Microsoft: Expecting Turnaround in Business but Valuation Not So Attractive

.jpg)

Source: TradingView

Key Points

- Microsoft has been underperforming the broad market due to supply issues in its cloud business, mostly related to data centers and AI infrastructure

- Microsoft’s profits mainly come from its business software and cloud products

- Microsoft has a very strong market position due to its brand value and decade-forged connections with large customers

- With the OpenAI cooperation and multi-billion-dollar investments in AI, Microsoft can fuel its growth for the years to come

- We will observe a rebound in the performance of the cloud business, but valuation is not the most attractive

Overview

Microsoft stock (MSFT) price could not find a clear direction last year, mostly because of its Cloud business facing slowing growth rates and decreasing margins. The issues related to Cloud appear to be more of a temporary problem, rather than structural decline, making us feel optimistic for a future turnaround. After all, Microsoft is a company with a very strong business moat, currently investing heavily in AI. However, it is not exactly cheap at the valuation of 32x PE, as other MAG7 companies like Google and Meta can be a better bargain.

Microsoft Business Description

Historically, Microsoft became a tech giant by developing and selling the Windows Operating system in the 1980s and 1990s. Nowadays Microsoft has several different business lines, all grouped into three main segments:

Productivity and Business Process: All the products and services related to productivity include the Microsoft Office software suite, the social media platform LinkedIn, as well as other enterprise-related solutions and apps. Copilot and Dynamic 365 are part of this segment.

Intelligent Cloud: This segment encompasses public, private and hybrid cloud services primarily aimed at developers operating in the areas of data and AI. The main components of this segment include Azure, SQL Server and Windows Server.

More Personal Computing is the segment that is more closely related to PCs. It includes Windows, Xbox games and consoles and Bing and MSN portal.

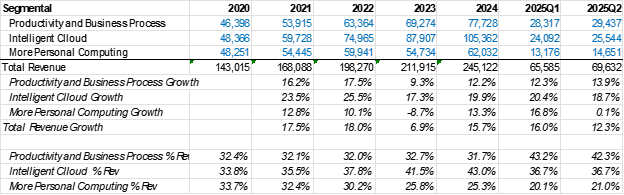

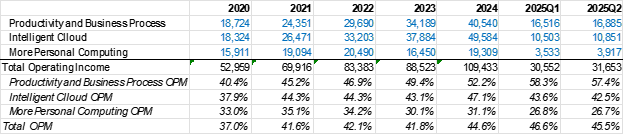

Until recently, the three segments used to contribute relatively equal amounts of revenue and profits, but due to the higher growth in business software and cloud, we can see how Microsoft has become more tied to these two business lines.

Source: TradingKey, SEC Filings

Source: TradingKey, SEC Filings

The Business Software Industry: Increasingly Competitive but Microsoft Stands Strong

The enterprise software market is large and complex, with many products with different functionalities (business email, communication tools, productivity tools, database solutions and others). It is hard to compare different products and players, as they may simply have different strengths and weaknesses, or they can have different targeted customer bases.

Despite that, it is safe to say that Microsoft and its flagship product Office 365 provide the most comprehensive set of tools on the market.

Google is the other market player that provides a similar wide scope of tools that Microsoft has. However, the clientele of Google Workplace is different from Microsoft’s. Google positions itself as more friendly towards smaller, fast-growing and cloud-native businesses with its more affordable pricing. On the other hand, Microsoft's stronghold are the larger and more established corporations.

We also have other players like Salesforce, SAP, Monday.com and ServiceNow that have a more specific focus on enterprise resource planning (ERP), customer relationship management (CRM) and project management. These players and products are seen more as complementary, rather than a potential alternative to Microsoft and Office 365.

We believe that the main role of Microsoft in this industry will remain. Throughout decades of operations, Microsoft was able to forge strong connections with clients, creating a very strong brand value and mind share among customers. The long-lasting business connections also make the switching costs quite unjustifiable. Thus, it seems unlikely to see a significant migration away from Microsoft towards competitor platforms.

The Current Cloud Computing Landscape: A Multifaceted Ecosystem

Cloud business is the process of providing on-demand access to hardware and computing resources over the Internet. The cloud industry can be summarized into three main types of service models, catering to diverse needs:

- Infrastructure-as-a-Service (IaaS): Provides on-demand access to computing resources like virtual machines, storage and networking. It offers maximum control and flexibility, ideal for organizations with complex infrastructure requirements. This is the least lucrative segment, as the providers of IaaS need to invest heavily in hardware.

- Platform-as-a-Service (PaaS): Offers a platform for developing, deploying and managing applications without the need to manage the underlying infrastructure. Simplifies development and deployment, accelerating time to market. PaaS is the fastest-growing cloud segment with a CAGR of 20%+ since developers of apps and software will primarily use PaaS.

- Software-as-a-Service (SaaS): Provides on-demand access to software applications over the internet. Eliminates the need for software installation and maintenance, simplifying IT management and reducing costs. SaaS is also growing at a high rate and it also has the highest level of margins among the three segments.

The way Cloud models are deployed also differs:

- Public Cloud: Resources are shared among multiple users, providing cost-effectiveness and scalability. Suitable for organizations with varying needs and budget constraints.

