The Death of UBER is “Slightly” Exaggerated

Summary

For Uber investors, 2024 was like a rollercoaster ride. In October, the stock was up 50% year-to-date, but in the last two months it went down nearly 30%. There are two main reasons for the dive. The first one is the positive development of Tesla and Waymo when it comes to autonomous vehicles and robotaxis. The second one has to do with the softer than expected business outlook with more tepid gross bookings growth on the platform. We believe the investor overestimated these two risks and punished UBER a bit too severely, sending the stock to an attractively valued territory. Currently the stock is traded at a 25% discount from its true potential value.

Source: TradingView

Overview

Company Profile

Uber is arguably the most successful company in the so-called “gig economy”. It is mainly engaged in the ride-hailing business (providing a platform that connects travelers and drivers, charging them a percentage-based commission per ride). It also does food delivery and freight forwarding. Uber was founded in 2009 and for these fifteen years of operations, it has made an enormous impact. Currently it operates in 70 countries and 10,000 cities globally, successfully disrupted the decade-long taxi industry and became a market share leader in the markets it operates in. Uber has an enormous brand value, just as much as the largest tech brands like Facebook, Instagram, Amazon, Google and Microsoft.

Business Lines

Ride-hailing, the main business, constitutes nearly 60% of the revenue. Uber controls a dominant market share of 75% in the USA (the rest 25% is held by Lyft). Uber is the market leader in most of the developed markets. There are other large players such as Didi in China, Grab and Gojek in Southeast Asia and Yandex in Russia, but they are mostly regional and unlikely to challenge Uber globally.

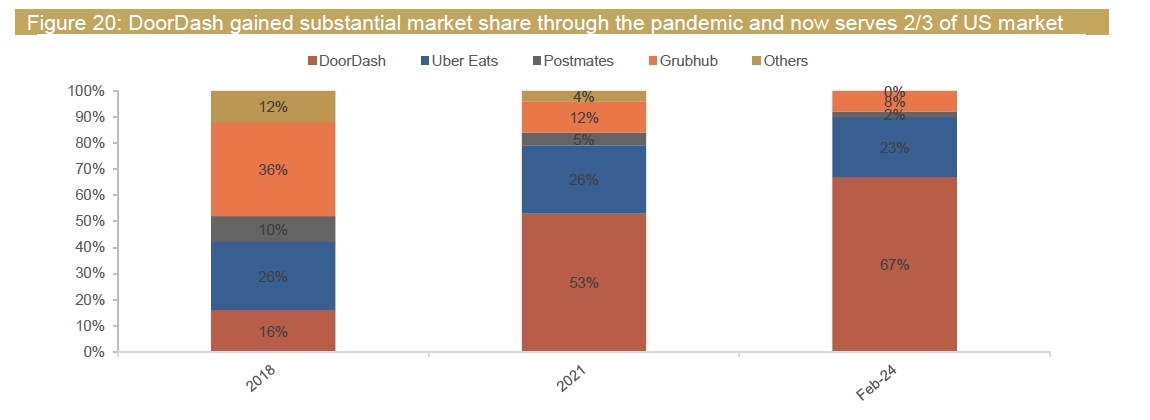

Food delivery is the second largest business, constituting roughly 30% of the revenue. UBER is the second largest player in the states with 23% market share (first is Doordash with 67%). Freight represents only 10% of the total revenue, thus we will not focus on it here.

Source: McKinsey & Company, Bloomberg

Source: Company Fillings, TradingKey

Defying the odds and the skepticism

Throughout its history, Uber path has always been a bumpy ride. Initially, there were many doubters in their ability to make profit. Uber was able to prove them wrong as their profitability is still improving with each quarter.

Source: Company Fillings, TradingKey

Uber also had plenty of legal battles with various stakeholders such as government authorities, taxi drivers and gig workers. Despite all this, Uber is still operationally sound and expanding healthily.

Currently, Uber is facing an existential threat from the rise of the robotaxis from Tesla and Waymo. The main narrative is that with the development of the automated vehicles, TSLA and GOOG (the owner of Waymo) can launch independent robotaxi companies and provide services for much lower prices than Uber and Lyft, simply because they do not need to pay riders, which will severely harm the business of the ride-hailing companies.

However, there are quite a lot of problems and unknowns with this thesis, and here’s a list of some of them:

1. The technology is at a nascent stage: Waymo just makes ~150,000 robotaxi rides per week vs 200 million Uber rides per week

