Wells Fargo (WFC): Can Regulatory Easing Lift It to the Next Level?

.jpg)

Source: TradingView

Executive Summary

Wells Fargo (WFC) has staged a remarkable comeback, surging 62% over the past year, significantly outperforming SPX’s 20.51% gain. Year-to-date, the financial sector (XLF +6.53%) has been one of the best-performing sectors, and WFC remains strong momentum (+12.91% YTD)—a reflection of investor confidence in its earnings resilience and potential regulatory tailwinds.

As the fourth-largest U.S. bank, Wells Fargo is rebuilding its reputation from past scandals while capitalizing on policy shifts. Potential regulatory easing under the Trump administration could unlock greater flexibility in lending and capital markets, bolstering profitability.

However, short-term challenges remain. Net Interest Income (NII) declined 7% YoY due to margin compression, though expected rate cuts in 2025 could stimulate loan demand and partially offset NII pressures. Meanwhile, noninterest income surged 11% YoY, fueled by investment banking, wealth management, and credit card fees, reducing reliance on NII.

It is projected to have a target price of $103 per share over the next 12 months, reflecting a 30% upside potential. Wells Fargo currently is trading at a reasonable forward P/E of 13.59x, supported by a solid CET1 ratio of 11.1% and an ROE of 10.84%. While risks such as economic slowdown, regulatory delays, and market volatility exist, Wells Fargo's efficiency gains, recovering reputation, and favorable macro trends position it as a compelling long-term investment.

Company Overview

As the fourth-largest bank in the United States, Wells Fargo was founded in 1852 and is headquartered in San Francisco, California. With a history spanning over 170 years, Wells Fargo gradually developed into a diversified financial institution, offering a wide range of services, including retail banking, corporate and investment banking, wealth management, and commercial banking. With consistent mergers & acquisitions, a vast customer base, a diversified revenue model, and strong brand recognition, Wells Fargo has grown to become one of the largest banks in the world.

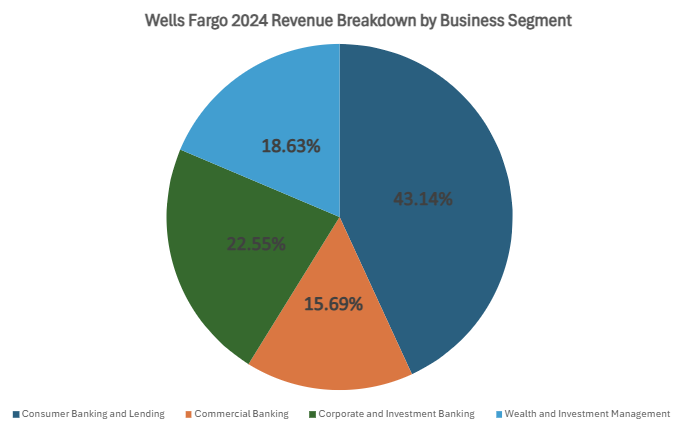

Wells Fargo's business is organized into 4 key business segments, each contributing to the company's overall financial performance. As of the end of 2024, the primary segments and their respective contributions are:

1. Consumer Banking and Lending: As the company’s largest revenue driver, this segment accounted for 43.14% of total revenue in 2024, generating $36.2 billion. It offers financial products and services to individuals and small businesses, including deposit accounts, credit and debit cards, and a variety of lending solutions such as home, auto, personal, and small business loans.

2. Corporate and Investment Banking: Contributing 22.55% of total revenue with $19.34 billion in 2024, this segment serves corporations, government entities, and institutional clients worldwide. It provides investment banking, corporate banking, treasury management, commercial real estate financing, equity and fixed income solutions, as well as sales, trading, and research capabilities.

3. Wealth and Investment Management: Generating $15.44 billion, or 18.63% of Wells Fargo’s 2024 revenue, this division offers personalized wealth management, investment, and retirement solutions. Through U.S.-based businesses like Wells Fargo Advisors and The Private Bank, it serves a broad range of clients seeking financial planning and asset management services.

4. Commercial Banking: Focusing on providing financial services to private, family-owned, and publicly traded businesses, this segment offers traditional commercial loans and lines of credit, asset-based lending, lease financing, and manages Wells Fargo's foreign loan portfolio. In 2024, it generated around $12.78 billion in revenue.

