[IN-DEPTH ANALYSIS] Apple’s Path Forward: Balancing Innovation, Pricing, and Market Challenges

Key Takeaways:

- iPhone Dominates but Faces Pressure: Apple’s iPhone remains its revenue cornerstone, but declining sales raises concerns due to competition and lack of major design updates.

- Smart Home and AI: New ventures like smart home devices and Apple Intelligence offer growth opportunities, but high pricing and delayed adoption limit near-term impact.

- Stock Valuation and Risks: Apple’s current stock price reflects market optimism, but risks in China and AI development may limit its fair value to a range of $167–$264.

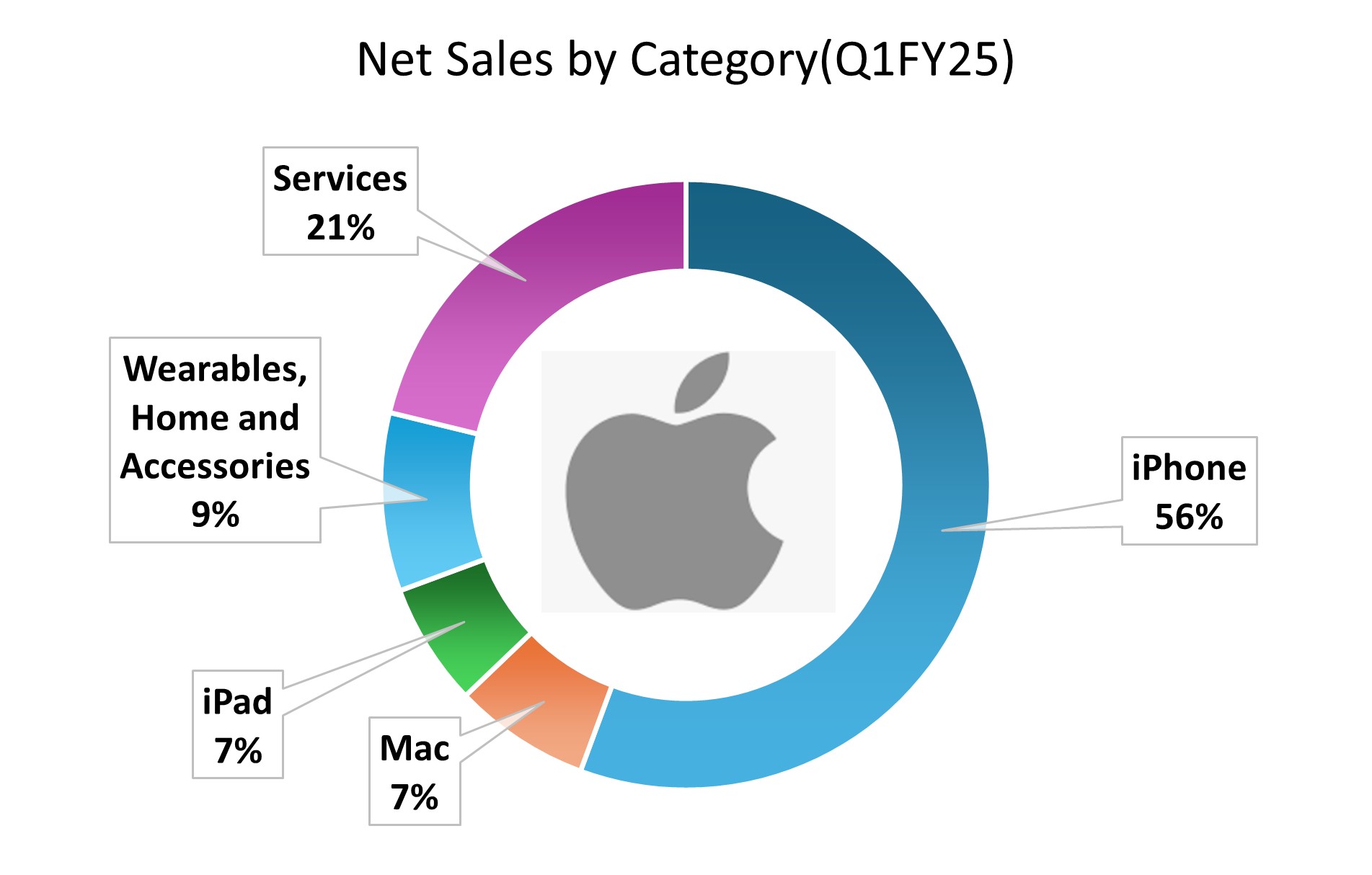

Apple's success depends on creating new and innovative products, with updates to both hardware and software helping the company grow—hardware being the most important part. However, Apple hasn’t made major design changes in years, which could make consumers lose interest. At the same time, its high prices are facing resistance in competitive markets. Even though the iPhone makes up 50% of Apple’s total revenue, the company is expanding into smart home devices and artificial intelligence (AI) to keep growing despite these challenges.

Source: Company Financials, Tradingkey.com

Smart Home Ecosystem: Strategic Expansion with Pricing Challenges

Apple is expanding its product line with smart home devices, aiming to make the most of its ecosystem, which includes over 2 billion active devices. The focus is on integrating these new products with Apple's existing hardware, but the high prices could make it harder to reach a wider market.

Product Pipeline:

- Smart Home IP Camera (2026): Apple plans to start mass production of a smart home IP camera in 2026, with a goal of shipping over 10 million units each year. According to IDC, global smart camera shipments currently range between 30 to 40 million units annually, which means there’s a large potential market. The camera will connect wirelessly with HomeKit, Siri, and Apple