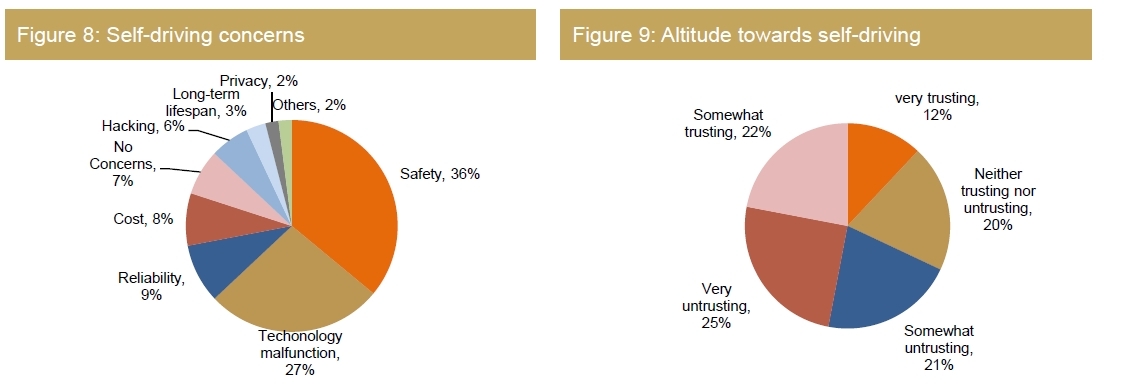

2. The overall public perception is still not very welcoming of the idea of autonomous driving. Safety is still a concern, and more safety tests should be carried out. Technology malfunction and lack of reliability when it comes to timing and mapping are also major worries.

Source: China Merchant Securities

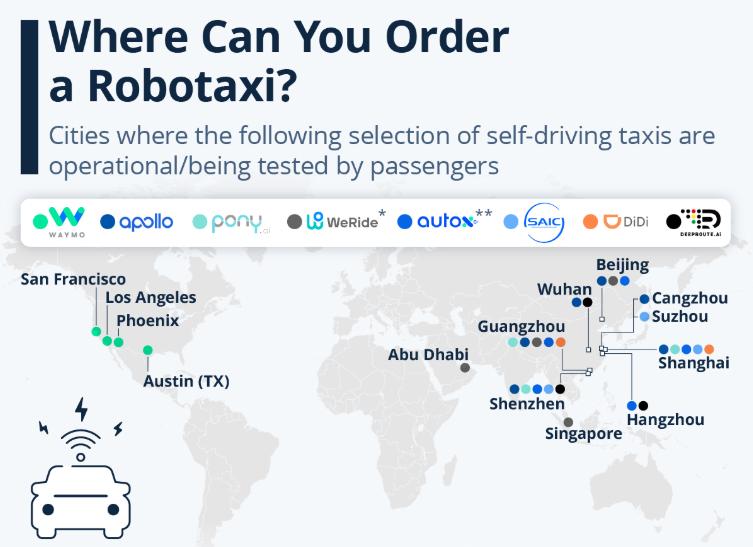

3. Overseas markets, apart from the US and some more developed countries, simply do not have the right road infrastructure for scaling such an initiative and suitable infrastructure should precede the development of vehicles

Source: Statista

4. Neither TSLA nor the other robotaxi startups have a production capacity to match the fleet of UBER

5. The autonomous vehicles’ hardware (sensors) and the related software are still quite expensive, and it will take time to become price competitive

6. UBER already partners with Waymo and other autonomous vehicles startups, thus instead of competition, this dynamic can turn out to be cooperative one simply because the robotaxi firms need Uber’s critical mass traffic and data. This puts Waymo in a situation where they need Uber more than Uber needs them

Uber from Financial Perspective

At this point, Uber is in a very sweet spot where it has moved from the stage of losing money to just becoming profitable. From now on, Uber will be able to utilize its economies of scale and improve their operating leverage, reaching higher absolute profits and better margins.

Source: appeconomyinsights.com

Unit Economics

In order to evaluate the growth, we need to see UBER from the perspective of several operating metrics:

Source: Company Fillings, TradingKey

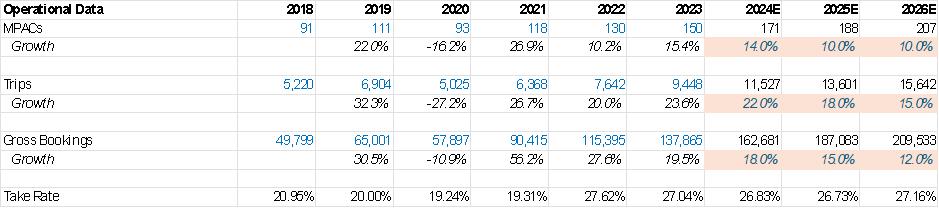

Monthly Active Platform Customers (MPAC) Growth

Source: Company Presentation

o MPACs are growing at low-teen y/y, decelerating to around ~10% y/y

o However, the growth path seems quite well-defined

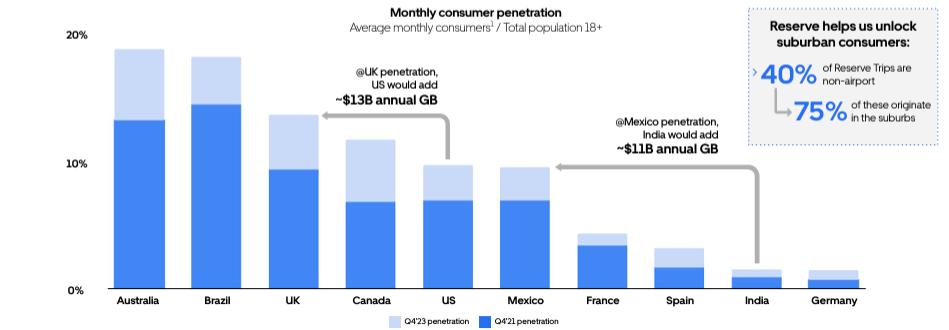

o Penetration is still not very high even in mature markets, as the US (10% of adult population)

