[IN-DEPTH ANALYSIS] Snowflake: Leading the Charge in Cloud Data Innovation

Key Takeaways

- Data Cloud Leadership: Snowflake’s cloud data platform outpaces competitors with its scalable, cross-cloud architecture and cost-efficient storage-compute separation, setting a new industry standard.

- AI Leadership Potential: Cortex AI and Snowpark help NRR at 126%, positioning Snowflake as an AI/ML frontrunner.

- Investment Outlook: A target price of $162 -$182, making it a profitable investment if AI and operational goals are met.

TradingKey-Imagine a world where data flows seamlessly across clouds, scales effortlessly to meet demand, and powers AI-driven insights without breaking the bank. That’s the promise of Snowflake Inc. (SNOW), a trailblazer in the cloud data platform space. Launched in 2012 and publicly listed in 2020, Snowflake has redefined how enterprises manage and extract value from their data. Its flagship offering—a fully managed cloud data warehouse—separates storage from compute, delivering elastic scalability, cross-cloud compatibility, and a robust ecosystem for analytics, data sharing, and AI.

What Does Snowflake Do?

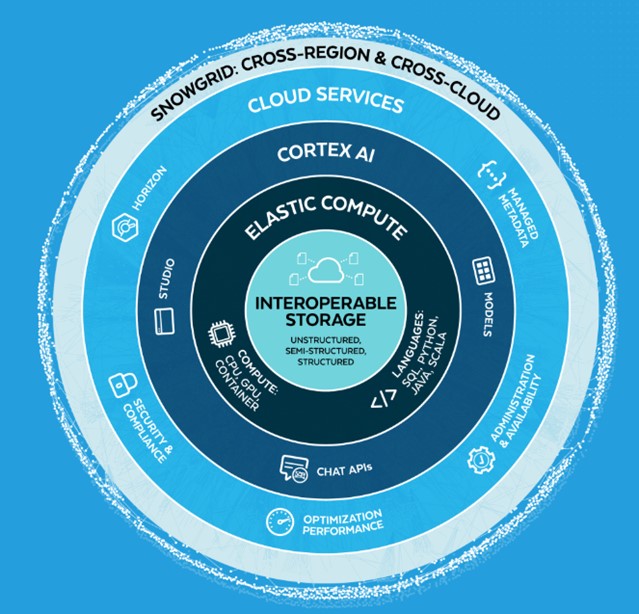

Source: Snowflake

Snowflake is a cloud-native SaaS leader that empowers organizations to store, process, and analyze massive datasets—structured, semi-structured, and unstructured—without the headaches of traditional data management. Its core product is a cloud data warehouse that runs on AWS, Azure, and Google Cloud, offering:

- Optimized Storage: Snowflake provides near-infinite scalability for structured, semi-structured, and unstructured data, leveraging cost-efficient cloud object storage. Its automated data compression and secure management eliminate silos, enabling seamless access to all data in one place.

- Elastic Compute: A single, flexible engine supports diverse workloads such as analytics, streaming, AI, and applications. It includes GPU options for performance-intensive tasks and ensures fast, reliable performance without tuning or contention, even under heavy concurrency.

- Data Sharing: The Snowflake Data Marketplace facilitates secure, real-time collaboration between enterprises. Organizations can instantly share and access data globally without needing ETL processes, enabling seamless cross-cloud and cross-region data exchange.

- AI Innovation (Cortex): Snowflake’s Cortex AI offers serverless large language models (LLMs) like Anthropic Claude and Llama 3 for natural language processing, data summarization, and predictive analytics. It also provides conversational interfaces to make insights more accessible to business users. Cortex AI has received positive feedback for its ease of use and efficiency in enhancing business processes, but users have also noted limitations in customization options and support, which can impact its effectiveness for advanced users. It is reported 750 customers (Snowflake owns 11000+ customers totally) are using Cortex AI, so the impact is minimal for now.