Intelligence, offering improved features. The camera may sell for around $200, which is in line with Apple’s pricing for other accessories like AirPods ($150–$250). This could bring in $2–$3 billion in annual revenue. The gross margin is projected to be 40%, similar to the margins for AirPods and Apple Watch, due to the competitive nature of the market.

Product | Estimated Profit Margin |

iPhone | 40-45% |

Mac | 30-35% |

iPad | 30-35% |

Accessories | 35-45% |

Services | 70-75% |

Source: FourWeekMBA, Counterpoint, GlobalData, Forrester, Investopedia, Tradingkey.com

- Screen-Equipped HomePod (3Q25): Production of a HomePod with a screen is expected to start in mid-2025, following Apple’s WWDC event. The device will feature a 6–7-inch display and the A18 processor, shifting the HomePod’s focus from just audio to smart home management. Initial shipments are projected at 500,000 units in the second half of 2025, potentially scaling up to 1 million units annually by 2026, depending on how well it’s received in the market. Priced at an estimated $250–$300, revenue is forecasted to be $125–$150 million in 2025, increasing to $250–$300 million annually after that.

- AirPods (Health Integration): Beyond smart home products, Apple is upgrading AirPods with health features, such as heart rate monitoring. Shipments are expected to grow from 48 million units in 2023 to 53–55 million in 2024, 58–62 million in 2025, and 65–68 million in 2026, helping to boost revenue from accessories.

Pricing Strategy:

Apple’s premium pricing—$200 for the IP camera and $250–$300 for the HomePod—is much higher than competitors. For example, Xiaomi offers smart cameras for $30–$50, and Amazon’s Echo sells for $99. In the past, the original HomePod, priced at $349, sold only 2 million units annually, while the Echo sold 30–40 million. The $99 HomePod Mini reached 5 million units, showing that consumers are price sensitive. This trend is also seen with Vision Pro, priced at $3,499, which sold only 200,000 units in 2024.

