Palantir Technologies (PLTR): Reaching Speculative Heights

By Petar Petrov

Source: TradingView

Summary

Palantir is a company with a superior product, operating in an industry with high secular growth, giving the stock an extremely high valuation. However, the market appears to only consider a very optimistic scenario where nothing could go wrong, ignoring the competitive landscape and the potential complications from its controversial business.

Company Overview

Stellar stock performance

Palantir Technologies (PLTR) is among the hottest stocks in 2024. Due to its superior technology, it is considered as one of the purest AI stocks on the market. Since the beginning of the year, the company’s stock has gone up by an astonishing 290% (the second biggest jump among the S&P500 stocks this year), far outpacing S&P500 (26% YTD) and even NVDA (182% YTD).

The factors behind PLTR rally are 1) the inclusion of the stock into S&P500 and potentially Nasdaq, improving the level of ownership by institutional investors and 2) beating the quarterly estimates and 3) acquiring more government contracts

Business description

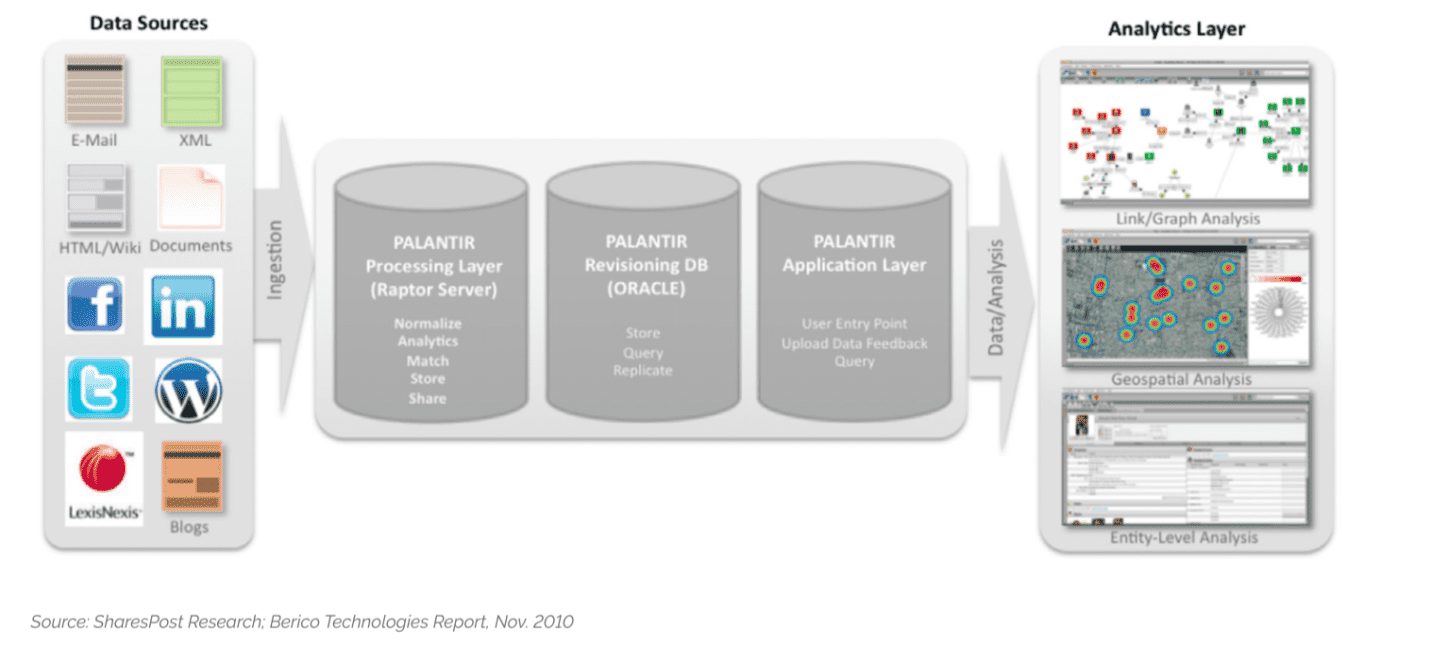

As much as PLTR is a hot stock, there is also a lot of mystery surrounding the company, mostly due to its close connection with the US military. In brief, Palantir is an enterprise software company that develops and sells data analytics solutions to government agencies and large corporations. What PLTR products mainly do is to integrate and organize data from a huge variety of sources and provide customers with various tools to analyze the data and reach conclusions regarding their operations.

