Advanced Micro Devices and the Battle for the Silver Medal for Processors

Source: TradingView

Summary

Advanced Micro Devices (AMD) has its strong sides such as a fast-growing data center business, a wide range of products at reasonable prices, plus a very capable management. However, the gap between AMD and NVDA is very obvious, and we do not expect this to change in the foreseeable future. AMD can still successfully compete with Intel for market share. We do not see much upside at this moment, but if big tech suddenly decides to be more conservative on AI spending, AMD will be the beneficiary.

Industry Overview

AMD is among the largest semiconductor companies worldwide. AMD designs and sells microprocessors (CPUs and GPUs) and other computing solutions for data centers, personal computers, gaming consoles and other devices.

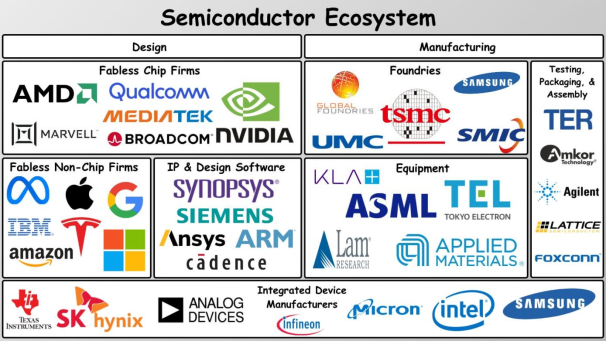

Companies in the semiconductor ecosystem can be classified into three categories:

- Fabless Firms - companies that design semiconductors but don’t manufacture them; AMD and Nvidia are such firms.

- Manufacturers (foundries) - companies that only manufacture, based on the designs provided by fabless firms. The most prominent example is TSMC.

- Integrated Manufacturers – companies that do the design and manufacturing in-house. Intel is the largest integrated chip manufacturer.

Source: Felicis Ventures

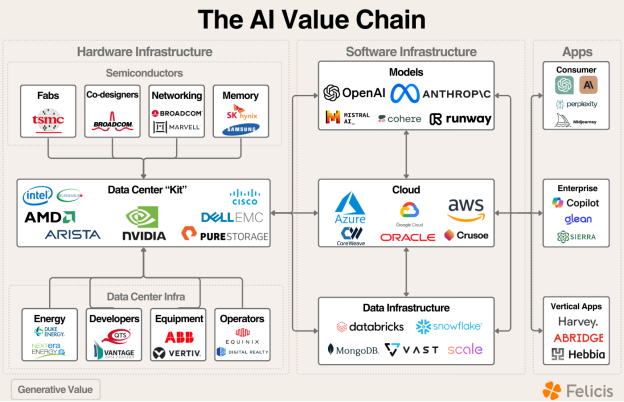

As the chip is basically the “brain”, every type of electronic device needs a chip. There are chips for phones, computers, laptops, game consoles, and data centers.

In the past few years, data center processors have been the hottest trend in the industry — largely because of the AI mania. Big tech firms like Google, Microsoft, Meta and Amazon need to develop their AI capabilities, thus they have to invest in enormous amount of computational power in the form of data centers. As data center chips are more powerful and sophisticated, not many chip companies are able to come up with such products. This is why companies like Nvidia are growing at such an enormous pace. The supply of high-quality powerful chips simply cannot match the demand.

Currently, the data center market is absolutely dominated by Nvidia with roughly 80% market share, while AMD and Intel have approximately 10% each. This segment is still expected to grow exponentially in the coming years driven mostly by capex from the big tech firms.

Source: Felicis Ventures

In terms of non-data center CPUs, the situation is quite different. The growth is more cyclical, highly correlated with the consumption of electronic goods such as phones, personal computers and gaming consoles, thus the opportunities here are not as lucrative as in the data center segment. Hence the CAGR expected in the coming years is much more modest, projected to be in the low teens. There, Intel has been dominating in the last few decades, but AMD is catching up.

