JPMorgan Asset Management’s Outlook for 2025: Shifting Expectations

TradingKey - While 2024 has been a great year for investors, on the whole, there are some concerns about what lays ahead in 2025. On the back of two great years in US stock markets, there’s always the lurking feeling that a third year of positive gains isn’t on the cards.

The case for why is easy to see. There’s more uncertainty with a new president-elect Trump taking office in the US in January while China’s slowing economy also remains a threat to global growth.

JPMorgan Asset Management recently released its 2025 Investment Outlook and the firm sees a lot of political and geopolitical ructions shaping markets in the new year. Here are some key takeaways for investors.

Taxes + tariffs in 2025

With Trump taking office in early 2025, there comes with his administration the prospect of new fiscal stimulus. This will likely be in the form of the tax package he passed in his first administration – the Tax Cuts and Jobs Act (TCJA) – being fully extended beyond the end-2025 expiry.

All in, that should be supportive of both household spending and corporate earnings. However, while this presents a supportive backdrop for markets, there are two big risks on the horizon in 2025 that could upset this positive scenario playing out.

First off is the ongoing large budget deficits of the US government and how more stimulus from Trump’s administration could unsettle bond markets. What’s put in consumers’ pockets via tax cuts could easily be offset by higher mortgage and corporate borrowing rates. Secondly, any negative policies with regards to tariffs could end up denting consumer and business confidence.

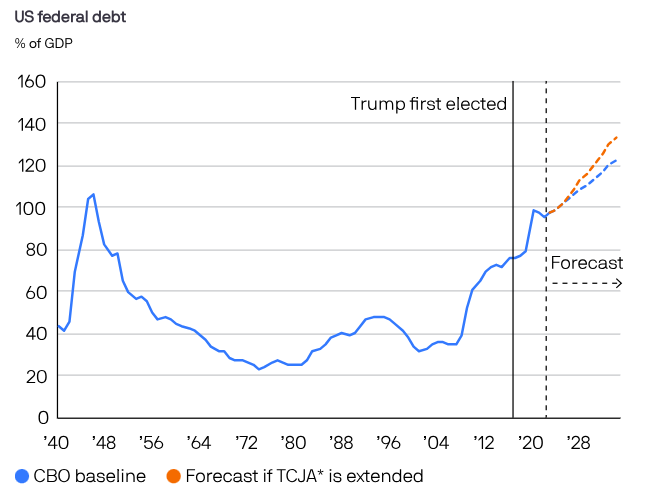

Trump is asking a lot of bond investors given the fiscal deficit is currently already set to stay in the region of 7% to 8% over the coming decade. Throw in the extension of the TCJA and that could bring it close to 9% by the early 2030s.

Meanwhile, there are projections for US federal debt could exceed a whopping 120% of US GDP by 2030. But with the extension of the TCJA, that could also be pushed higher.

Ever-rising government debt in the US could unsettle bond markets

Sources: BEA, CBO, US Treasury, JPMorgan Asset Management. Years shown are fiscal years and data as of 12 November 2024.

Risk of trade wars

Understanding how far Trump will go with his trade agenda is also an important factor for investors to consider. Both him and key members of his team – like former trade negotiator Robert Lighthizer – are ideologically predisposed to tariffs. They view free trade with more suspicion and see tariffs as an easy “win” in terms of raising revenue to fund tax cuts at home.

Yet Trump may run into the practical difficulties of imposing wide-ranging tariffs by executive order. While he can use executive orders to execute unilateral and targeted tariffs, the prospect of broad-based tariffs will require more congressional action and that will take time to get pushed through.

Recent years (post-pandemic) have shown politicians just how much US citizens dislike inflation and a potential 10% to 20% universal tariff on all imported goods will likely have an impact on US price pressures. It’s also no coincidence that the trade war, initiated under Trump’s first term in office, also brought about a dramatic decline in business investment in the US.

Therefore, it’s believed that other countries and regions will have the space to negotiate with the US with respect to tariffs.

How should investors think about 2025?

Overall, JPMorgan says there’s a large degree of uncertainty in markets when it comes to US domestic and foreign policy and how other nations will react to this.

While there is the American “exceptionalism” argument for why US stocks trade at a more expensive valuation than other regions, they believe that a forward price-to-earnings (PE) multiple of 22x (vs. 14x in Europe) means a lot of optimism is already priced in.

Thinking more broadly, investors should be mindful how they manage their equity allocations as the AI boom needs to progress from the “hype” phase into reality, where profits can be consistently generated.