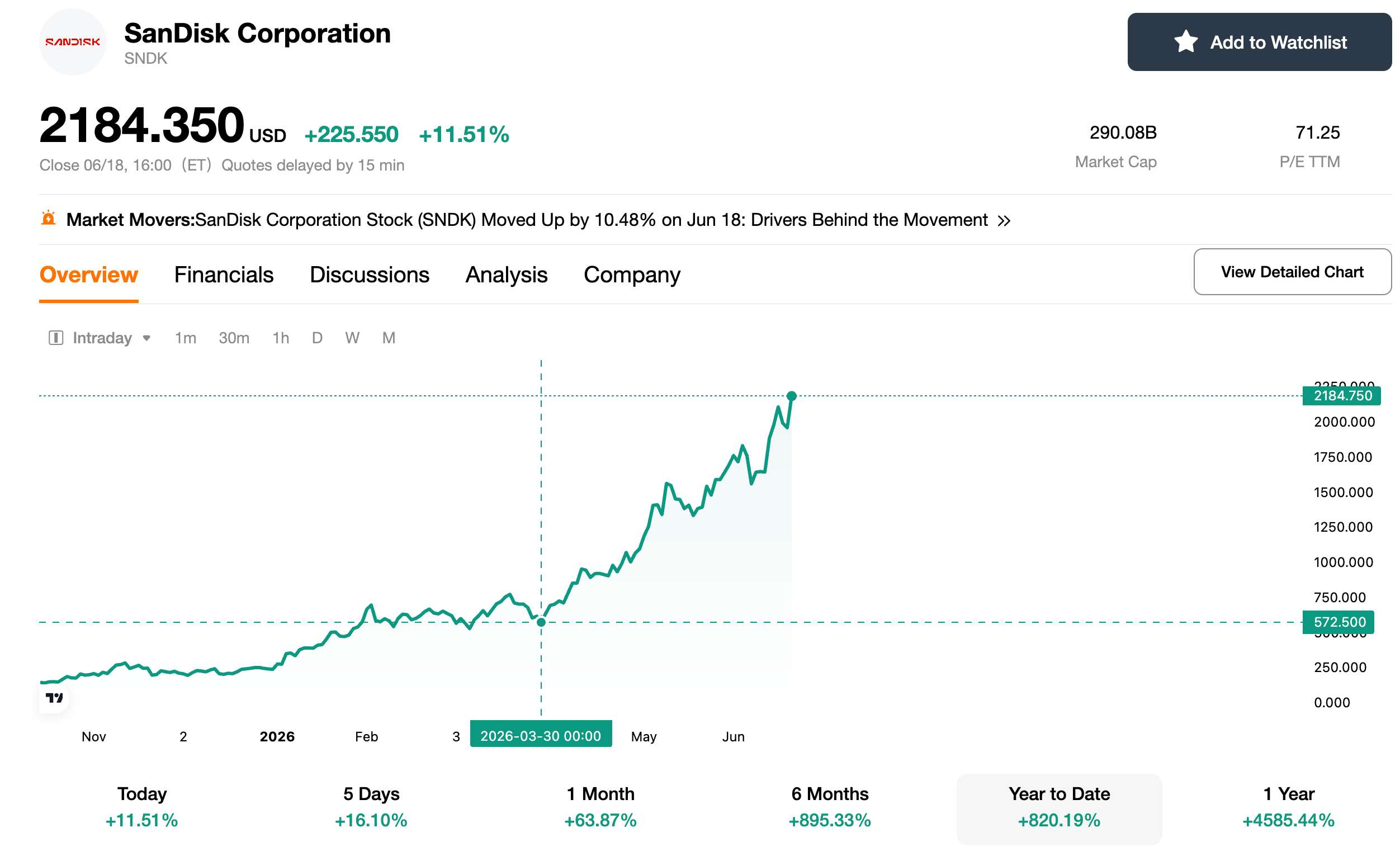

SanDisk (SNDK): A Legendary 45-Fold Rally in One Year

[Source: TradingKey]

SanDisk is one of the most astonishing tech stocks in terms of global share price gains in 2026. On June 18, Eastern Time, SNDK's stock price rose over 11% to close at $2,184, hitting another historic high and representing a cumulative gain of over 45 times from its 52-week low of approximately $36 in 2025. Its year-to-date gain has exceeded 820%, achieving a valuation rerate in just half a year that had eluded the company for more than a decade.

