Can Earnings Season Be the Catalyst for U.S. Stocks?

TradingKey - Fears of persistent inflation, driven by strong employment data and Trump’s potential policies, have raised concerns that the Federal Reserve may scale back planned rate cuts. Combined with worries over high valuations and a potential stock market bubble, these factors have increased selling pressure on U.S. equities.

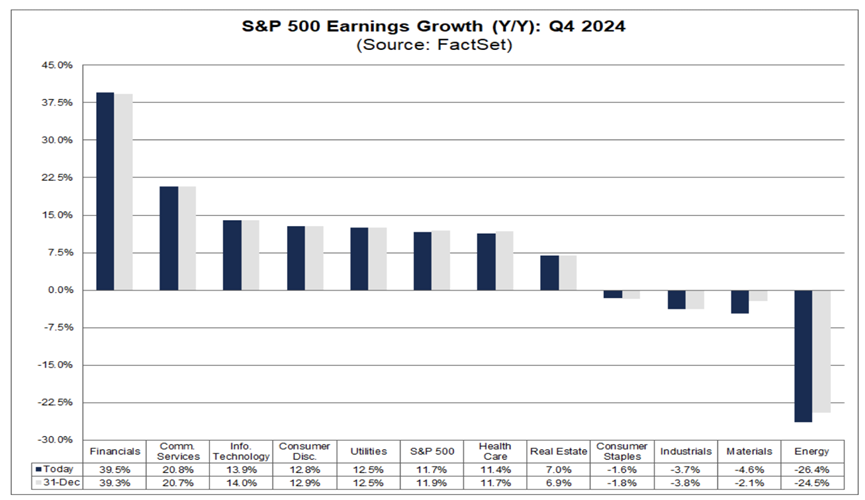

The Nasdaq Composite and S&P 500 have both dropped over 1% year-to-date. However, according to the latest FactSet earnings insights, the S&P 500 is on track to deliver its strongest quarterly earnings growth in three years.

The S&P 500 is currently projected to post earnings growth of 11.7% for Q4, which would represent the highest year-over-year growth rate since Q4 2021 (31.4%). Historically, the actual earnings growth rate has surpassed the estimates at the end of the quarter in 37 of the past 40 quarters. Based on the most conservative average historical improvement, the index is likely to report a year-over-year earnings growth rate of 14.1% for the fourth quarter.

This week, the Financials sector will take center stage as several major institutions, including Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Wells Fargo, are set to release their earnings. The Financials sector is expected to report the highest year-over-year earnings growth among all eleven sectors, with a projected growth rate of 39.5% for Q4.

Source: FactSet

Sean Ryan, VP and Associate Director for the banking and specialty finance sector at FactSet, pointed out that trends for banks will likely be mixed. Net interest margins (NIMs), loan growth, and deposit growth are expected to be positives, while noninterest income and the effects of higher long-term rates could be negatives for most banks.

Ryan added, “the most important new information is likely to be refreshed forward guidance on the earnings calls, which is likely to skew bullish based on late-fourth-quarter conference commentary, a steeper yield curve, and industry anticipation of a more favorable regulatory environment than has existed in several years.”

The Information Technology sector, the most attractive to investors, is anticipated to post the third-highest year-over-year earnings growth at 13.9%. However, it is projected to lead in revenue growth, with an increase of 11.1%. The Semiconductors & Semiconductor Equipment industry is the largest contributor to the sector’s earnings growth. Without this industry, the sector’s estimated earnings growth would drop to 6.1%.

Strong earnings remain the foundation for supporting the long-term value of U.S. stocks. Positive earnings data will likely bolster investor confidence. However, short-term risks remain. Jay Woods, global strategist at Freedom Capital Markets, said the coming weeks could be challenging as large-cap tech stocks, which have been key to supporting the market, are starting to weaken. He also noted that many S&P 500 stocks remain below their 200-day moving average, a key indicator of market strength.