- Developer-Friendly Tools (Snowpark): Snowpark supports popular languages like SQL, Python, and Java, allowing developers to build data engineering and machine learning workflows easily. It integrates with native or third-party tools, enabling efficient development without moving data.

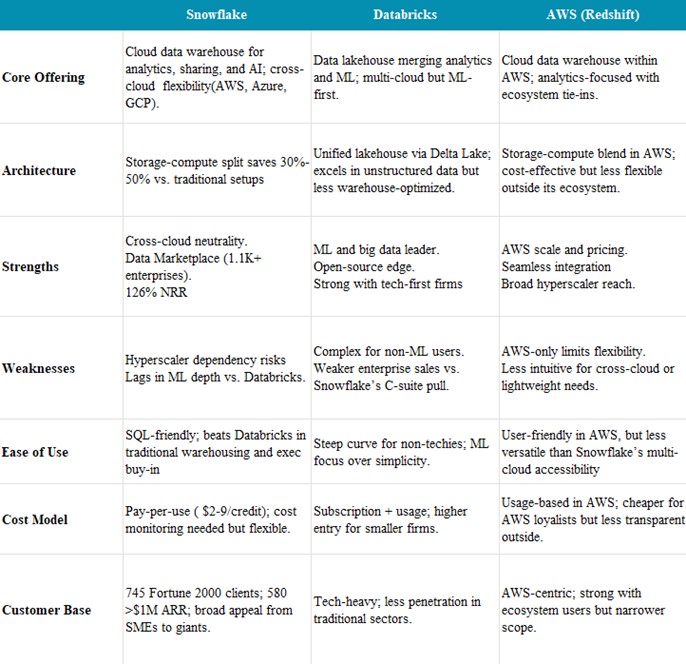

Competitive Landscape

Snowflake shines in a crowded field, but it’s not without flaws. Snowflake’s blend of scalability, ease, and cross-cloud neutrality creates a sticky platform. Its rare talent for charming big company executives with sharp cost-saving and data-driven pitches sets it apart. The Data Marketplace amplifies this, turning data into a collaborative asset. Yet, hyperscaler dependency and cost management remain critical weaknesses.

Here’s how it compares against key rivals— Databricks (ML-driven lakehouse) and AWS (hyperscaler titan):

Source: Tradingkey.com

Strategic Deep Dive

Competing with Cloud Providers

Snowflake’s reliance on AWS, Azure, and Google Cloud for infrastructure presents a unique challenge. These hyperscalers possess significant capital and resources, allowing them to aggressively promote their own solutions, such as AWS Redshift and Google BigQuery, as cost-effective alternatives. However, Snowflake’s key differentiator lies in its cross-cloud neutrality, enabling it to operate seamlessly across all three major cloud providers. This neutrality addresses enterprise concerns about vendor lock-in, a value proposition hyperscalers are unable to replicate.

Recent results indicate that Snowflake’s collaboration with hyperscalers is yielding positive outcomes, with partnerships driving incremental sales leverage rather than fostering direct competition. That said, Snowflake’s rising compute costs remain a headwind, putting pressure on margins. To sustain its market position, Snowflake must continue to innovate and leverage its storage-compute separation architecture to maintain its cost advantage.

Strengthening AI/ML Customer Relationships

The rapid growth of AI/ML workloads represents a significant opportunity for Snowflake. Its elastic compute engine, Cortex AI, and managed service model are well-suited to address this demand. The pay-as-you-go pricing model reduces adoption barriers for small and medium-sized enterprises, while enterprise-grade features like serverless large language models (LLMs) and Snowpark’s Python/Java integration attract larger organizations building sophisticated AI pipelines.

Notably, growing traction in Cortex AI and Snowpark workloads, which helped stabilize Snowflake’s net revenue retention (NRR), following a ten-quarter decline. Snowflake’s intuitive platform and enterprise-focused sales strategy also give it a significant edge over competitors like Databricks, which is often seen as more complex and developer-centric.

