Meta’s Big Bet on the Future

- Meta delivered Q4 2024 revenue of $48.39B (+21% YoY) and net income of $20.84B (+49%) on strong ad performance.

- Free cash flow reached $52.1B in 2024, supporting aggressive $60–65B CapEx plans for AI and infrastructure expansion in 2025.

- Meta AI targets over 1B users as Llama 4 and smart glasses push the company deeper into open-source and ambient computing.

- Trading at 23.2x forward earnings, Meta commands a rich premium, raising stakes amid rising CapEx and competitive AI pressure.

TradingKey - Meta Platforms closed 2024 with a solid set of financials that asserted its leadership in the digital ad ecosystem while accelerating its long-term game in AI and next-gen computing platforms. With revenue rising 21% year-on-year to $48.39 billion in Q4 and net income rising by 49% to $20.84 billion, it was able to drive profitability while aggressively investing in AI and infrastructure. Valuation remains a key consideration, with sector comparisons indicating that Meta trades at a meaningful premium to industry averages, reflecting investor confidence in its growth prospects. This raises crucial questions for investors on whether these higher multiples are sustainable, given CapEx estimated to reach $60-65 billion in 2025 to fund AI-related infrastructure.

Meta’s business strategy is increasingly directed towards its AI ecosystem that includes consumer-facing AI assistants, open-source large language models, and AI-powered advertising optimization. Meta AI has been set by Mark Zuckerberg as the world’s best personal assistant with plans to grow to serve more than a billion users. Meta’s Llama 4 model to be rolled out in 2025 is intended to beat others and assert Meta’s leadership in open-source AI.

However, whether this is sustainable is questionable with competitors like OpenAI and Google (GOOG) investing heavily in proprietary AI models. Whether there are significant revenue gains to be made through an open-source strategy is debatable. In the meantime, Meta is still developing AI-powered consumer hardware, including its Ray-Ban Meta smart glasses that it believes will be the future’s big computing platform. AI-powered wearables’ adoption trend is still unclear and Meta’s hardware experience—most notably in Reality Labs—suggests that profitability in this sector will be a long-term impediment.

