Tesla in 2025: Brilliance, Bottlenecks, and the Billion-Dollar Question

- Tesla delivered 1.79 million vehicles in 2024, with Q4 cost per vehicle hitting a record low under $35,000.

- Energy revenue jumped 67% YoY to $10.1 billion, fueled by record 31.4 GWh storage deployments and factory expansion.

- Valuation remains steep with a forward P/E of 93x and EV/Sales at 7x, far above sector averages.

- Free cash flow declined 18% to $3.6 billion, while CapEx surged 27% amid major investments in AI and autonomy.

TradingKey - As Tesla (TSLA) ventures deeper into 2025, the electric vehicle (EV) behemoth is caught between two powerful currents—one pulling it forward with promise, and another pulling it back with sobering reality.

The company remains one of the globe's most powerful innovation drivers, not only transforming how we drive but also how we store, produce, and conceptualize energy. And yet for all its pioneering edge and brand value, Tesla's shares are facing new pressure as growth slows, margins contract, and competition ratchets up.

As the broader EV sector ripens and investor expectations shift, Tesla's strategic agility will face its greatest challenge ever. From full self-driving and energy storage to margins and value, the road ahead is anything but smooth. But it's still Tesla—and that means one thing above all: it cannot be ignored.

From Cars to Vision: Full Stretch for Tesla's Business

Tesla's story has long extended well beyond merely making electric cars. At its core, Tesla is a vertically integrated technology group with a focus on building scalable clean energy and AI ecosystems. The company has two main segments—automotive and energy generation/storage—each with important developments happening in 2024.

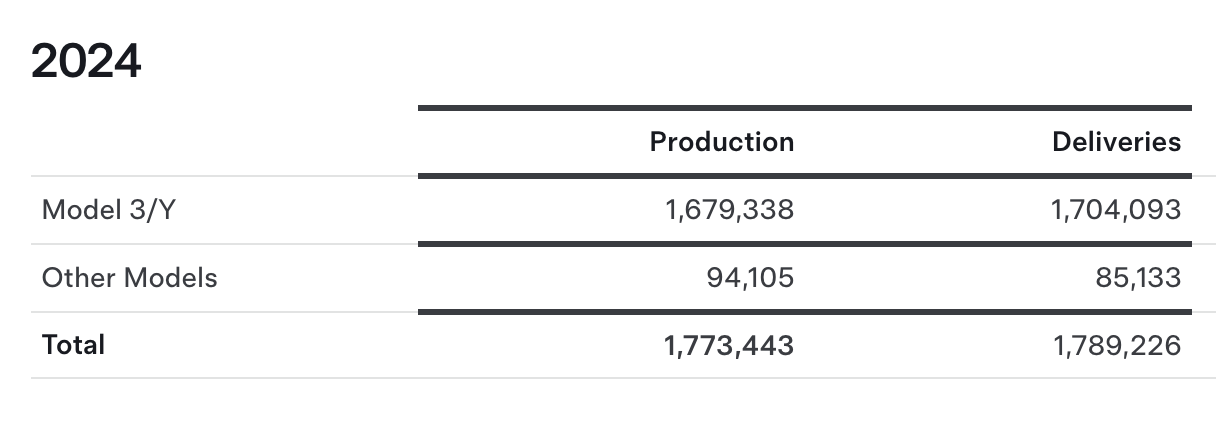

The automotive segment, driven by volume vehicles such as the Model 3 and Model Y, delivered 1.79 million cars in 2024, a modest year-over-year decline, but still enough to maintain Tesla as number one for worldwide EV sales. Model Y, in particular, became the best-selling vehicle of any type on the planet, solidifying its role as a mass-market anchor.

Source: Tesla’s Q4 Release

What makes Tesla unique is its control over technology. From proprietary battery chemistries and car software to chip design and over-the-air updates, the company has a level of control that's obsessive. The result is not product synergy, but margin protection, brand loyalty, and data accumulation.