Source: Wells Fargo, TradingKey

Industry Positioning

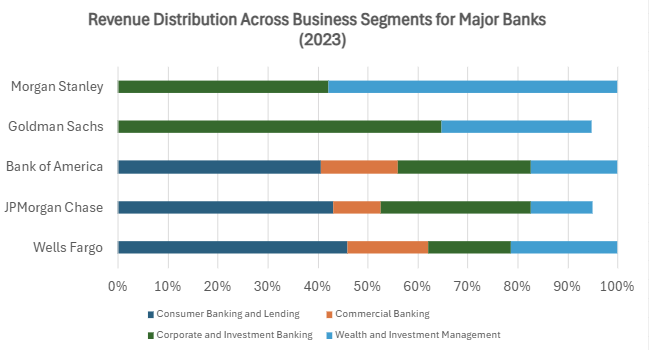

Based on the 2023 revenue data, Wells Fargo distinguishes itself from other major banks by its heavy focus on retail banking and consumer lending, which make up a significant portion of its revenue. While banks like JPMorgan and Bank of America also have strong retail banking divisions, they balance this with larger contributions from investment banking and wealth management. In addition, Goldman Sachs and Morgan Stanley are more focused on corporate and investment banking and wealth management, with limited exposure to traditional banking services.

Wells Fargo's focus on traditional banking services positions it as a stable, low-risk player in the market and this steady business model makes Wells Fargo less dependent on market fluctuations, unlike its competitors, who are more exposed to the volatility of capital markets. As a result, Wells Fargo is better positioned as a consistent, interest rate-sensitive institution.

Source: Refinitiv, TradingKey

Business Model & Market Strengths

- Diverse Business Model: Wells Fargo operates a diversified business model across various financial services, which allows the bank to generate revenue from multiple sources and mitigate risks associated with market volatility.

- Extensive Retail Banking Network: With over 4,100 branches, Wells Fargo has a strong domestic footprint, especially dominant in home loans and credit card services. This extensive presence helps capture a wide customer base across the U.S., making Wells Fargo the fourth-largest bank in the country by assets ($1.69 trillion).

- Robust Deposit Base and Diversified Loan Portfolio: Wells Fargo excels in deposit services, with average deposits of $1.4 trillion in 2024. On the other flip, Wells Fargo maintains a balanced portfolio across mortgage loans, credit cards, and commercial lending. Unlike JPMorgan Chase and Bank of America, which have significant exposure to capital markets, Wells Fargo remains more reliant on traditional banking operations.

- Strong Brand and Customer Base: Wells Fargo's brand is one of its most valuable assets. With a customer base of over 70 million worldwide, Wells Fargo benefits from strong customer loyalty.

Financial Performance---Key for Understanding the Banking Company

1. Revenue & Profit Analysis

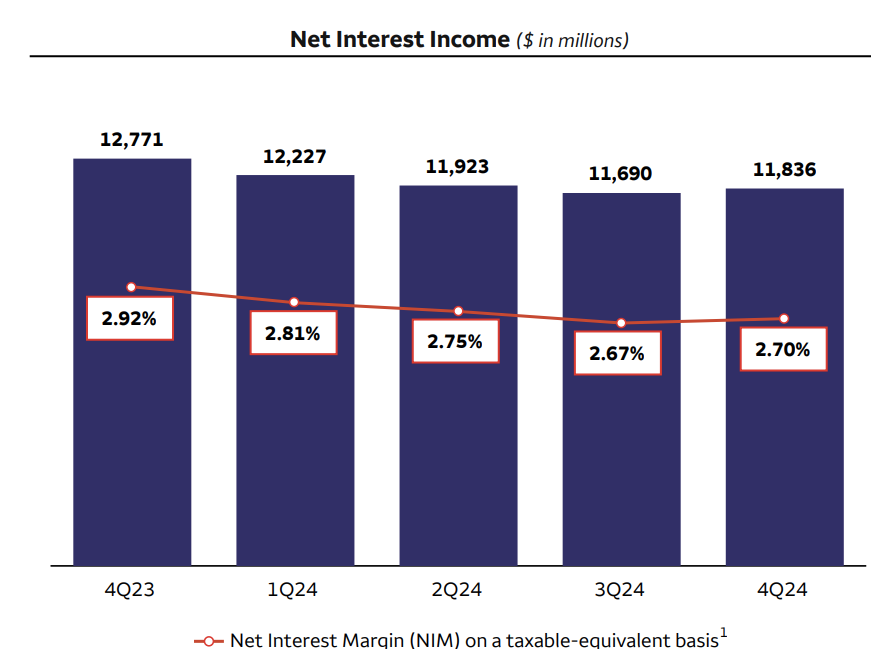

- Net Interest Income (NII)

