Inside Palantir’s Unstoppable Momentum

- Q4 2024 revenue hit $828M, up 14% QoQ and 36% YoY, driven by explosive U.S. commercial growth and AIP adoption.

- FY 2024 revenue reached $2.87B, with commercial up 43% YoY to $1.29B and government contributing $1.57B (+28% YoY).

- Rule of 40 score climbed to 81% in Q4, with 29% YoY growth and 39% adjusted margins, placing Palantir in elite SaaS territory.

- Valuation remains stretched at 55.25x EV/S and 162.91x P/E, implying little margin for error despite $1.25B in free cash flow.

TradingKey - Palantir Technologies (PLTR) is no longer merely the name that evokes national security and classified government initiatives. Now, it's one of the most visionary, and potentially most controversial, enterprise software and AI players.

Palantir has spent well over two decades cultivating a platform so deeply embedded in the fabric of government and corporate processes that now it's essentially an operating system for decision-making in the modern age. Underlying this process is one clear vision: the union of large language models and enterprise data in real-time so that institutions have the ability to meet complexity with speed, accuracy, and strength.

As AI moves from novelty to inevitability, Palantir has the rare position of being both legacy and upstart. It has the size and credentials of an established defense contractor, but it’s rolling out cutting-edge AI tools faster than most start-ups can push out a beta. From the combat lines of the front to the hospital wards, from the factory floors to the trading floors, its platforms are now integrated into operations that cannot afford to fail.

But there's also scrutiny that goes along with ambition. The market has rewarded Palantir handsomely, perhaps too handsomely. The stock's rocketing rise says less about stellar performance than about fervent belief in a world where Palantir serves as the digital command post for the world's most important institutions. And the answer that investors have today is: Is that belief premature or visionary?

The Business Engine: Platforms for Complexity

To understand the potential—and the hype—behind Palantir, you have to take apart the company's business model. Palantir has built four related software platforms: Gotham, Foundry, Apollo, and the latest flagship, the Artificial Intelligence Platform (AIP). They're not tools. They're modular ecosystems that solve the most complex problems that afflict modern-day organizations, ranging from the logistical problems of the military to supply chain forecasting.

Its nucleus platform, Gotham, remains the foundation for U.S. intelligence and defense agencies' work. It’s used by analysts and operators to process complex datasets—satellite photos, for example, or signals intelligence—and build real-time action plans. Foundry supports commercial businesses by providing a nervous system that connects disparate data assets, automates workflow, and drives analytics into daily operations.

Apollo, the most unsung but arguably most critical piece, manages software deployment into any environment—cloud, on-premise, or even air-gapped military systems. All three combined form a vertically integrated software stack that enables decision-critical operations at scale.

And there's AIP, Palantir's coup. Rolled out mid-2023, it transforms the company's existing platforms into AI-native ones. It makes it possible for enterprises to operate generative AI on their own data—under tight controls, with baked-in human feedback loops, and wrapped in fine-grained access controls.

While most companies bolt on AI onto disjointed processes, AIP weaves it into the fabric. Applications run the gamut: Tampa General Hospital uses it to optimize patient flow and reduce length of stay, Polaris uses it to combat human trafficking, and global manufacturers save millions in months.