The Competitive Landscape: AI Disruption to Confront Monetization Power

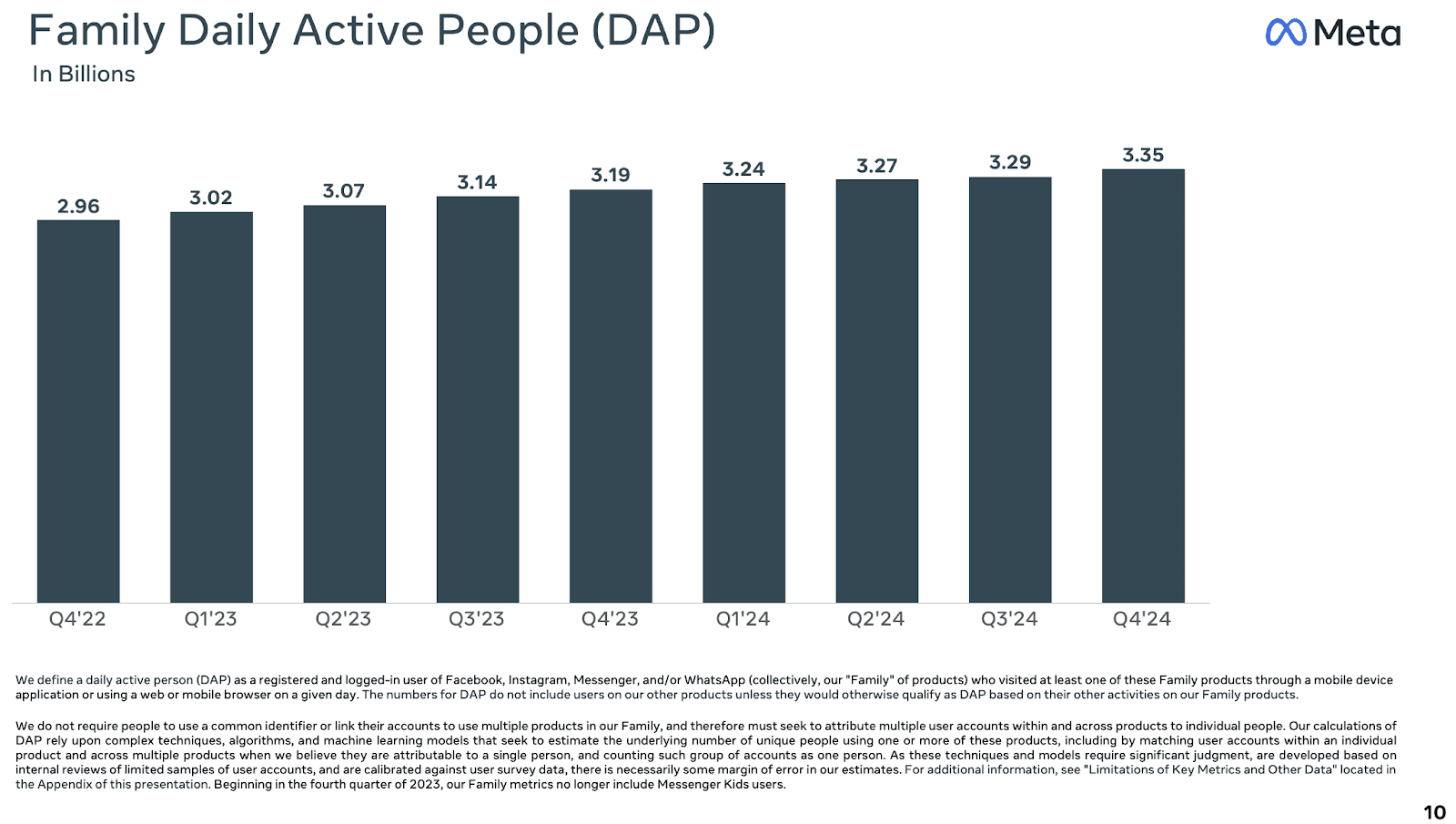

Meta’s advertising business maintains strong growth with Q4 advertising revenue of $46.8 billion, up by 21% on last year. Leadership in social engagement is still unmatched with 3.3 billion daily active users across its Family of Apps including Facebook, Instagram, WhatsApp, and Messenger. Ongoing market share dominance by Instagram Reels has been particularly impressive with engagement and monetization trends continuing to improve. WhatsApp Business, a fresh growth driver, grew revenue by 55% year-on-year as messaging and commerce features saw increased adoption.

Source: Meta’s Q4 Earnings Presentation

In parallel, Threads, Meta’s X (previously Twitter)-rival has reached more than 320 million monthly active users, testifying to the company’s ability to grow new platforms rapidly. However, monetization potential on Threads is still in infancy with Meta just starting to introduce ads in 2025. Gradual monetization strategy for this platform means that it may not be a material revenue contributor until 2026 or later.

While Meta leads the digital advertising market, its AI strategy places it in direct competition with some of the strongest incumbent players in the tech sector. OpenAI still has a leadership position in enterprise AI use cases with ChatGPT gaining support among business and developer communities. Meta’s open-source response, open-source Llama model series, is designed to drive widespread adoption and reduce dependence on closed systems.

However, OpenAI’s monetization of models through API integrations and enterprise partnerships challenges whether Meta’s open-source strategy will generate similar economics. DeepSeek, a rapidly emerging Chinese competitor, has made things more difficult by producing AI models that compete with Western incumbents for a fraction of the cost. If DeepSeek’s cost savings are sustainable, they would drive margin compression for AI-powered services across the sector. Google’s DeepMind and Anthropic are also building on next-generation AI systems with increasing competitive pressure.

Other than AI, Meta’s Reality Labs business is still a drain on finances. While revenue for the business grew modestly to $1.1 billion in Q4, it still saw a staggering $5.0 billion operating loss. Despite investing for decades, Meta has yet to prove that virtual and augmented reality can deliver profitable expansion on a large scale. Zuckerberg is still hoping that AI-powered smart glasses will drive mass adoption, but previous attempts in the metaverse show that mass adoption may take longer to happen than anticipated. Meta’s strategic conundrum is to balance its AI and hardware ambitions with continued need to maximize its core advertising business that still brings in more than 97% of revenue.

.png)

Source: Meta’s Q4 Earnings Release

Financial and Strategic Analysis: The Cost of Expansion

Meta’s 2024 financial report offered a compelling blend of revenue expansion, margin improvement, and disciplined operating execution—a remarkable feat given a heavily investment-heavy transition to computing infrastructure and AI.

Revenue for the year was $164.5 billion, up 22% on 2023, with Q4 revenue of more than $48.39 billion. Fueling that was advertising strength across Meta’s platforms, particularly on Instagram Reels, WhatsApp Business, and emerging monetization surfaces like Threads. More impressive than top-line growth was the increase in profitability metrics that showed the operating leverage in Meta’s platform business.