Expanding the Data Marketplace’s Role

Snowflake’s Data Marketplace is a pioneering platform for secure and compliant live data sharing. Tools like Snowgrid (for cross-cloud collaboration) and Horizon Catalog (for governance) make it easier for organizations to share data seamlessly across businesses and clouds. However, the Marketplace’s current focus is predominantly on analytics use cases, such as sharing datasets for insights or reports. It lacks the capabilities to support operational workflows, where data is used in real-time to drive business decisions—an area where competitors like Palantir excel.

To become the leading live-data ecosystem, Snowflake must expand the Data Marketplace’s functionality beyond analytics into real-time decision-making workflows, where shared data can actively influence business processes (supply chain optimization or fraud detection). While hyperscalers (AWS or Google Cloud) may attempt to replicate this offering, Snowflake’s first-mover advantage and large customer base give it a strong foundation to maintain its lead.

Financials: From Post-IPO Turbulence to Steady Resilience

Post-IPO Decline

Snowflake’s stock plummeted post-IPO due to market shifts and internal challenges, but these factors have largely eased, signaling a sustainable recovery driven by operational improvements.

Source: Tradingview

Snowflake soared to $429 in December 2020 after its $120 IPO, only to crash 75% to $110 by late 2022. The drop stemmed from two forces: a macro-driven SaaS sell-off and company-specific stumbles. Rising interest rates crushed high-valuation growth stocks—Snowflake’s 60x forward sales became untenable. Meanwhile, revenue growth slowed (174% FY2021 to 69% FY2023), NRR fell (168% to 151%), and negative profit margins fueled doubts as customers optimized spending. Now we examine whether things have improved by Q4 FY2025:

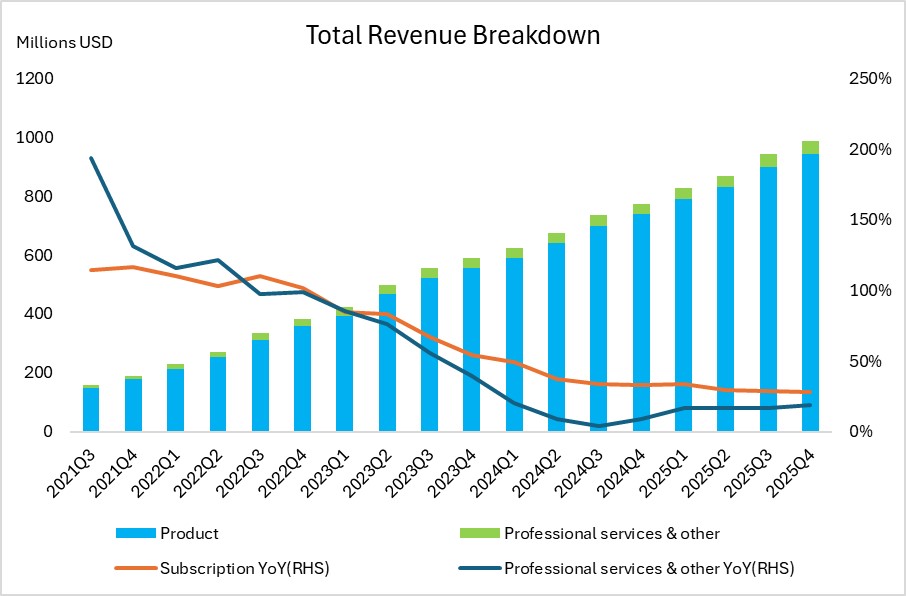

- Revenue: Revenue splits heavily toward the cloud data platform at 96%, with just 4% from professional services like training and support. While product revenue’s YoY growth has slowed over the past four years, raising concerns about potential market saturation or tougher comparisons. However, management counters this by spotlighting the Data Marketplace as a key growth engine, driving higher consumption as customers increasingly rely on shared datasets to power analytics workloads.