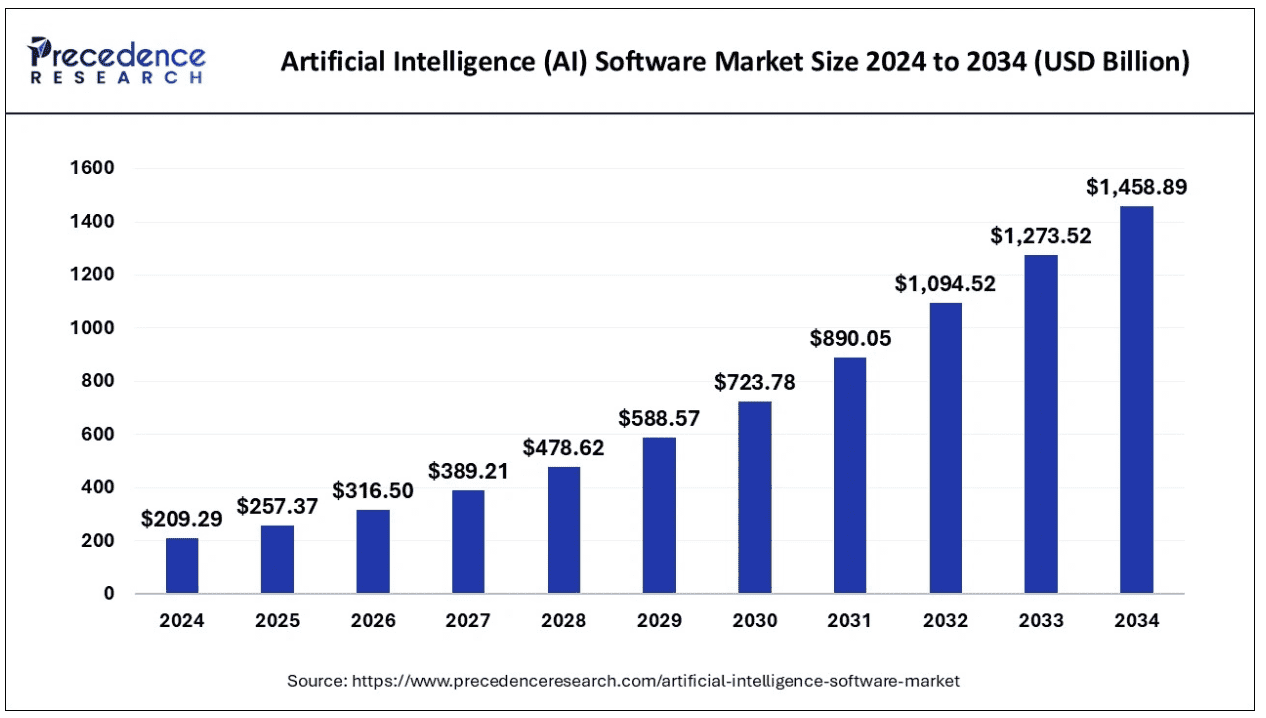

This is not software—it’s governed AI infrastructure, a market which is growing fast yearly. The faster the pace of adoption goes, most prominently in the U.S., the more critical Palantir’s value multiplies.

Source: Precedence Research

The Competitive Environment: Alone, Not Unchallenged

Despite all the uniqueness that it possesses, Palantir does not operate in a vacuum. It faces intense yet fractured competition across all of its platforms. Enterprises attempt internally to stitch together the same capabilities using Snowflake, Databricks, and cloud-native services from AWS, Azure, or Google Cloud. System integrators such as Accenture and Deloitte provide system integration and custom development that can mimic Palantir’s output, albeit at longer timelines and higher implementation risk.

Palantir's value lies in its full-stack mastery and time-to-value. Within one week alone, over 1,000 companies have gone from concept to working prototype on the strength of its AIP Bootcamps. In one case, one Fortune 500 insurance company signed a two-year seven-figure contract just 16 days after the commencement of one of the company's Bootcamps. Enterprise software purchasing processes don't normally occur that rapidly.

However, the competition is changing. Microsoft has added GPT into Azure and Office, effectively bringing generative AI tools within the reach of any enterprise that touches them. Salesforce, SAP, and Oracle are incorporating AI into existing platforms and giving enterprises the familiar interfaces and incremental intelligence. They don’t have the depth that Palantir does in data fusion and operational AI capabilities, but they win on cost, ease, and brand recognition.

But the most pernicious and most formidable competitor is inertia. Palantir’s tools demand cultural transformation. They are not install-and-go. Revolutionary when companywide accepted, they require the endorsement of executives, data analysts, engineers, and line-of-business leaders. To global companies that are loath to replace existing systems, that’s a steep mountain.

Strategic and Financial Depth: Growth and Leverage

What makes Palantir so fascinating is that it combines high growth with mature profitability. Revenue for the year ended 2024 was $2.87 billion, up 29% from the previous year. In Q4 2024, Palantir’s revenue grew 14% quarter-over-quarter, accelerating from $726 million in Q3 to a record $828 million, underscoring the company’s compounding commercial momentum.

.png) Source: Palantir's Shareholder Letter

Source: Palantir's Shareholder Letter

Palantir's revenue tale is rapidly becoming one of two engines—commercial and government—gaining strength on diverging trajectories yet merging into one overarching theme: operational indispensability. Commercial revenue in FY 2024 increased by 29% YoY to reach $1.29 billion and contributed 45% to total revenue. The U.S. commercial segment feels the turning point more keenly, increasing by 54% YoY to $702 million.

That momentum is not merely quantitative—it’s qualitative. Palantir signed a record-breaking $803 million in total commercial contract value in Q4 2024, up by 134% YoY and 170% QoQ. Not only are the deals larger—they're stickier, more strategic, and associated with foundational changes in infrastructure.