Wells Fargo's Net Interest Income (NII) dropped by 7% YoY to $11.8 billion in 4Q24, mainly due to lower deposit margins and sluggish loan growth. The Net Interest Margin (NIM) slipped to 2.70%, reflecting the challenges of low rates and changing deposit mixes.

Looking ahead to 2025, Wells Fargo expects NII to grow by 1-3% compared to 2024. This growth is anticipated to come from modest loan expansion, particularly in corporate banking and credit cards, as well as reinvestment in higher-yielding assets. The bank's focus on higher-margin assets and diversified revenue streams suggests a strategic shift away from heavy reliance on traditional lending.

However, given expectations that the Federal Reserve will continue cutting rates in 2025, the short-term impact on Wells Fargo may be negative, as loan yields could decline faster than deposit costs, leading to NIM compression and a direct reduction in NII. In the mid to long run, if rate cuts stimulate loan demand, Wells Fargo could partially offset NII losses by expanding its loan portfolio and leveraging increased borrowing activity to drive revenue growth.

Source: Wells Fargo

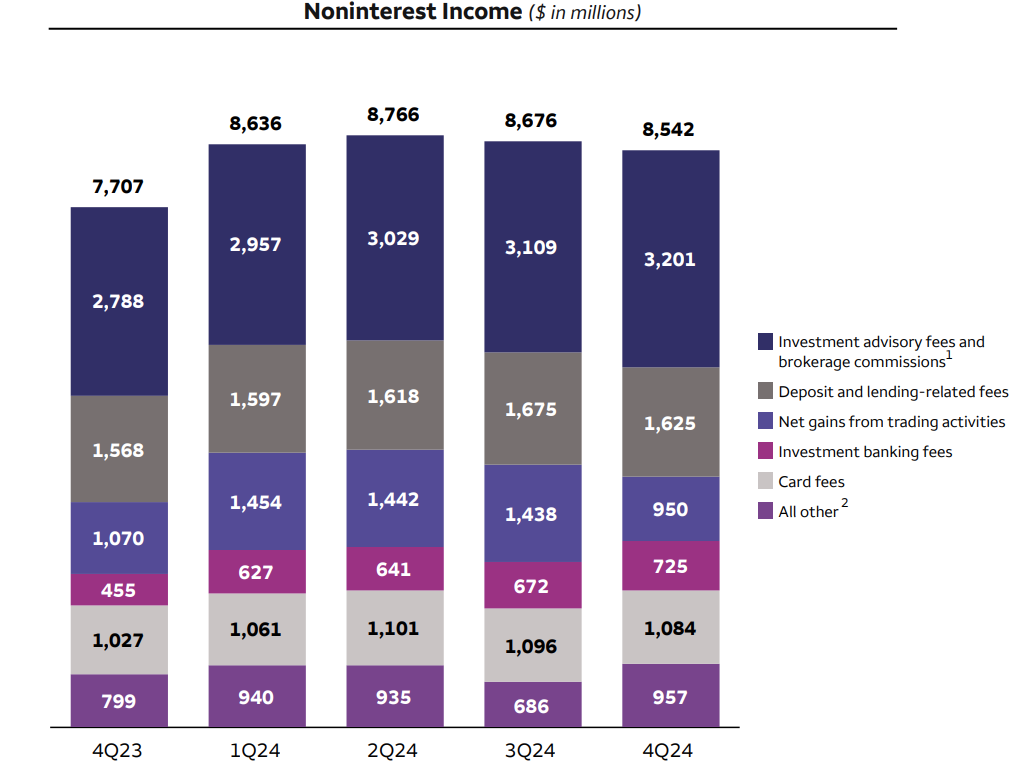

- Noninterest Income

Noninterest Income surged 11% YoY in 4Q24, reaching $8.5 billion, driven by strong growth in investment advisory fees, investment banking revenues, and credit card fees.

