META: Is There Any Further Room for Growth After Q4?

By Petar Petrov

Source: TradingView

Key Points

- Meta is in the middle of an intensive AI capex cycle, which will weigh on margins and EPS growth in the near future

- Meta’s brand value is so strong that it has defined the age we live in – the age of social media

- The high margin nature of Meta’s ad business enables them to invest massive amounts of funds into AI

- With the emergence of open-source language models, Meta can utilize the capabilities of their Llama family of models to become a frontrunner in AI

- In the long run, the AI-related tools will help Meta provide a strong value proposition to advertisers

- Meta has plenty of room for monetization, with Threads still in early stage

- In the context of Mag7, Meta is quite cheap, but the gloomy earnings prospects related to the near future spending make the stock already not attractive

Investment Thesis

Meta's stock price has grown remarkably in the past two years, and rightfully so. Its high-margin ad business generates a great deal of cash, which is being used to invest in various innovations. The newly developed innovations improve the products Meta offers (more efficient ad targeting) to generate even more cash, creating a one-of-a-kind virtuous circle.

From the recent Q4 earnings, it appears that Meta is in the middle of an intensive AI capex cycle, which will weigh on margins and EPS growth in the near future. This means we will probably not see a significant surge in the stock price in the coming quarters.

Long-term, however, Meta is well-positioned for growth due to 1) AI-related investments will help improve users’ engagement across platforms, thus improving the number of ad impressions; 2) AI-related tools and products will help advertisers develop campaigns with higher efficiency and accuracy, allowing Meta to increase ad prices; 3) the company will start monetizing the currently growing platforms like WhatsApp and Threads once they gain enough critical mass.

Overview

Meta owns some of the most popular social media platforms, including Facebook, Instagram, WhatsApp, and Messenger. For the past fifteen years, Meta has been dominating the social media world, with nearly half of the global population using at least one of its products.

Meta’s brand value is so strong that it has defined the age we live in – the age of social media. It is hard to imagine a world without Facebook or Instagram. Meta's success stems from its deep understanding of user preferences and its ability to adapt, coupled with its technical prowess. The interconnectivity across its platforms (e.g., seamless navigation between Facebook, Instagram, Threads, and Messenger) also helps retain users.

Meta is part of the "Magnificent 7" stocks, alongside NVDA, AMZN, MSFT, AAPL, TSLA, and GOOGL. It is currently among the leading AI scalers, riding the AI wave with these companies.

How does Meta make Money from Digital Advertising?

Meta does not charge their user base. Instead, they provide various ways for businesses to advertise their products and services on their platforms. Basically, businesses buy ad space that is placed on Meta’s social media platforms and apps, including Facebook, Instagram, Messenger, and WhatsApp.

Ad prices are determined by an auction system based on bids and performance. Businesses are charged only for the number of clicks ads receive or the number of impressions (the number of times the ad is displayed).

Ads can appear between the stories, in between the posts, as sponsored content, or as “suggested for you” content. The greatest strength of Meta (and other digital platforms) is that with the huge amount of data collected from users, they can personalize the ads they push based on user profiles. This can significantly improve the efficiency of the ad campaign.

Meta Ads operates on a CPM (Cost-Per-Thousand Impressions) model where advertisers are charged based on the number of impressions or views their ads receive per thousand. This differs from Google, where advertisers are charged per click or engagement.

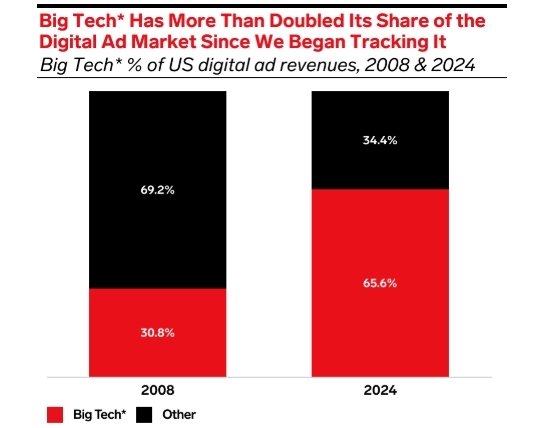

With the further development of their capabilities and creating a technological advantage, big tech companies will continue to gain ad dollars on the expense of non-big tech companies.