Source: Company Financials, Tradingkey.com

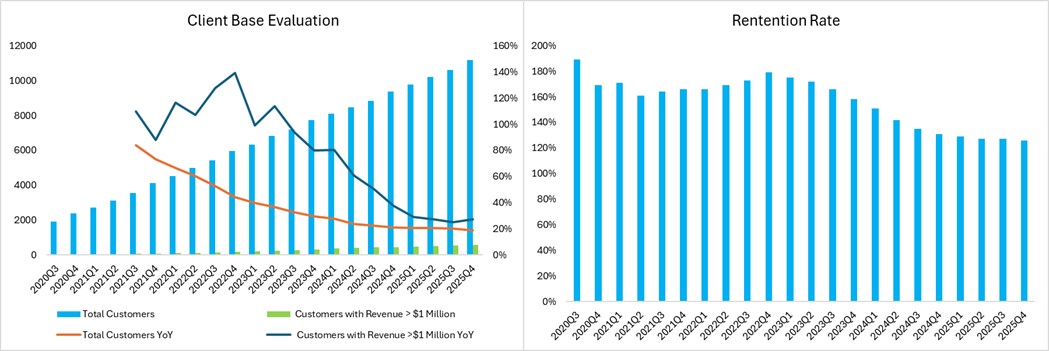

- Customer Adoption: over 11,000 customers across finance, healthcare, and retail, proving its broad appeal. The number of customers spending over $1 million annually rebounded. However, net revenue retention (NRR) slid from 170% in FY2023 to 126% in FY2025, likely due to cost-conscious customers optimizing usage and competitive pressures from Databricks and hyperscalers. This dip, while cushioned by growing customer numbers, signals a modest setback as slower expansion dims the growth story, even as reliance on shared datasets keeps churn low.

Source: Company Financials, Tradingkey.com

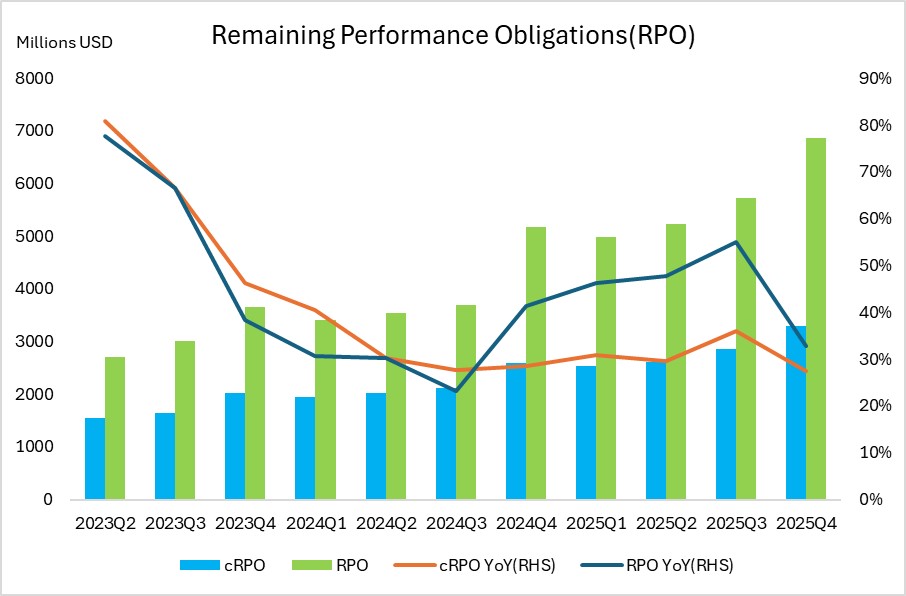

- cRPO: The significant YoY drop in cRPO and RPO in Q4 FY2025, reversing a two-year upward trend, suggests shorter customer contracts or weaker upselling, reducing Snowflake’s near-term revenue visibility. This could strain its ability to fund AI initiatives, requiring a closer look at spending trends in future quarters.