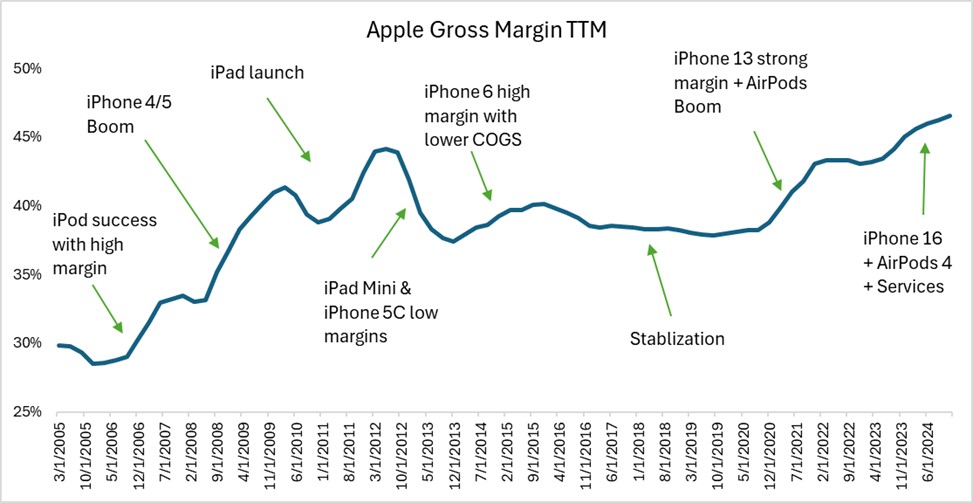

Apple focuses on high-end consumers who value sleek design and exclusivity, relying on brand loyalty to offer a premium, integrated experience. The expected adoption is from about 1% of its 2 billion device users—around 20 million buyers, mainly those who already own a full set of Apple products (e.g., iPhone, iPad, Mac), since its ecosystem doesn’t work well with non-Apple devices. However, Xiaomi and Amazon dominate the market with 15–20 million units annually, due to lower prices and broader compatibility. Apple’s high pricing will limit its market share, prioritizing profitability over volume. Apple’s success depends on releasing cutting-edge products. If successful, Apple could charge higher prices while increasing sales volume, leading to higher profit margins, as shown in the chart.

Source: MacroTrends, Tradingkey.com

Apple Intelligence (AI) – High Investment, Deferred Returns

Apple Intelligence, launched in 2024, is designed to improve device functionality through an upgraded Siri and generative AI features. Despite significant investment, its impact is still in the early stages.

Partnership with Alibaba:

Apple Intelligence debuted on the iPhone 16 and select Macs in October 2024. In China, where the iPhone 16 is being sold, Apple faced delays, and it has formed partnership with Alibaba (Qwen AI), which was shifted from a failed attempt with Baidu. This delay is further complicated by competition from Huawei’s new AI-equipped phones.

Hardware Upgrade:

Apple is preparing to integrate its M5 chip series into devices starting in 2025–2026, a move expected to significantly boost Apple Intelligence. These next-generation chips, currently in testing for mass production, will enhance AI performance—delivering faster Siri responses and smoother on-device tools—compared to the iPhone 16’s A18 chip. This upgrade aims to close the gap with competitors like Huawei, especially in China once the Alibaba partnership takes effect. It could also drive demand for future iPhones and Macs by making AI a stronger selling point.

Pricing and Adoption:

Apple Intelligence is offered at no additional cost—it’s embedded in the price of devices. CEO Tim Cook confirmed there are no plans for a subscription model, meaning Apple will need to increase device sales to grow revenue. However, iPhone shipments declined by 5% globally in 4Q24, and user surveys show limited enthusiasm for the feature, with many viewing it as a novelty rather than a necessity, according to IDC.

Strategic Potential:

In the long term, Apple Intelligence could boost the $25 billion Services segment by 10–20% if AI attracts 5–10% more users to Apple’s services. For smart home devices, a more capable Siri might help justify Apple’s premium pricing. However, the current lack of sales impact contrasts with competitors like Huawei, whose AI-enabled devices saw a 50% surge in China.

Delayed adoption in China adds to regional challenges, and consumers may need time to understand the value of AI in their devices. With $10–$20 billion invested, Apple Intelligence holds future potential but offers no immediate revenue boost. Its success depends on broader market acceptance, which remains unproven.

iPhone – Core Revenue Facing Headwinds

iPhone continues to be Apple’s revenue backbone, contributing $200 billion in 2024. While premium pricing maintains profitability, the company faces challenges with declining sales volumes and regional pressures.