Will AMD be able to repeat the success of NVDA?

Source: TradingView

AMD bulls often present the company as an alternative to NVDA that is poised to repeat its success. As AMD is clearly lagging NVDA stock performance since the start of the AI Mania, AMD bulls expect AMD to catch up, especially in the data center segment. There are several good reasons why this will not happen in the observable future.

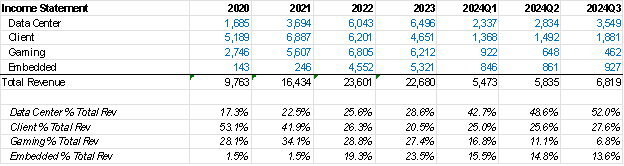

First of all, the revenue constitution of both firms is not the same. Data centers represent a bit over 50% for AMD vs 85% for NVDA revenue. This makes AMD significantly less exposed to the secular trend of AI and more exposed to the cyclical nature of the other types of chips.

Source: TradingKey, Company Financials

Second, comparing the flagship products of both Nvidia and AMD, we can conclude that Nvidia products are more powerful. AMD chips on average can perform at 80% the capacity of Nvidia products.

Finally, Nvidia’s CUDA is superior to AMD’s ROCm. CUDA is NVDA’s proprietary computing platform which is used by developers to create software utilizing NVDA chips capabilities. CUDA can only be used on NVDA products and considering that NVDA holds dominant market share, the moat for NVDA is really strong. AMD software platform ROCm may be more flexible but less powerful than CUDA. Overall, Nvidia was more successful in integrating software and hardware and we can’t say the same thing about AMD. Hence, the market sees NVDA as an AI firm with equally strong software and hardware, while AMD is seen as a hardware company only.

One big advantage for AMD is that their products have lower prices, delivering more value per dollar. AMD also supports a wider range of CPU-GPU-Networking products. AMD products may actually provide better ROI but that may not be enough to justify big scalers (Microsoft, Amazon, Meta, Alphabet) to switch to AMD on a large scale.

All of the big scalers have very healthy balance sheets, solidified with a great amount of cash reserves. Not just that, their strong cash flow generation from their traditional business can constantly support their cash reserves. As long as these firms have endless amounts of cash to spend, they will continue to prefer the premium products of NVDA since they are rather price-insensitive.

Furthermore, they expect a need for more investment in AI. Even if the ROI is currently unclear and companies may not need this level of computing power right away, this is perfectly okay. The investment outlook that we should think of is fifteen years and above. That is why big clients do not mind spending extra for extra computing power.

Google’s CEO Sundar Pichai: “The risk of under-investing is higher than the risk of over-investing.”

Competition with INTC

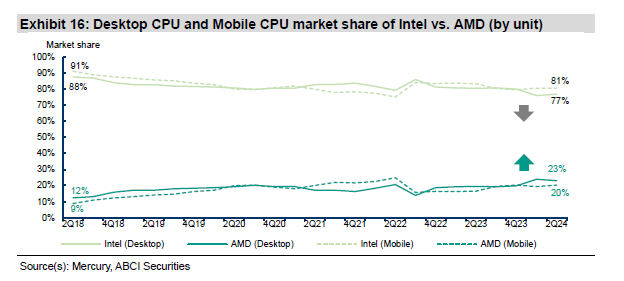

AMD’s investment case should revolve more around its competition with INTC. In terms of non-Data Center business, AMD has long been in competition with Intel and Intel has always been more dominant. However recently AMD successfully took advantage of Intel’s weaknesses and stole market share, both in terms of revenue and volume.

Even though INTC still has a dominant market share, and this won’t change soon, its financial troubles and lack of innovation can present a good opportunity for AMD to steal market share.

AMD is fabless and cooperates with TSMC for its product development, unlike INTC which is predominantly integrated. With the help of TSMC’s superior capabilities, AMD can produce superior products.