- Private Cloud: Resources are dedicated to a single organization, offering greater control and security. Ideal for organizations with stringent security and compliance requirements.

- Hybrid Cloud: Combines public and private cloud resources, allowing organizations to leverage the benefits of both models. Offers flexibility and scalability while maintaining control over sensitive data.

- Multi-Cloud: Utilizes multiple public cloud providers to diversify risk and leverage the strengths of different platforms. Provides resilience and avoids vendor lock-in.

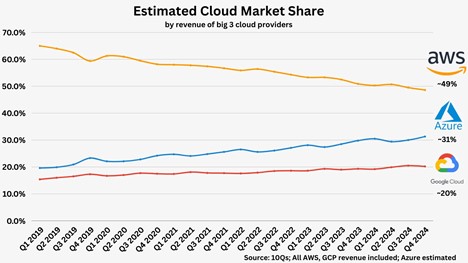

The cloud computing industry is less fragmented than the business software industry. Here we see a well-defined top three players taking the majority of the market – Amazon (AWS), Microsoft (Azure) and Google (Google Cloud). They provide services across all cloud types and service models. However, AWS is more focused on IaaS, while Azure and Google Cloud are specializing in PaaS and SaaS.

Source: Generating Value

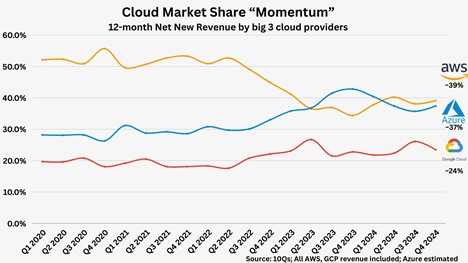

Source: Generating Value

Source: Generating Value

Looking at the market share development in the past years, we can see a clear trend of Amazon losing market share, while Microsoft and Google are gaining more ground.

As the oldest cloud company and having the first-mover advantage, Amazon was able to occupy the dominant market share within the industry in the early days. However, the more recent players like Azure and Google Cloud are successfully catching up. Amazon Web Services (AWS) still has the most comprehensive package of tools from all three, but that also means Azure and Google Cloud have more room for growth.

Azure and Google Cloud seem to position themselves better among large corporate clients and SMEs respectively. In the case of Azure, the integration with the rest of the Microsoft system within the organization is relatively smooth making the case for Microsoft cloud business quite strong.

Recently, what we have been observing in all cloud players is the decelerated growth and retreating margins. For Azure, specifically, we can see the growth rates decelerated to below 20% and the operating margin went down several percentage points.

Despite the investors’ concerns about slowing demand, the reality is that supply issues are causing the revenue growth to go down. Currently, the rate of development of the physical infrastructure (building data centers) cannot catch up with the rate of demand growth for cloud services, putting a temporary cap on the growth across the cloud sector. As of today, the industry is predominantly optimistic that with the increasing amount of capital expenditures, the supply bottleneck will be resolved.

Microsoft-OpenAI Relationship

An important part of Microsoft's AI strategy is its relationship with OpenAI, the company that owns the ChatGPT series of models. The business relationship between the two sides is quite complex and most details are not fully disclosed, but it looks like this:

API: Copilot is run on OpenAI, GPT-4 and OpenAI API is exclusive for Azure and run on Azure. Also, Microsoft has invested roughly 13 billion dollars in OpenAI.

Investment: Microsoft has already invested over 13 billion dollars in OpenAI. However, this is not considered a direct ownership but more like “economic interest” where Microsoft can claim a portion of OpenAI profits.

Exclusive Cloud Provider: Microsoft Azure is the exclusive cloud provider for OpenAI, powering all of OpenAI's workloads, including research, products and API services. This makes OpenAI one of Azure's most significant clients.

Integration into Microsoft Products: OpenAI's models are integrated into various Microsoft products, such as Microsoft 365 Copilot, enhancing their capabilities with advanced AI

Revenue Sharing: Both companies benefit from mutual revenue-sharing agreements, ensuring that increased use of AI models benefits both parties.

Growth and Profitability Outlook

In terms of average revenue growth for the coming 2-3 years, we expect a number within the 15% range. On the one hand, Microsoft operates in a quite mature market in which the degree of penetration is already reasonably high. However, there are a few positive drivers for revenue growth in the coming years:

Introduction of AI features: Clients will start utilizing the newly introduced AI features (Copilot) and this will enable Microsoft to increase the prices of their products.

Cloud Growth will rebound: The supply issues related to the lack of available hardware infrastructure are gradually going to be addressed with extensive capital expenditures aimed at building more data centers. This itself will unlock cloud revenue growth to re-accelerate.

In terms of profitability, we expect margins to not change significantly despite the increased spending on AI, because we will see a positive impact from the new high margin functions the company is currently implementing.

Valuation

Currently, Microsoft is trading at around 32x the last twelve months’ earnings. The number is not extremely high, but not low either, as it is slightly above the historical PE levels of the company. This implies a limited growth in the stock price. However, we are yet to see the extent to which AI will impact Microsoft’s valuation.