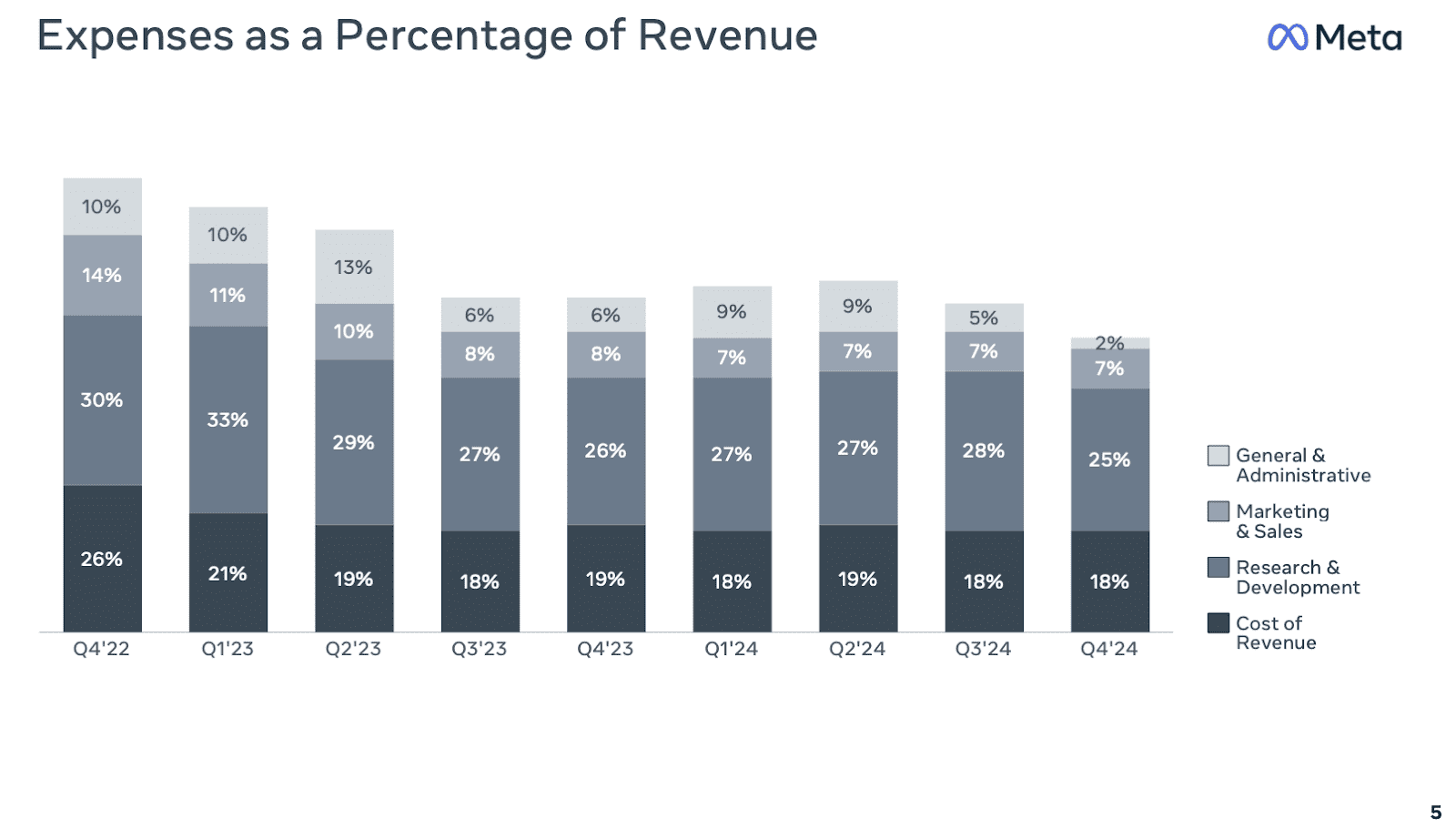

Operating income for Q4 was $23.36 billion with an operating margin of 48%—a big improvement on last year’s 41%. Similarly, Meta’s operating margin for the twelve months was 42%, a big improvement on 35% in 2023. These improvements were achieved despite increased expenditure on R&D, infrastructure costs, and continuing operating losses in Reality Labs with a $5.0 billion quarterly loss. Cost control elsewhere, particularly on legal and administrative lines, also helped to drive up profitability. General and administrative costs fell heavily in Q4 due to a positive $1.55 billion legal accrual reversal that also helped to keep total expense growth moderate at 5% on a twelve-month-on-twelve-month basis.