Wells Fargo is optimistic about maintaining strong noninterest income growth in 2025, driven by continued demand for advisory services and investment banking, positioning the bank as being less dependent on interest rate fluctuations. Most importantly, Trump's deregulatory policies could reduce regulatory burdens on the financial sector, especially in investment banking and capital market activities, Wells Fargo is expected to gain more flexibility to innovate and expand its business. Additionally, the expectation of continued rate cuts in 2025 could boost market activity, benefiting wealth management and investment banking businesses. These factors contribute to growth in noninterest income, particularly in fees related to trading and investments.

Source: Wells Fargo

- Net Profit

Wells Fargo reported net income of $5.1 billion, with diluted earnings per share (EPS) at $1.43, reflecting a 49% YoY increase. This growth was driven by lower noninterest expenses (-12% YoY), strong performance in investment banking and advisory services, and effective cost management.

The net margin trend over recent years shows that it has remained stable with signs of improvement, aligning with Wells Fargo’s focus on cost efficiencies and fee-based income expansion. The bank expects stable earnings growth in 2025, supported by continued cost discipline, diversification in revenue streams, and a modest rebound in net interest income (NII).

Source: Refinitiv

2. Credit Quality

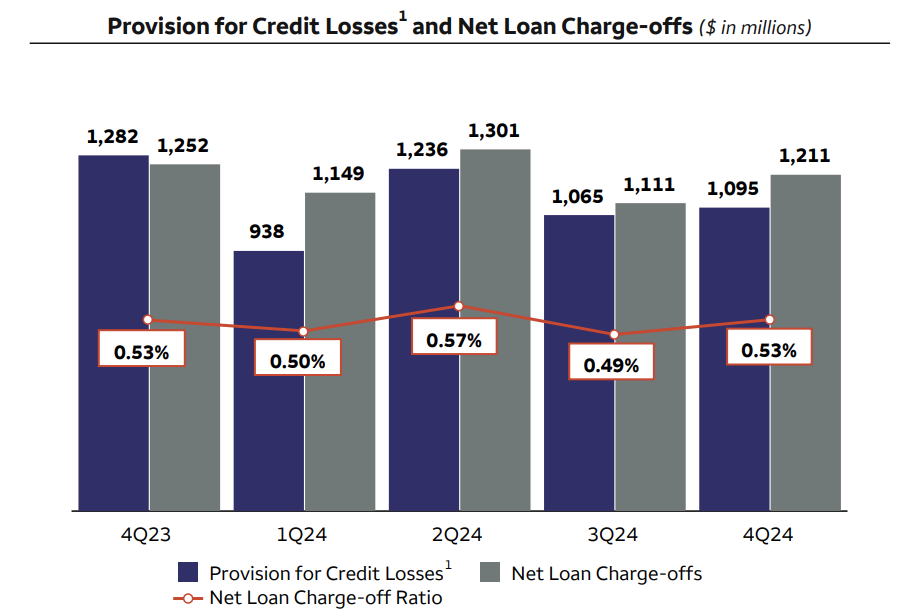

- Net Loan Charge-Offs

In 4Q24, Wells Fargo reported net loan charge-offs of $1.2 billion, down by $41 million YoY, with a charge-off ratio of 0.53%. The decline was mainly driven by improvements in certain loan categories. The management anticipates stable charge-offs in the coming quarters, which is a positive indicator for future earnings, as the bank continues to keep bad debts under control despite economic pressures.