In 2024, Tesla completed deploying its “Cortex” AI training cluster at Gigafactory Texas, a 50,000 H100 GPU giant fueling its autonomous drive. The FSD (Supervised) platform accumulated more than three billion miles through January 2025, training its neural network with real-world data. Tesla's vision-based autonomy stack is one of the most battle-tested on the road, allowing it to iterate ahead of regulatory ecosystems.

.png)

Source: Tesla’s Q4 Presentation

Its energy business, if less visible, has become a backbone of its diversified growth engine. Energy storage revenue increased 67% to $10.1 billion in 2024. Deployments hit a record 31.4 GWh, driven largely through sales of Powerwall and Megapack. With its Lathrop Megafactory on line and its new Shanghai Megafactory now ramping, Tesla is aggressively entering into grid-scale storage—a business still in its infancy. From car software through solar rooftops and battery deployments, Tesla is consolidating several industries into a single, vertically integrated roof. It's a bold strategy, for sure. It's also one that depends on relentless execution.

Competition Closes In: The Struggle to Stay on Top in a Competitive Market

For most of the past decade, Tesla enjoyed a virtual monopoly on the EV business—owing to its head start, aggressive R&D, and cult-like brand following. All that's evaporating. In each of the major markets—China, Europe, North America—other automakers are not only catching up but, in a few instances, leaping ahead on price, range, and feature innovation. In China, low-cost EVs from BYD are dominating the compact segment. In Europe, VW and Hyundai are closing the gap. Even veteran players Ford and GM have put serious money on electrification and are starting to produce EVs with comparable specs at a lower price point.

Tesla's response has been a steep reduction in average selling prices (ASPs). Between 2023 and through 2024, the company slashed prices on all models across its lineup for volume protection. It achieved unit volumes but at a cost: automotive revenue fell 6% year-over-year at $77.1 billion, and gross margins fell to 17.9%—well below historic highs above 25%. During Q4 alone, nearly 500,000 vehicles were shipped but at less money per unit than ever, with cost per unit falling below $35,000. While a testament to manufacturing efficiency, it also shows price sensitivity on the part of Tesla's core customers.

.png)

Source: Tesla’s Q4 Presentation

Its charging system, once a moat, is also less proprietary as Tesla opens its Supercharger network up for non-Tesla EVs on the North American Charging Standard (NACS). It's consistent with its mission and creates potential licensing revenue, but at the same time, erodes a previously proprietary ownership advantage. AI capabilities are not anymore Tesla's private playground. Nvidia (NVDA), Mobileye, and Waymo are all speeding ahead on autonomous driving—though with varying architectures. Its vision-based system remains unique, but the AI arms race is on.

Even Tesla's cultural cool can wear off. Brand fatigue, poorly thought out words from its CEO, and polarizing rollouts of FSD features into safety-conscious markets have generated headwinds. Simply, Tesla is still the benchmark—but is no longer the only one. And with today's macro backdrop, brand prestige may not be enough to forgive persistent underperformance on margin and volume.