Source: Meta’s Q4 Earnings Presentation

One of Meta’s best demonstrations of financial health is free cash flow generation. It produced $52.1 billion of free cash flow for the full year and $13.15 billion in Q4 alone. That level of internal cash generation makes Meta not only able to self-fund its enormous capital expenditure plans but also able to fund shareholder returns through buybacks and dividends. Of particular note is that Meta closed out 2024 with $77.8 billion of cash, cash equivalents, and marketable securities and only $28.8 billion of long-term debt—a very strong net cash position. That liquidity cushion gives Meta strategic room and downside protection, especially as the AI infrastructure arms race picks up speed across the tech sector.

All that notwithstanding, the path forward will entail navigating a steep rise in capital intensity. Capital expenditure was $39.2 billion in 2024 and will rise higher still, with Meta guiding to $60–65 billion in 2025. These are for AI compute, data center buildout, and customized silicon development—all necessary to enable the scaling of Llama models, Meta AI deployment, and advanced ad personalization infrastructure.

Although management is anticipating long-term revenue leverage on these investments, they do put pressure on near-term returns on invested capital. The durability of Meta’s operating margin will thus depend on whether it can optimize AI workloads in efficient and effective forms and avoid overbuilding ahead of monetization.

.png)

Source: Meta’s Q4 Earnings Presentation

At the segment level, Family of Apps remains the company’s economic engine. The segment reported a staggering $28.3 billion of Q4 operating income on a 60% margin—a reflection of the health of Meta’s core advertising business. Reality Labs is a stark contrast and remains a big drag with $6.0 billion of Q4 costs and only $1.1 billion of revenue. Management still characterizes these losses as long-duration investments, but financially Reality Labs remains dilutive to operating margins and earnings per share.

Valuation Gravity: Can Meta’s Premium Hold Amid Rising Expectations?

From a valuation perspective, Meta’s premium to peers is a test for shareholders. With a forward multiple of 23.2x earnings, the company is priced at a significant premium to sector-median of 17.4x. EV-to-sales, a metric to consider for growth stocks, is 7.7x, nearly four times sector-average.

Leadership in digital advertising and AI innovation may warrant a premium, but it also subjects the company to multiple compression in case revenue growth slows or AI investment fails to generate projected returns. The company’s dividend yield remains low at 0.35%, compared to sector-median of 3.65%, implying that Meta is still more focused on reinvesting profits than returning capital to shareholders. On first glance, this premium multiple would seem to be unsustainable, particularly in a market that is increasingly finicky about capital efficiency. That said, Meta’s leadership position in both digital advertising and underlying AI infrastructure lends this premium credibility. It’s not just a participant in secular growth trends—Meta is shaping them.

The question for shareholders is whether this reinvestment-heavy strategy will deliver returns that not only sustain, but grow, Meta’s current premium. If it can maintain its leadership in AI monetization and deliver on its infrastructure with operating efficiency, existing valuation multiples can readily prove to be conservative.

For long-term patient investors who can stomach some volatility, Meta offers exposure to some of the decade’s most important tech inflections—ranging across social commerce and personalized advertising to open-source AI and ambient computing. While the path might not be linear, the story for the upside remains intact—backed by a fortress balance sheet, strong free cash flow, and a track record of navigating structural changes.

Concluding Thoughts

Meta Platforms remains a giant in digital advertising and a key player in rapidly evolving AI. Its capital resources, technological leadership, and vast user base provide a strong platform for future expansion. Its entry into AI-based advertising, smart assistants, and open-source language models has potential to drive long-term expansion, and expanding into integrating AI with hardware is part of a greater vision for future computing. That being said, there are risks to watch in its capital-intensive AI strategy, competitive pressures in the AI market, and stretched valuation on the stock.

Meta’s fundamentals remain robust while the elevated multiples of the company’s stock suggest that a significant portion of future growth is priced in. Any miss on AI execution, regulation changes, or ad market dynamics can cause a valuation reset. With all that heavy investment in AI infrastructure and uncertainty around AI monetization, there are better points for investors to enter on a downturn in the market. For those with a long-term investment horizon and conviction in Meta’s AI vision, the company’s stock is still a good bet on digital transformation.