Source: Company Financials, Tradingkey.com

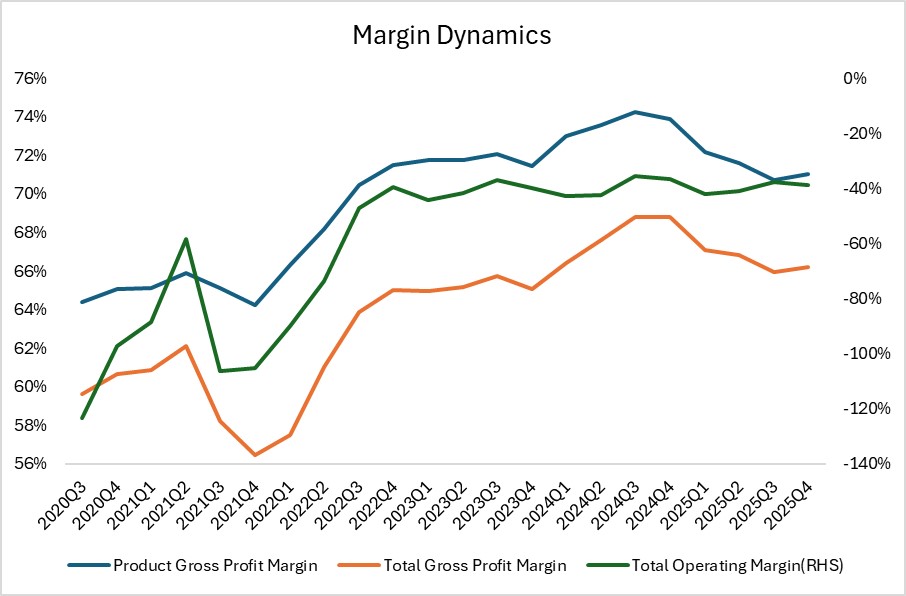

- Margins Evolvement: Profitability is trending upward, with Product Gross Profit and Total Gross Profit margins climbing since FY2022 as Snowflake successfully reduced expenses, though a slight dip in FY2025 reflects heavier investments in AI and security; the Operating margin mirrors this rise but stays negative, while cutting low-value garbage projects and scaling back equity grants have further lifted margins.

Source: Company Financials, Tradingkey.com

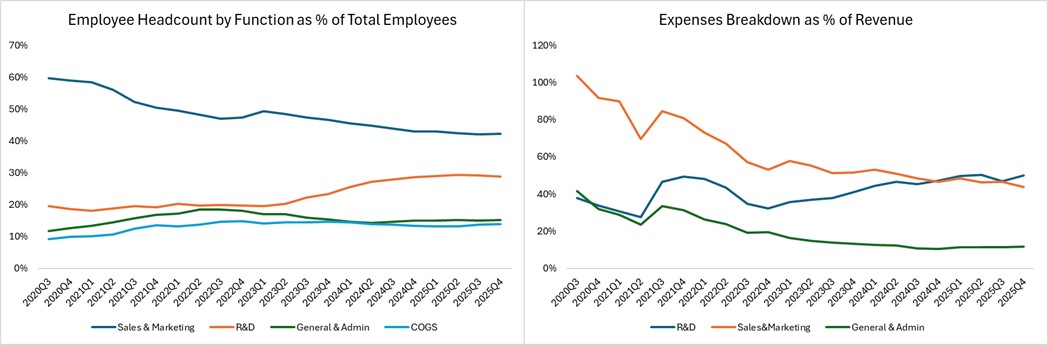

- Expenses Distribution: Since FY2023, Snowflake’s employee and expense trends show a clear shift: Research & Development headcount and costs are rising, while Sales & Marketing and General & Administrative expenses are declining. This focus on R&D over sales and overhead is a positive signal, as it channels resources into product innovation, enhancing competitive differentiation and customer retention, while efficiency gains reduce reliance on costly sales tactics, paving the way for sustainable future growth.