.png)

Source: Palantir's 10K

All that notwithstanding, the government vertical continues to provide the overall top line's anchor, contributing $1.57 billion in revenue (55% of total) in 2024, up by 28% YoY. Commercial has become the growth driver now, yet the government remains the margin driver. Palantir’s roots in intelligence, defense, and federal services have built deep institutional trust—and high-margin, multi-year contracts with highly defendable renewal.

The company’s Q4 FedRAMP High authorization and renewal by Army Vantage for up to four years suggest government revenue will remain strong, if incrementally growing less than commercial. That duality provides Palantir unusual resilience: recurring government base and high-growth commercial rocket.

Long-term agreements between intelligence and defense agencies like the new $480 million contract between the Department of Defense's CDAO reaffirm Palantir's position as a foundational national security provider. These agreements are large-scale, multi-year, and highly embedded—demonstrating stability, transparency, and high switching barriers that shield Palantir from typical SaaS churn.

As the deal cycles shorten—some closing in less than 30 days—and the value of the remaining deals more than doubled year-over-year, the commercial segment now provides exponential upside. If the trend holds, it's plausible that the revenue mix at Palantir will become dominated by commercial within the next 12–18 months, marking the fundamental shift in the company's long-term growth story.

Its customer base goes even deeper, with average revenue among the company's top 20 clients at $64.6 million, up by 18% year-over-year. Palantir's ability to capture multi-million-dollar contracts and then expand within accounts—typically within entire industries—speaks to the product's stickiness and vertical nature. Within the industries of energy, insurance, and aerospace, Palantir is becoming operational DNA.