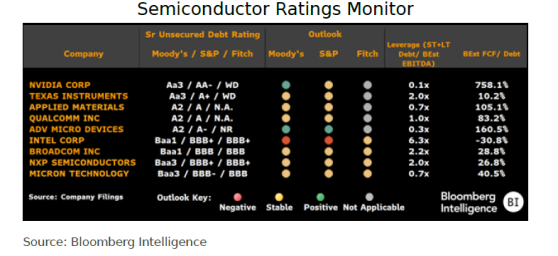

AMD is also in a better financial position. AMD has a strong balance sheet with 0.3x Debt over EBITDA and FCF in the positive area. In contrast, INTC has the highest Debt/EBITDA among their semiconductor peers, as well as negative FCF. This shows how uncertain the situation is with INTC, and while AMD may have enough resources to invest in upgraded products and R&D, it will be very difficult for INTC to match this.

Last but not least, AMD management has proven to the industry that it can make a big difference. Lisa Su, the current CEO, took the position in 2014 – a time when AMD was far behind INTC in terms of technology and with a huge pile of debt. In ten years, Su was able to make a complete turnaround, and this can be seen from the magnificent stock rally in the last decade.

Source: TradingView

Valuation and Assumptions

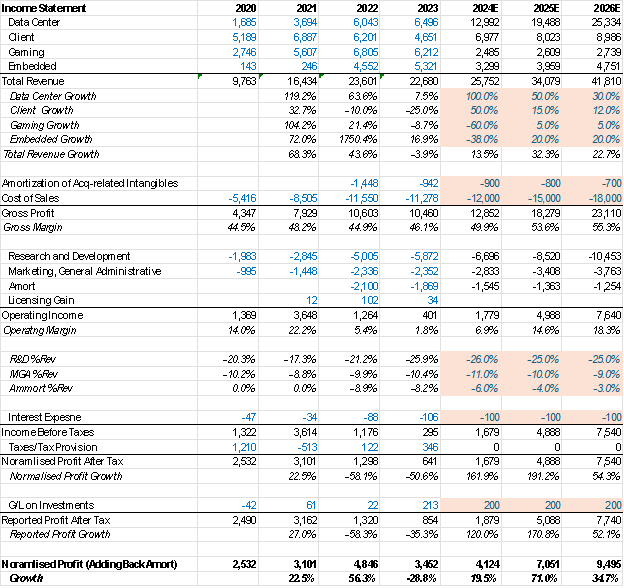

Average revenue growth is expected to be within the 20%-30% range, mostly driven by the Data Center segment but lower than NVDA’s growth which is expected to be 50% CAGR. This is because NVDA has higher exposure to Data Centers. Also, there will be a drag from the gaming, PC, and mobile CPU markets which will grow at a much slower pace than data centers.

Gross margins, currently standing at around 50% are set to improve due to the favorable revenue mix of data centers and embedded chips. However, we won’t see a drastic increase due to the launch of the newer products. Opex efficiencies will come primarily from SG&A expenses, while R&D expenses need to remain high due to catching up with Nvidia technologically. Furthermore, because AMD has to keep its prices relatively low compared to Nvidia’s products, we won’t see margins going towards 70% as we’ve seen with Jansen Huang’s firm.

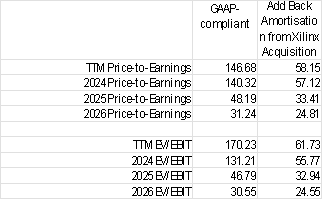

For the valuation, we use the earnings and add back the amortization expenses from the Xilinx acquisition.

Currently, AMD is traded at 57 times the adjusted earnings, a similar level to NVDA. However, at this stage, NVDA is the superior one. NVDA has higher earnings growth, better margins and exposure to a mega-trend rather than a cyclical business. Therefore, AMD is currently correctly valued with not much upside.

Source: TradingKey, Company Financials

Source: TradingKey, Company Financials