- Provision & Allowance for Credit Losses

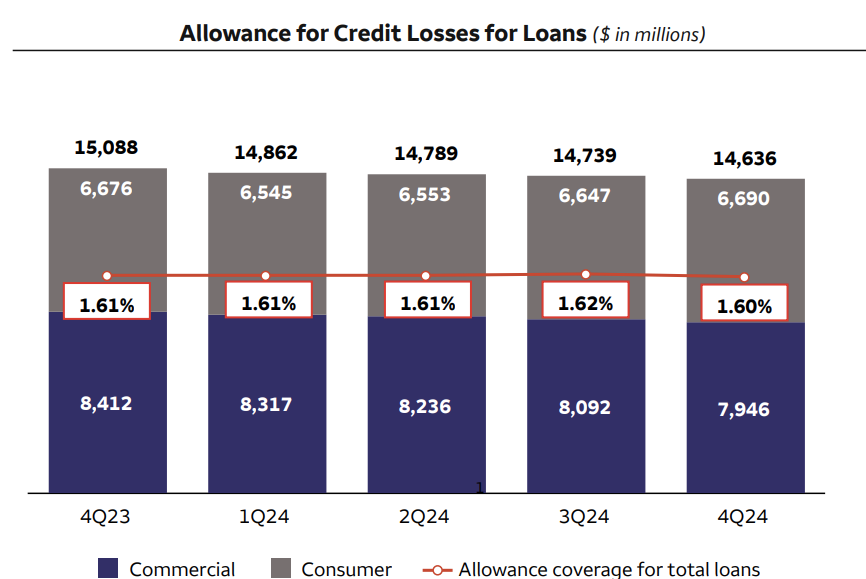

In 4Q24, provision for credit losses fell 15% YoY to $1.1 billion, while the allowance for credit losses (ACL) decreased 3% YoY to $14.6 billion. Based on the expectation, both ACL and provisions are expected to remain stable, which is a strong indication of a healthy credit environment and a relatively stable loan portfolio.

Source: Wells Fargo

Source: Wells Fargo

- Commercial Real Estate (CRE) Quality

CRE net charge-offs rose to $261 million in 4Q24, primarily driven by office loans. Nonperforming CRE assets decreased, but office real estate remains a challenge. The bank is expected to continue facing headwinds in the CRE office sector, with modest improvements in the overall CRE portfolio if the market stabilizes.

The market currently expects the Federal Reserve to cut interest rates twice in 2025. If the Federal Reserve cuts rates, Wells Fargo’s CRE risk exposure could see some relief, particularly in financing cost reductions and valuation recovery. However, the office sector still faces structural challenges (e.g., remote work trends), meaning that rate cuts alone won’t fully eliminate risks.

3. Capital & Liquidity Position

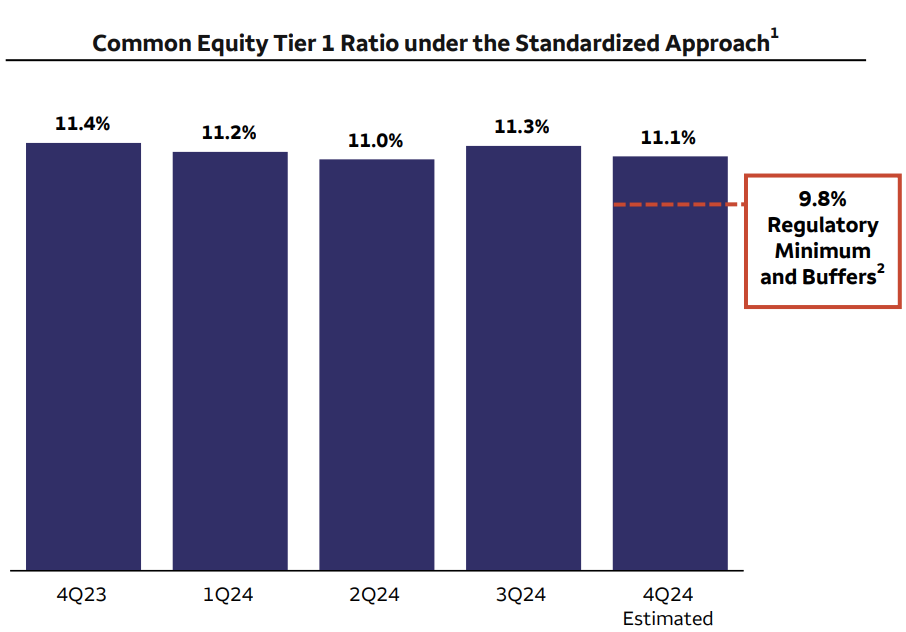

Wells Fargo maintains a strong capital position, ensuring regulatory compliance and financial stability. As of 4Q24 (estimated), the bank’s Common Equity Tier 1 (CET1) ratio under the stood at 11.1%, well above the 9.8% regulatory minimum (including buffers).

Capital Adequacy Trends:

- CET1 ratio declined slightly from 11.4% in 4Q23 to 11.1% in 4Q24, reflecting capital deployment and risk-weighted asset (RWA) adjustments.