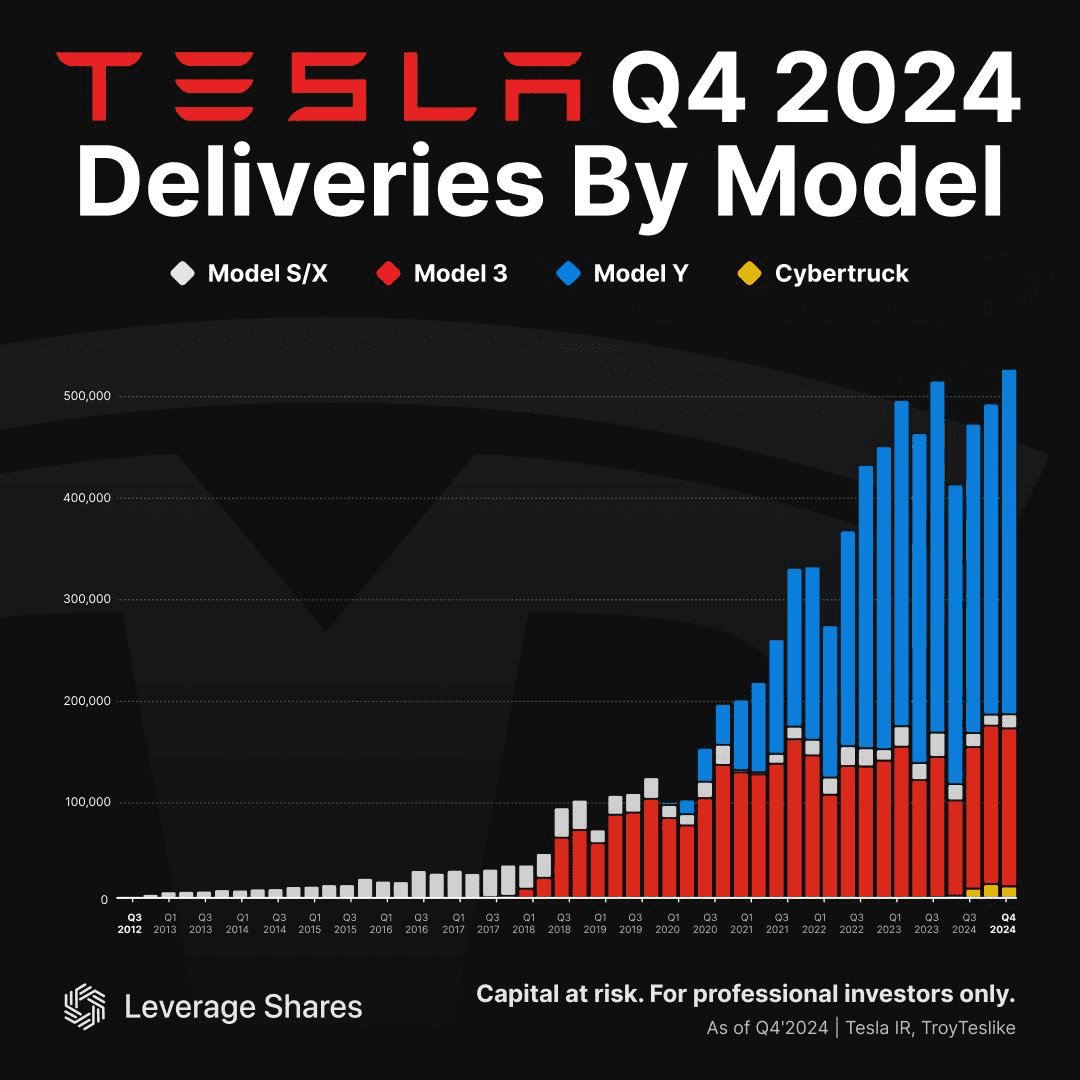

In Q4 2024, the Model Y continued as Tesla's flagship, again leading all vehicles as the top-selling vehicle globally. Deliveries for the Model 3/Y totaled 471,930, and these cars dominated Tesla's quarterly volume, cementing their place at the center of the company's mass-market strategy. The new design and greater affordability of the Model Y worked to sustain demand as competition and economic headwinds rose.

Source: Leverage Shares

In-Depth: Financial Strength, Operating Leverage, and Strategic Mathematics

Tesla's 2024 full-year financials reveal a company in transition. Revenue was flat year-over-year, up just 1% at $97.7 billion, as net income dropped 53% to $7.1 billion. Automotive gross margin tightened, operating income dropped 20%, and free cash flow fell 18% to $3.6 billion. These aren't numbers for a growth technology company—these are numbers for a mature industrial business navigating margin compression and capex-heavy transformation.

However, its balance sheet remains a fortress. With $36.6 billion in cash and investments, Tesla has ample liquidity for its Robotaxi plan, low-cost EV platform, and energy storage ramp. Its operating cash flow reached nearly $15 billion in 2024, a 13% year-over-year increase. Capex was as aggressive, increasing 27% to over $11 billion as production capacity at several gigafactories increased. That investment supports Tesla's long-game: a next-generation car—a low-cost model likely below $30,000—and a scalable Robotaxi network are at its margin story's core.