Source: Company Financials, Tradingkey.com

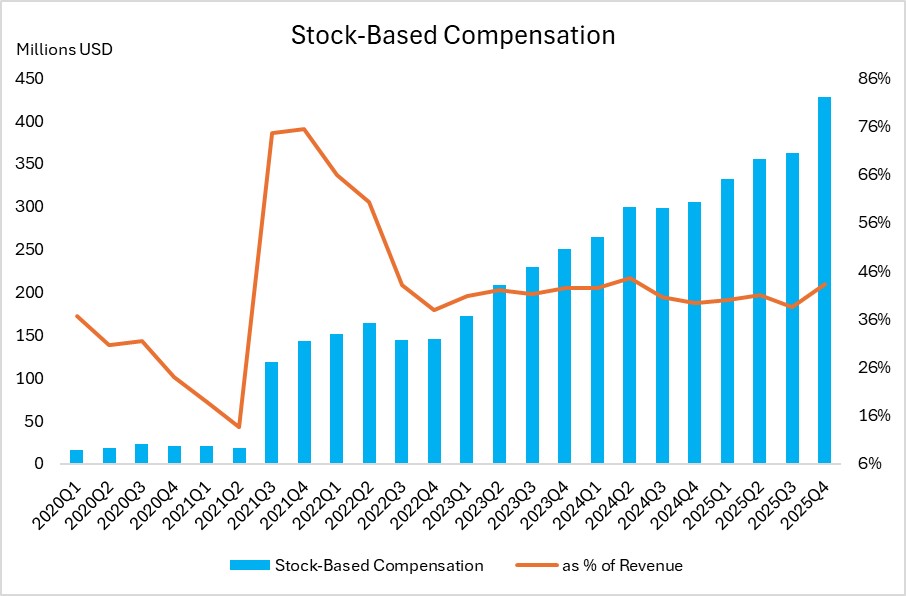

Stock-based compensation (SBC): SBC is vital for high-tech companies like Snowflake to attract top talent and conserve cash for innovation. SBC doped from peak of 75% of revenue indicates a more disciplined equity allocation post-IPO, and trended steadily at around 40% afterwards, while there is a surge in Q4 FY2025. This jump probably stemmed from AI-focused hiring, retention amid rival pressure, and a rebounding stock price boosting grant values.

Source: Company Financials, Tradingkey.com

Valuation

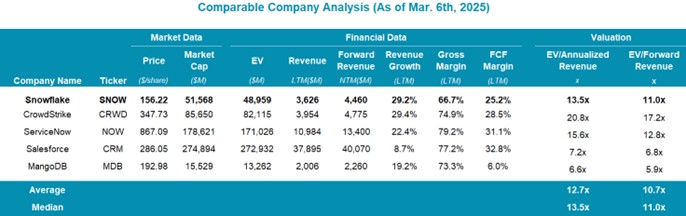

We value Snowflake using the EV/Forward Revenue multiple, a forward-looking metric ideal for high-growth SaaS companies, as it reflects market expectations for the next twelve months’ revenue, capturing near-term growth potential. With Snowflake’s forward revenue at $4,460M and an enterprise value of $48,959M, its current EV/Forward Revenue multiple is 11.0x. This is benchmarked against peers, with a median of 11.0x. Snowflake’s 29.2% revenue growth, surpassing peers like Salesforce (8.7%) and MongoDB (19.2%), supports a premium multiple. We apply a target range of 11.5x-13.0x, aligning with ServiceNow’s 12.8x while reflecting Snowflake’s growth leadership.

Using $4,460M, target EV ranges from $51,290M (11.5x) to $57,980M (13.0x). With forecast net cash of $2,508M, equity value spans $53,798M to $60,488M, yielding a target price range of $162-$182 per share.

Source: Company Financials, Tradingkey.com

Conclusion

Snowflake stands as a leader in the cloud data platform space, with its Data Marketplace and cross-cloud capabilities driving 24-30% annual revenue growth through FY2026. Despite a competitive landscape featuring Palantir, hyperscalers, and Databricks, Snowflake’s focus on AI innovation (Cortex, Snowpark) and operational expansion positions it for long-term success, though execution risks remain. It is an attractive company for investors confident in its AI and real-time workflow advancements.