The spinoff was the core catalyst for the valuation rerate. In February 2025, SanDisk went public independently from Western Digital. Freed from the income statement structure of the HDD business, the market was able to value it using a pure-play NAND provider pricing model, no longer dragged down by a conglomerate discount. From a fundamental perspective, SanDisk's data center revenue in Q1 2026 jumped over sixfold year-over-year, with enterprise SSDs becoming one of the fastest-growing business lines in this storage cycle.

Kioxia (285A), Japan's Strongest Memory Chip Stock

[Source: TradingView]

On June 12, 2026, Kioxia's market capitalization reached 44.36 trillion yen, surpassing Toyota Motor to claim the top spot in Japan by market value, unseating Toyota from its 22-year reign just 18 months after going public. As of the close on June 19, Kioxia's year-to-date stock gain exceeded 850%, with its gain over the past year soaring by more than 52 times, putting it at the top of the MSCI World Index constituents' gainers list.

In terms of financial performance, Kioxia's Q1 2026 revenue reached 1.0029 trillion yen, surging 189% year-over-year; its operating profit soared nearly 15-fold to 596.8 billion yen, hitting a quarterly record high. The company expects Q2 revenue to reach 1.75 trillion yen and operating profit to hit 1.3 trillion yen, with an operating margin exceeding 74%. Based on these projections, Kioxia's full-year operating profit for 2026 is poised to break 4 trillion yen, with its profitability potentially eclipsing that of Toyota.

The HDD Duopoly: Quiet Winners of AI Cold Data

While the market is frantically chasing HBM and SSDs, the hard disk drive (HDD) duopoly is emerging as the invisible winners of AI infrastructure through a completely different logic.

Seagate Technology ( STX )

has gained approximately 279% year-to-date in 2026, with a market capitalization of around $240 billion. The company's guidance shows that its high-capacity nearline hard drive capacity for the entire year has been sold out, and it has begun accepting orders for 2027. The CEO pointed out that approximately 90% of AI data falls under warm/cold data, which requires HDD storage. While this logic holds, the HDD market is essentially one of replacement (SSDs will erode HDD market share once prices for high-capacity SSDs fall).

Seagate's 40TB products based on HAMR technology are already in mass production, with gross margins expected to rise to 50%, though its long-term growth rate can hardly be compared to those of HBM or enterprise-grade SSDs.

Western Digital ( WDC) benefits on both fronts post-spin-off

Western Digital has gained approximately 321% year-to-date in 2026, with a total market capitalization of around $257.2 billion. The company's FY2026 Q2 revenue reached $3.02 billion, up 25% year-on-year, while net profit skyrocketed 209% year-on-year to $1.842 billion. The CEO stated that capacity for 2026 is fully booked, with long-term agreements for 2027 to 2028 already signed with multiple clients. Meanwhile, as a shareholder of SanDisk, Western Digital continues to divest its SanDisk holdings through exchange agreements to facilitate capital repatriation.

How much longer can the supply-demand imbalance persist?

According to Counterpoint data, global NAND market revenue reached $46 billion in Q1 2026, surging 3.5 times year-on-year and already exceeding the full-year total for 2023. Enterprise SSDs accounted for 43% of the market. On the supply side, while demand is projected to grow by 18% annually from 2026 to 2027, wafer starts are expected to contract by 5% in 2026 and increase by only 3% in 2027. This supply tightness is expected to persist until at least 2027.

However, memory chip prices are currently at extreme highs. The spot price of DDR5 16G has soared from around $5.50 in May 2025 to over $40 in May 2026. Any signs of slowing demand growth or capacity recovery could trigger a price correction, thereby sparking sharp volatility in memory stocks. Historically, the peak of a memory supercycle is often when risks accumulate.

SK Hynix Leads the Memory Cycle, but Three Major Risks Warrant Vigilance

Overall, among the seven major memory chipmakers, SK Hynix is in the most favorable position, leveraging its technical and customer advantages in HBM. Samsung possesses the potential for a comeback, but its short-term market share disadvantage remains pronounced. Micron will need to prove itself in the HBM4 era. Kioxia and SanDisk are enjoying peak premiums from the NAND upcycle, but they are poised for the sharpest declines when the cycle turns. Meanwhile, Seagate and Western Digital are benefiting from cold data demand, though their long-term growth prospects are constrained.

Investors should remain vigilant against the following risks: First, memory prices are already at historic highs, and supply-demand dynamics could see marginal shifts at any moment. Second, the HBM4/4E technological roadmap has not yet been fully finalized; any failure in customer qualification would deal a severe blow to the respective companies. Third, current valuations already bake in extremely optimistic expectations, leaving multiple stocks vulnerable to corrections of 30% or more if earnings reports fall short of expectations. The analysis above does not constitute investment advice, and investment decisions should be made in accordance with individual risk tolerance.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.