Product Updates:

- iPhone 16e (February 2025): Priced starting at $599, which is not very attractive compared with iPhone 16 which sells from $799. It features Apple’s proprietary C1 modem, which helps reduce Qualcomm licensing costs. Shipments are projected at 10–15 million units, replacing the $429 SE model and integrating Face ID.

- Shipment Trends: Weak demand, including a 5% global decline in 4Q24, lowered iPhone shipments to 225 million units in 2024, with 2025 projected at 225–230 million—falling short of the 240 million consensus estimate.

Replacing Qualcomm:

Apple’s move to its proprietary C1 modem is part of a strategic effort to take control of its hardware ecosystem and reduce reliance on Qualcomm. For years, Apple depended on Qualcomm’s modems, paying licensing fees of $5–$6 per iPhone—totaling $1.1–$1.35 billion annually on the 225 million units shipped in 2024. After a failed attempt with Intel modems and a 2019 settlement that tied Apple to Qualcomm until 2027, Apple began developing the C1 modem. It acquired Intel’s modem team to create a chip tailored to its needs. This mirrors Apple’s success with its A-series and M-series chips, aiming to optimize performance, cut costs, and avoid third-party limitations in an increasingly competitive market.

Pricing Strategy:

The iPhone 16 Pro and Pro Max models accounted for 60% of total iPhone shipments in 4Q24, up from 50% in 4Q23. This helped maintain an average selling price (ASP) of $1,000 and limited iPhone revenue declined to 0.8%, despite a 5% drop in global shipments. In China, however, discounts of 10–15% failed to prevent a 11% sales decline, driven by competition from other smart phone brands and economic challenges.

Source: Canalys

Volume and Risks:

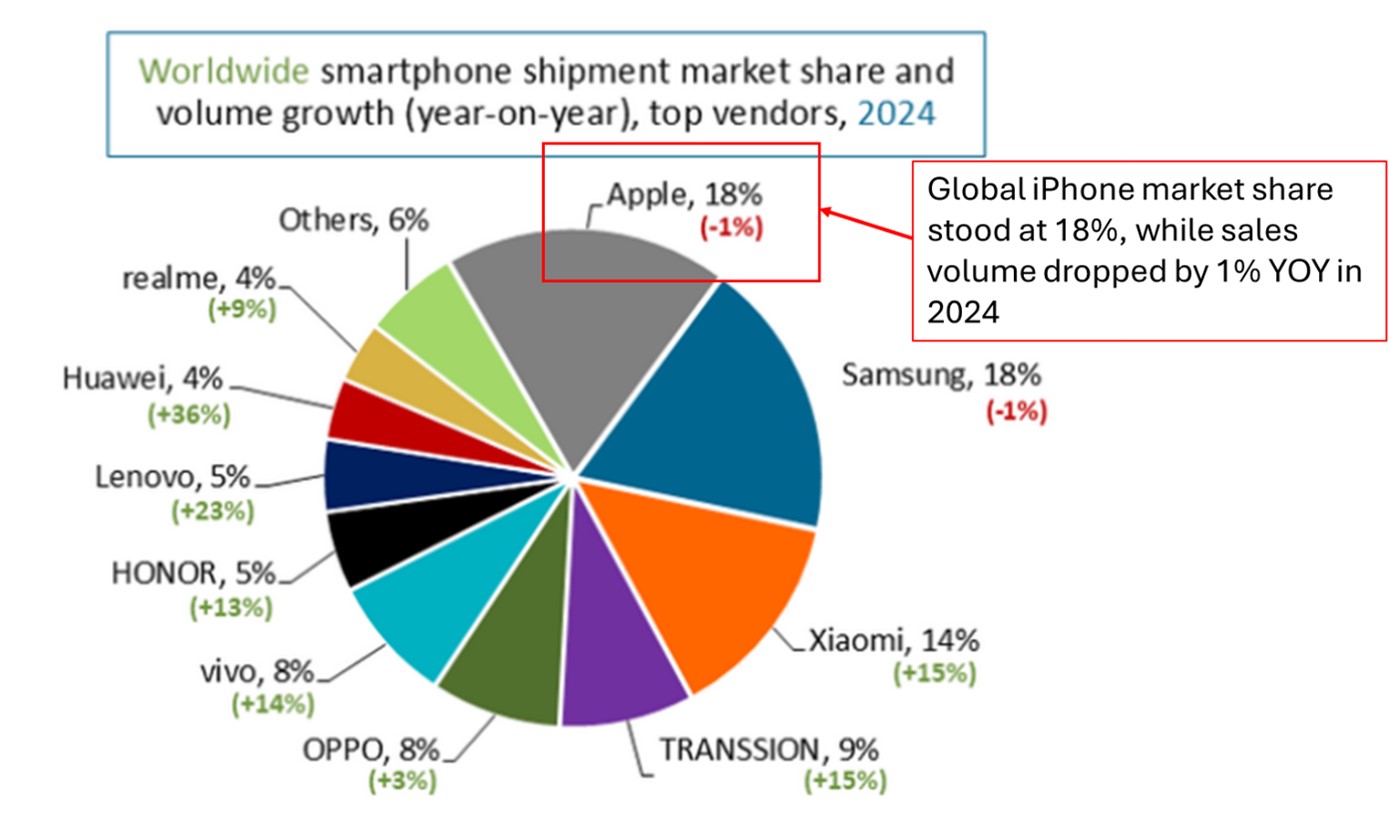

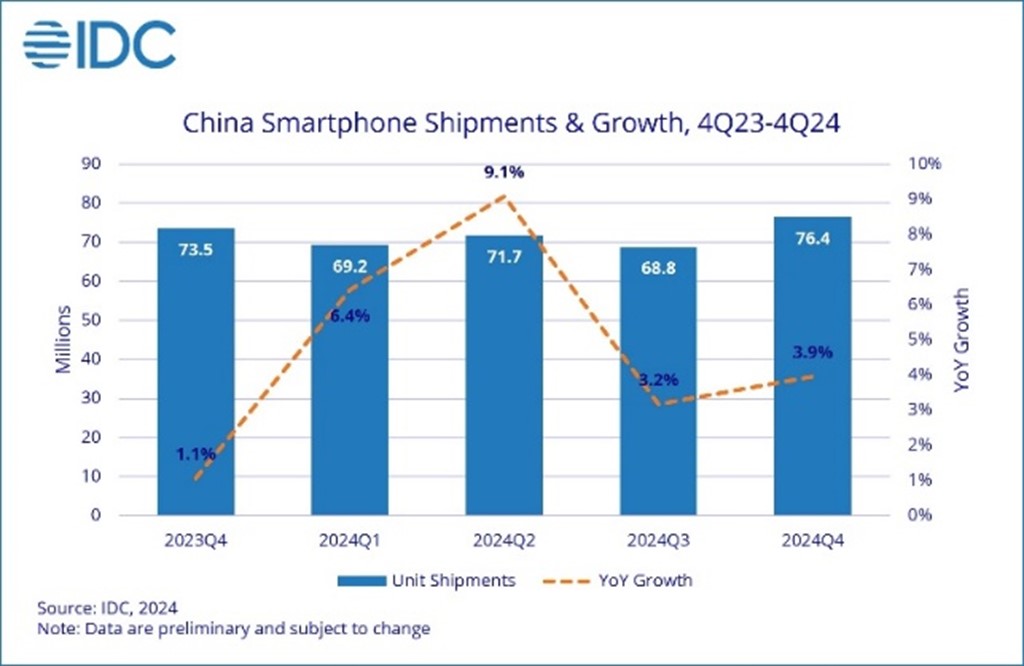

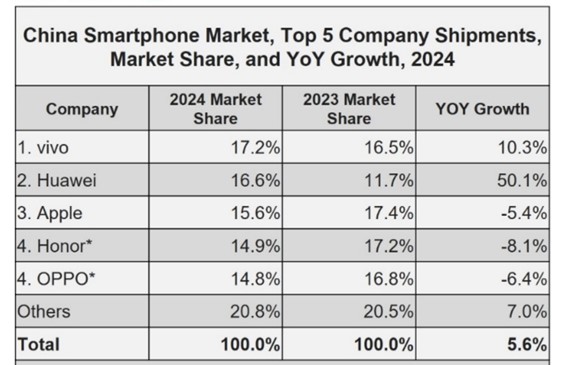

China’s market presents significant risks for Apple. Huawei’s shipments grew by 50% in 2024, securing a 16.6% market share compared to Apple’s 15%. While smartphone shipments in China are recovering, Apple’s total revenues from China dropped 11% in Q1 FY2025. In the meantime, potential 25% tariffs on $40–$50 billion worth of China-made iPhones could increase costs, though Apple is mitigating this risk by shifting production to India (currently around 14%, projected to reach 25% by 2027). Upcoming thin and foldable models (expected in 2H25) may face adoption challenges in China due to their eSIM-only design. Additionally, globally, smartphone brands beyond Apple and Samsung saw strong growth in 2024, and Apple’s decline may continue into the first half of 2025.

Source: IDC

Source: IDC

Apple’s premium pricing and strong brand loyalty help maintain its resilience, with the C1 modem expected to boost margins by 2027 through cost savings. However, the lack of significant design innovation—with no major updates since 2020—and intense regional competition, particularly from Huawei in China, pose risks. These factors could lead to a 5% revenue decline in iPhone revenue.

Valuation

Apple’s currently has a forward P/E of 33x, is supported by $100 billion in free cash flows, $80–$100 billion in annual share buybacks, and sustained growth from Services and premium iPhone sales. We estimate Apple’s FY2026 EPS at $7.50 in our base case, factoring in stable iPhone revenue, sustained Services growth with limited AI contribution, and modest Smart Home performance. Using a 30x P/E multiple, which aligns with Apple’s typical historical valuation, we project the stock’s future performance. The table below outlines base, bull, and bear scenarios based on segment performance.

Assumptions:

- Smart Home: Expected to contribute $4–$6 billion, adding $0.20–$0.30 to EPS if successful; minimal impact if pricing struggles.

- Apple Intelligence: A $10–$20 billion investment yields no immediate return; long-term potential includes a $2.5–$5 billion uplift in Services, adding $0.25–$0.50 to EPS. Downside risk includes investor skepticism, potentially reducing the P/E to 25x.

- iPhone: Stability at $200 billion maintains $7.50 EPS; a 5% decline to $190 billion by 2026 would reduce EPS by $0.30, partially offset by $0.40–$0.50 in savings from the C1 modem.

Scenario | FY2026 EPS | P/E | Stock Price |

Base Case | $7.5 | 30x | $225 |

Bull Case | $8.80 ($7.50 + $0.30 SH + $0.50 AI + $0.50 iPhone) | 30x | $264 |

Bear Case | $6.70 ($7.50 - $0.30 iPhone - $0.50 AI) | 25x | $167 |

Scenario Analysis:

- Base Case ($225): Assumes iPhone revenue remains stable at $200 billion, modest growth in smart home products, and limited impact from AI by 2026. With a 30x multiple on $7.50 EPS, the stock is valued at $225.

- Bull Case ($264): Reflects maximum contributions from smart home ($0.30 EPS), AI ($0.50 EPS), and iPhone modem savings ($0.50 EPS), resulting in $8.80 EPS. At a 30x multiple, this aligns with $264, suggesting limited upside from the current stock price unless all segments outperform expectations.

- Bear Case ($167): Factors in a 5% decline in iPhone revenue to $190 billion (a $0.30 EPS hit) and a drag from AI investments ($0.50 EPS), with the P/E multiple contracting to 25x due to market concerns.

Recommendation:

The target price range for Apple based on our estimates is between 167 and 264. The current stock price may reflect optimism not fully supported by segment performance. A fair value of $225 aligns with steady growth, with a potential buy point at $200 if risks in China or pricing pressures emerge. Apple’s strong cash flow and share buybacks provide downside support, though contributions from smart home and AI are expected to remain incremental through 2026.