Source: eMarketer

Ad Business as a Solid Cash Cow

Source: TradingKey, SEC Fillings

Ad-related businesses usually have a very high margin due to the lack of upfront costs. Social media companies like Meta can take advantage of their massive scale to drive the relative costs down and generate significant amounts of operating cash flow. This is reflected in the balance sheet as currently Meta has nearly 50 billion dollars of net cash, including the marketable securities.

Meta AI initiatives

The huge reserves of cash enable Meta to be one of the biggest AI spenders along with Microsoft, Alphabet and Amazon. The motivation behind Meta spending so much on AI should be seen from two perspectives: 1) strengthen their existing advertising products and 2) monetize on non-ad-related ventures.

The two most important pillars of Meta’s masterplan for AI are Llama LLM and Advantage+.

Llama LLM

Llama LLM is a family of language models developed by Meta. Llama models are currently one of the major language models out there in the market along with OpenAI's GPT and Google's Gemini—but with one key difference: all the Llama models are open-source.

Open-source models are publicly available, allowing anyone to use, modify, and distribute the software. Closed-source models, on the other hand, are often proprietary models, with their source code bases accessible only to the organization that developed them or those willing to pay for access.

Examples of Open-Source Models:

● GPT-2 and GPT-Neo

● BERT (Bidirectional Encoder Representations from Transformers)

● ELECTRA

● T5 (Text-to-Text Transfer Transformer)

● Llama 3

● Grok

● Mixtral

● DBRX

● Deepseek

Examples of Closed Models:

● GPT-3 & 4 by OpenAI

● Amazon Alexa’s Language Model

● IBM Watson

● Microsoft Visual Studio

● Tableau Software

● JetBrains IntelliJ IDEA

● Microsoft Azure Cognitive Services

● Google Cloud AI and Natural Language

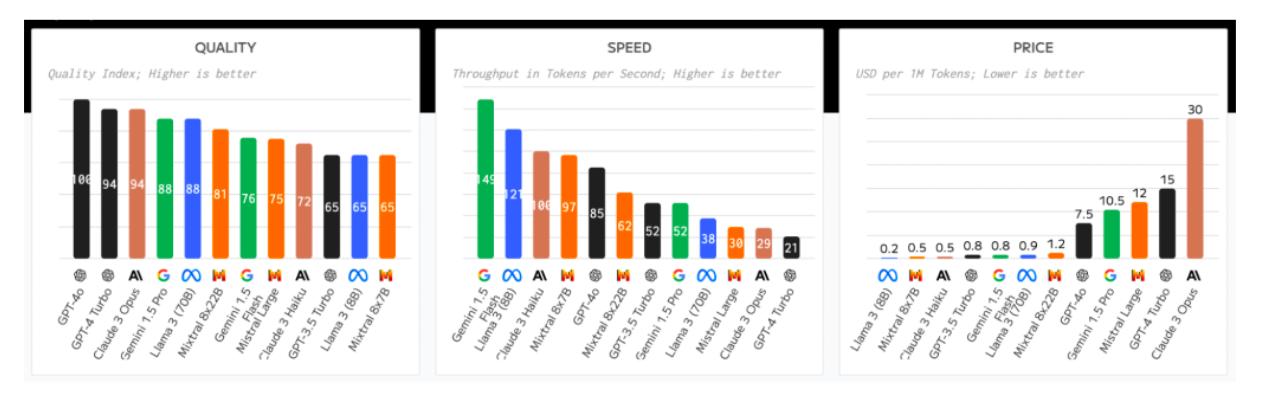

In terms of performance, the closed models are more sophisticated at this stage, however, the open-source large language models allow for more customization and have a higher potential for faster innovation.

Source: HatchworksAI

The emergence of DeepSeek, which is open-source by nature, presents a great opportunity for other open-source models to gain market traction with their affordability and high potential. Meta, having the most well-known open-source LLM, can benefit extensively in the long run.

In the coming months, Meta will release the latest version of Llama (Llama 4), which will be even more powerful and efficient. This continued innovation positions Meta at the forefront of AI development, enhancing its competitive edge in the industry.