Operationally, Tesla also leads with automation and vertical integration. The 4680 battery cell, produced in-house, hit production levels over 2,500 Cybertrucks per week, and the Texas lithium refinery processed its first batch of spodumene within 18 months from ground break—a turnaround industry best. These upstream investment costs are designed to secure Tesla's supply chain and stabilize cost profiles, particularly for battery raw materials.

Profitability, however, remains volatile. While adjusted EBITDA stayed at $16.6 billion, adjusted margins dipped below 18%, well short of 2022's high. Cost reductions at Tesla, especially on raw materials and logistics, helped offset some of the damage from falling ASPs, but growing R&D spending on AI, FSD, and robots continues to put a dent in the bottom line. And though FSD keeps improving, monetization is limited. Most customers still pay for it outright or on a monthly subscription basis, but scale adoption is still controlled. The potential upside from a successful Robotaxi launch is huge, but the risk of execution is just as huge.

Valuation on Autopilot: Is Tesla’s Stock Running Too Hot for Its Fundamentals?

Is Tesla worth the expense? Valuations, Premiums, and Hard Realities Tesla's shares continue to trade as a growth technology platform, but its fundamentals are increasingly those of a mature industry. With a non-GAAP P/E at 103x and a forward multiple on EV/Sales at near 7x, Tesla is priced for explosive growth—yet revenue and net income are not increasing at all exponentially.

Compared with sector medians, its value is inflated over 500% on fundamental measures such as P/E, EV/EBITDA, and Price/Cash Flow. To place this into perspective, Tesla's forward P/E at 93x is nearly seven multiples of sector average 14.9x, with a growth curve that is flat. In comparison to its own five-year record, Tesla also appears overvalued. It's now beneath peak multiples but still considerably above its five-year average for many metrics. That shows that the market continues to place an enormous premium on Tesla's future—that is, on FSD monetization, on its energy sector, and on a sub-$30,000 EV launch.

The problem is that those bets remain in the future tense. With a more realistic framework, if one puts a 20–25x forward P/E on 2025 non-GAAP EPS estimates of $3.00–$3.20, a fair value estimate would translate into $60–$80 per share. If one stretches optimism and assumes a $4.00 EPS with margin expansion, the stock may well be worth $100. That's a far cry from where it's currently priced. Even generous DCF models with Robotaxi and AI assume base-case fair values at $120, with today's price at risk of downward repricing if something goes wrong with execution.

Ultimately, Tesla's worth is based on faith—faith that energy, AI, and autonomy will disrupt its business as much as EVs have. At least for now, that faith continues to deserve a premium. Without a tangible earnings reacceleration and actual monetization of high-conviction wagers, however, markets may begin demanding evidence, not potential.

Risk Assessment: Where the Future Meets Friction

Tesla’s forward-looking narrative is powerful, but it comes with equally meaningful risk. Margin compression is front and center—vehicle price cuts aimed at defending volume have weighed on profitability, a trend that could worsen if inflationary pressures persist or if demand softens further amid high interest rates. Tesla’s ability to preserve operating leverage while scaling lower-cost models will be tested throughout 2025.

The autonomy roadmap adds further uncertainty. While FSD (Supervised) has logged billions of miles, full regulatory approval for unsupervised driving remains elusive. If Robotaxi deployment is delayed or fails to deliver material revenue, a core pillar of Tesla’s long-term valuation may weaken significantly. Similarly, its expansion in China—critical to both vehicle and energy growth—exposes Tesla to geopolitical tensions and intensifying local competition, especially from BYD.

Finally, the company's concentrated leadership structure introduces headline risk. Elon Musk’s polarizing persona and commitments outside Tesla could impact strategic focus and investor confidence. In a market that increasingly demands execution over vision, any misstep could drive a rapid reevaluation of Tesla’s premium valuation.

Concluding Thoughts

Tesla remains a market-shaping force, but its stock is priced for perfection while its fundamentals reflect a maturing business under pressure. Unless the company delivers on autonomy, energy, and affordable EVs, valuation multiples may face a sharp reality check. In 2025, belief must start turning into bottom-line performance.