o Lyft riders, for instance, grew 9% in the last quarter, but since they cover only the United States, the international exposure will definitely help Uber with registering high growth

o The situation overseas is even more favorable with much lower penetration rates in markets like France, Spain, India and Germany

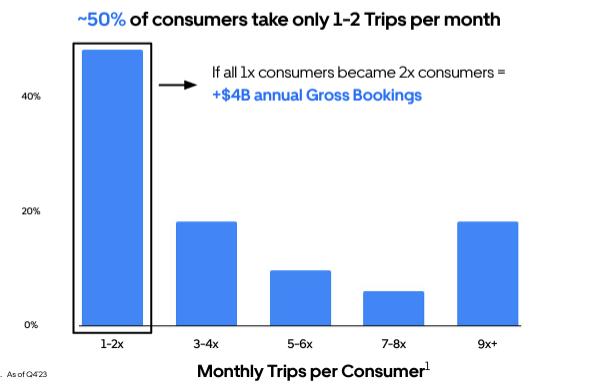

Trips Growth

o Trips are expected to grow at a faster rate than MPACs due to increased frequency of orders, as the more mature the users are, the more trips they will make

o Increase in order frequency with low single-digit y/y

Source: Company Presentation

Gross Bookings

o Many investors reacted negatively when Uber announced slightly softer gross bookings in Q3, however the primary focus should be on take rates and monetization, as Uber is no longer in a hyper-growth stage

o We do expect Gross Bookings to grow at a lower rate than Trips due to the expansion outside of North America towards markets with lower purchasing power

Take rate (monetization)

o Take rate will remain stable for the near future

o On one side, we have tailwinds such as a higher portion of ride-hailing from the total revenue (generally higher take rate)

o On the other hand, we have headwind, as the proportion of non-USA/Canada revenue will increase with time

Financial Metrics

As the gross bookings are expected to grow in teens and the take rate remains rather stable, revenue will also grow at a similar rate to the gross bookings.

In terms of operating expenses, we can see major improvements with the economies of scale, and we see this trend continuing in the coming years - especially from the marketing side, where the solid brand moat will allow decelerated spending on incentives and promotions.

Source: Company Fillings, TradingKey

Valuation

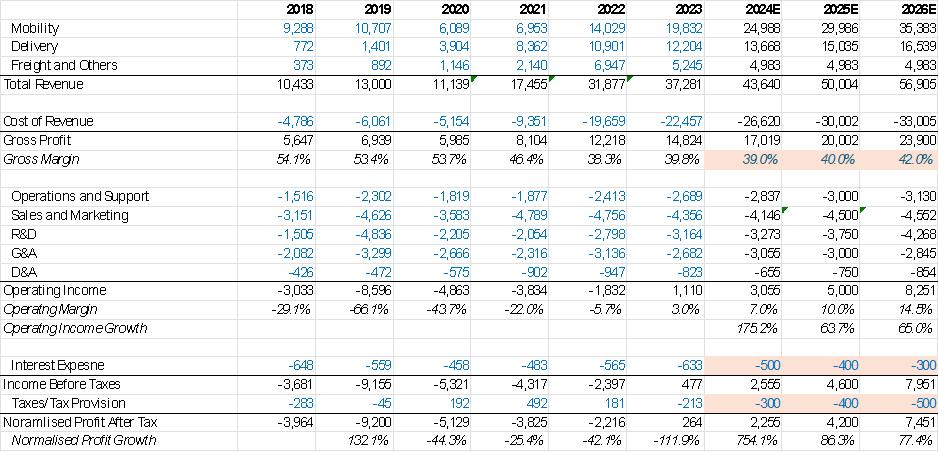

Valuing Uber can be a bit different from how we value other tech names. Even though Uber is profitable on a GAAP basis, a huge chunk of its profit comes from activities not fully linked to their operations. Items such as gain/loss on equity securities do not reflect the capabilities of the company and they are quite lumpy in nature. Thus, we use normalized profit after tax (NPAT), without including the non-operating income.

Source: Company Fillings

Uber is traded 57x 2024E NPAT, which seems quite generous. However, the NPAT is expected to grow 70-80% per year up to 2026. Due to its early stage of profitability and dominant market share, we believe Uber deserves a high valuation of around 70x 2024E NPAT, at its target stock price of USD75.00-85.00 gives the stock a 25%+ upside.

Source: Company Fillings, TradingKey