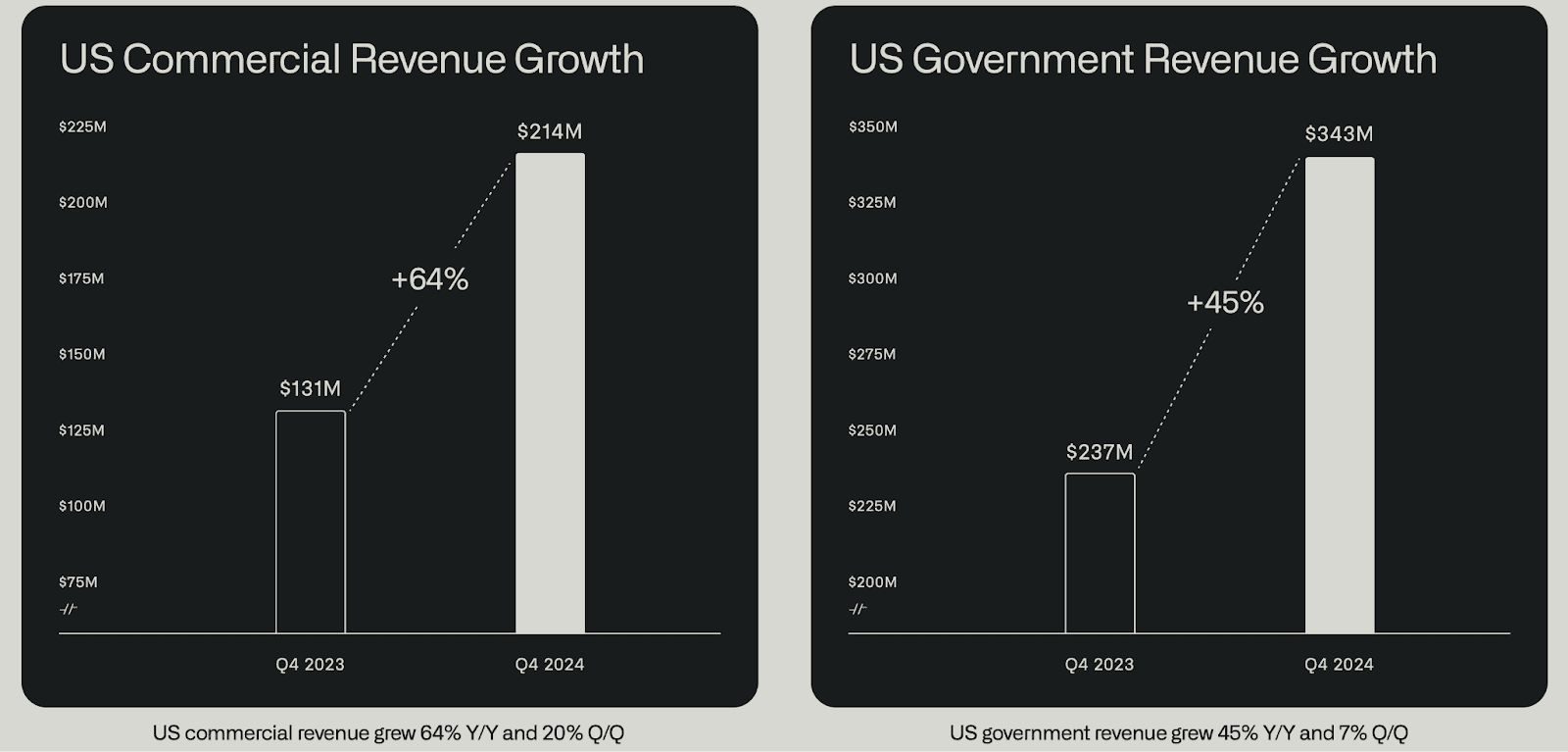

U.S. commercial revenue in Q4 2024 increased by 20% QoQ to $214 million on the strength of takeup of the AIP and growing enterprise penetration. U.S. government revenue grew by 7% QoQ to $343 million, continuing steady growth at a slower pace than the commercial driver.

Source: Palantir’s Q4 Earnings

Finally, the company has also been criticized for the practice of using stock-based compensation (SBC), most significantly in the form of SARs (Stock Appreciation Rights). Net income according to GAAP for the year came in at $462 million, but adding SBC brings that figure up to $1 billion. The company has committed to better capital allocation in the years ahead, but investors will keep a close eye on measures for dilution.

Valuation: Stretched by Any Measure

Against the backdrop of Palantir’s operational strength, the valuation of the stock is extreme by any conventional measure. At 55.25x forward EV/Sales and 162.91x forward Non-GAAP P/E as of March 21, 2025, the multiples are more than 1,900% and 650% higher than the medians in the sector. Even allowing for long-term margin expansion, these figures imply expectations bordering on perfection.

Relative to peers, Palantir's valuation is well above high growth SaaS stocks such as CrowdStrike (~18x EV/S) or Snowflake (~22x). Even Nvidia—a beneficiary of the generational tailwinds around AI—has a lower forward P/E.

A discounted cash flow calculation using 30% CAGR by 2029, 35% long-term FCF margins, and a 10% discount rate puts the fair value in the $62–$74 range—way less than the current level. To support $90+, bulls would require Palantir to offer not only growth acceleration in revenues but also steady 40%+ margins, leadership in the sector, and geopolitical tailwinds.

By the Rule of 40 measure, however, Palantir excels. At 39% adjusted operating margin and 29% YoY growth in FY 2024, the company’s overall score of 68% places it firmly among the elite. That score reached 81% in Q4. These figures mean the company not only growing—growing efficiently. Below-50% scores are typical for most high-multiple SaaS stocks, so Palantir’s premium is partially vindicated—though certainly still excessive.

.png)

Source: Palantir's Q4 Earnings

However, the bear case is just as clear: if the trend in AI goes towards open-source commoditization or Palantir's pricing strategy meets resistance, the current valuation cannot hold.

Risks and Red Flags: Not Without Shadows

Though the story is tempting, investors cannot overlook critical threats. Customer concentration remains high, with the three largest clients accounting for 17% of revenues. Many government contracts include early termination clauses, and the company's reliance on U.S. defense spending exposes it to political instability.

International growth remains a work in progress. While U.S. revenue picked up pace, non-U.S. revenue growth has stalled. That divergence might become troublesome, especially in the light of growing geopolitical scrutiny surrounding data and AI.

The complexity of the Palantir platform also serves as a two-edged sword. Adoption processes are intensive and require high levels of upfront training, integration, and cultural adoption. Organizations that have matured on SaaS simplicity might find Palantir overwhelming—and expensive.

Finally, the accelerated development pace in generative AI also introduces another type of risk: commoditization. If the companies switch to in-house LLMs or open-source alternatives, Palantir’s pricing power will dissipate. Its competitiveness arises from deployment and integration, yet these barriers are viable only if the clients view them as irreplaceable.

Conclusion: Bet on Intelligence Infrastructure Boldly

Palantir is building what few companies even attempt—an AI-native operating system for the real world. It's expanding for real, has great margins, and has the most favorable strategic positioning. Already the stock market has priced in years of flawless execution. It very well may become the control layer of the companies of the 21st century, yet even the slightest misstep would bring the valuation down to reality. Investors who are betting on Palantir are not just betting on the company, they're betting on the paradigm.