Advantage+ and Andromeda

Advantage+ and Andromeda are a portfolio of tools, which assist advertisers and Meta in automating ad campaigns using AI. Meta introduced a suite of new generative AI tools for advertisers, including creative productivity tools for generating images and text. By offering tools to develop well-targeted campaigns, with higher quality images and text, Meta can charge advertisers higher fees, fueling the future revenue growth.

Threads and WhatsApp have a long monetization runaway

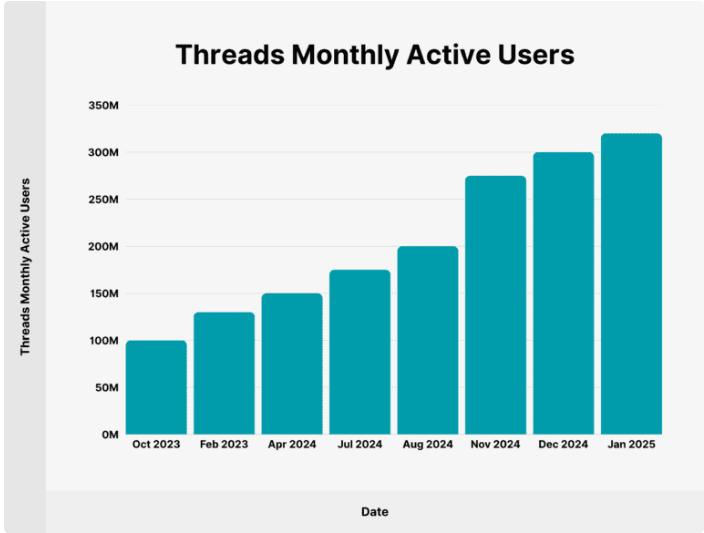

Source: Backlinko

Threads, the Meta answer to X (formerly Twitter), more than doubled its user base. At this moment. Threads has accumulated 320 million users, and this is still less than 10% penetration from the total number of users of all the Meta platforms, with the prospect of continuing to grow at high rates. Meta does not monetize Threads, but they are expected to do so in the coming years.

Unlike Threads, WhatsApp has already started to be monetized with Click-to-WhatsApp ads. However, lots of monetizing opportunities can emerger here, especially within WhatsApp Business.

Risks

Enormous Spending

Spending right now is the biggest concern for Meta investors. For 2025, the total cost of revenue and operating expenses will go up by over 20% and the capex will be 70% higher than what we saw in 2024. Also, judging from the tone of the management, the spending spree will not just be a thing of this year, but it may take a while - maybe several years.

Source: TradingKey, SEC Fillings

If we take into account the decelerating growth of less than 20% year-on-year, by the end of the year, Meta may actually see a decrease in EPS.

The excessive amount of spending can be also seen in the Reality Labs Revenue segment – the segment is losing tens of billions of dollars and the outlook for narrowing the losses seems unclear.

Source: SEC Fillings

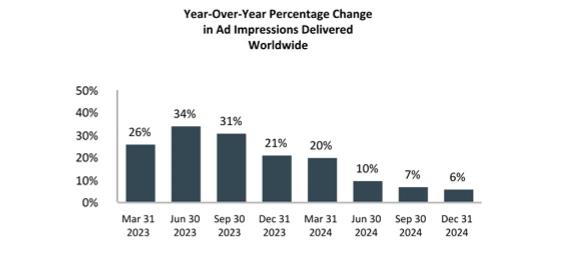

Cyclicality is Still Here

When it comes to growth, we should bear in mind that advertising is still a cyclical business. So far, the economy has been doing great, with recession being avoided. However, if we see a sudden economic slowdown, businesses will spend less on advertising, hence the growth will be lower. From the recent quarters' results, we can see a trend of growth normalization within the revenue line.

Source: SEC Fillings

Source: SEC Fillings

Other Risks

Lastly, there are always regulatory (data-breach) risks and competition risks present for companies with this business model.

Valuation

Meta is currently traded at 29x TTM Earnings. Apart from GOOGL, this is the second lowest among the Mag7 firms. However, with the uncertain prospects of near-term earnings growth in the coming year, the valuation suddenly does not look that attractive anymore. Thus, we believe Meta is quite fully priced at the moment, with not much upside potential in the near term.

Long-term, with the growth of AI, the opportunities remain abundant for the company. Any positive news with regards to Llama can be a potential positive surprise.