- Despite the decline, the capital buffer remains strong, providing resilience against market uncertainties. The CET1 ratio remains above regulatory requirements, ensuring financial flexibility for future growth and risk management.

Liquidity Position:

Wells Fargo’s Liquidity Coverage Ratio (LCR) remains at 125%, exceeding the 100% regulatory threshold, ensuring ample liquidity to meet short-term obligations.

Looking ahead, Wells Fargo will focus on balancing capital efficiency with regulatory compliance, ensuring steady capital returns while maintaining a strong liquidity buffer.

Source: Wells Fargo

Valuation

- P/E & P/B

Wells Fargo's forward P/E of 13.59 is above the sector median (12.29) but lower than Morgan Stanley and JPMorgan Chase, reflecting market expectations for stable profitability. Its P/B ratio of 1.63 exceeds the sector median (1.30), indicating strong asset returns but a relatively moderate valuation compared to Goldman Sachs and Morgan Stanley. Overall, Wells Fargo's valuation remains reasonable, making it suitable for long-term investors seeking steady returns. If the interest rate environment improves or cost efficiencies materialize, there is potential for further valuation expansion.

Source: Refinitiv, TradingKey

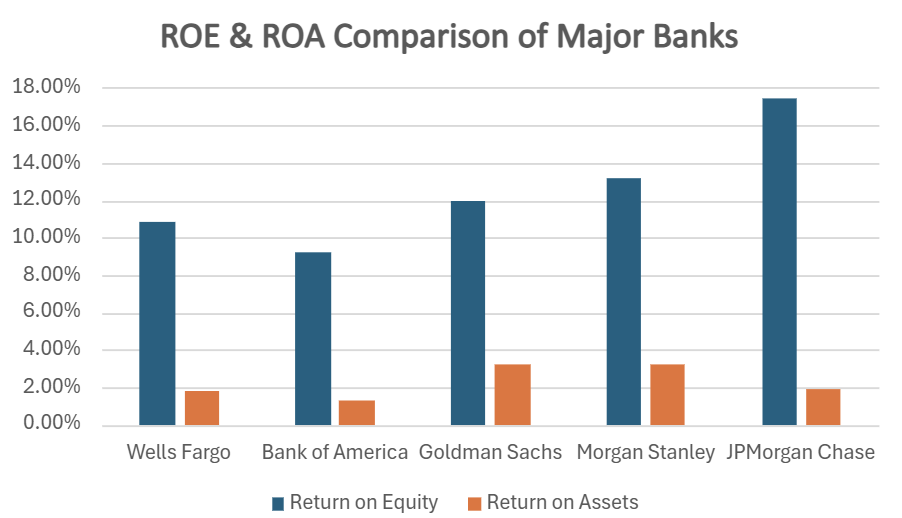

- ROE &ROA

Wells Fargo's ROE is 10.84%, ranking fourth among the five major banks. However, it still maintains a double-digit return, demonstrating solid shareholder profitability. Its ROA is 1.75%, positioning it above average, outperforming Bank of America, which reflects efficient asset utilization. While slightly lower than investment banking-focused competitors Goldman Sachs and Morgan Stanley, it remains competitive within its retail and commercial banking-driven model.

Source: Refinitiv, TradingKey

Investment Recommendation

Overall, Wells Fargo's current valuation appears reasonable, supported by its strong retail banking foundation, ongoing digital transformation, and gradual compliance improvements. Additionally, the potential deregulatory policies under the Trump administration could serve as a tailwind, enhancing its profitability outlook. Given the bank’s solid financial performance, strong ROE, and growth potential, a fair valuation range of 15-20x P/E seems appropriate. Based on Refinitiv’s average EPS estimate of $6.88 for the next three years, this implies a target price of $103 per share in the following 12 months, representing approximately 30% upside from current levels.

However, key risks include a macroeconomic slowdown, which could reduce credit demand and increase non-performing loans, impacting profitability. Regulatory delays in lifting restrictions may limit business expansion and earnings recovery, dragging down the valuation. Additionally, financial market volatility could pressure credit quality and capital markets revenue, creating earnings uncertainty.

While Wells Fargo presents an attractive investment opportunity, investors should weigh these risks carefully, as economic downturns, regulatory setbacks, or market disruptions could limit upside potential and delay the expected valuation re-rating.