The company provides a number of products with the two main ones being Gotham for government clients and Foundry for commercial customers. Gotham has been widely used in the US army, the US Health Department and the Immigration authorities, while Foundry is implemented in various industries such as finance, oil & gas and technology.

Controversial government business

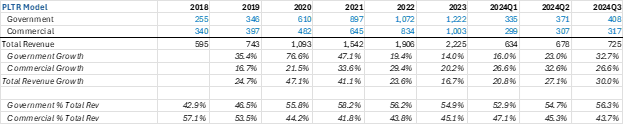

Source: TradingKey, Company Financials

PLTR can be considered part of the enterprise software industry, thus having a similar business as Microsoft, Oracle, SAP and Salesforce, combining software-as-a-service and project-based revenue model.

However, what makes PLTR different from the names above is the strong government/political background they have. More than half of the revenue is generated from government clients, as PLTR has very deep connections with the government. In the first five years of its operations (2004-2009), PLTR only had government agencies as clients. Its first non-government client was JP Morgan in 2009. Palantir even received seed capital from the CIA in its early days.

The fact that they collaborate with the state authorities makes Palantir different from other competitors, as others tend to be more cautious working on government projects due to political reasons. This makes PLTR quite comfortable operating in this segment.

What’s more, the founder and the CEO, Alex Karp has rather extreme views supporting the United States and its Western allies, claiming he is not interested in doing business with countries that are not close allies to them. Unsurprisingly, over 70% of the revenue comes from the US and the UK. Palantir capabilities have been utilized in the battlegrounds of Iraq, Afghanistan and currently Ukraine. Another controversial project of Palantir is the implementation of technology that helps with the deportation of illegal immigrants.

Working on government projects has One big advantage and one major disadvantage. The advantage is that projects will have a low correlation with the economic cycle. For instance, during economic downtime, the other more commercial-focused competitors will experience a drop-in business activity, but Palantir may end up being quite resilient due to the government spending not being affected by the economy much. On the other hand, government projects can be more lumpy than commercial ones, making revenue flow for Palantir less predictable.

Competitive commercial business

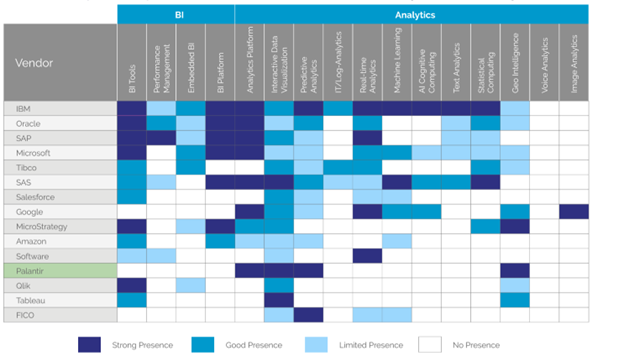

On the commercial client front, the situation is quite different. PLTR has already expressed their desire to acquire more business with commercial players, but the competition there is quite intense, and we can classify it as follows:

Type | Example | Definition |

Large Vendors | Microsoft, Oracle, IBM, SAP | - Provide wide range of product packages - Can easily up-sell to customers with their wide range of solutions, improving client stickiness - Due to the economies of scale, they can provide more competitive prices, raising the barriers of entry for smaller players |

In-house Software Tools | Google, Facebook | - Large companies that possess unlimited access to data collected from their daily business operations - Having in-house tools to operate with the data - Can also use external vendors for certain projects and tasks |

Smaller Specialized Players | Palantir, Tableau | - Rather new compared to large vendors - Product line is not as extensive, but they are more specialized - Often having superior capabilities due to their specialization - Pricing may not be as attractive as the one from larger players |

As part of the smaller specialized group of players, Palantir arguably has one of the most advanced capabilities according to many industry experts. They are particularly good in the areas of predictive analytics and geo intelligence.

Another huge advantage of PLTR is the relatively low percentage of marketing expenses that is typical for the rest of the industry. The reliance on government projects makes it not compulsory for them to splurge on customer acquisition, as their business grows quite organically towards other USG agencies and overseas governments. In recent quarters they have spent around 30% of the revenue on marketing (less than 25% if we exclude share-based compensation) vs other SaaS competitors that may spend up to 50%.

Source: TradingKey, Company Financials

Even if PLTR products are technologically superior, and their government business may be more resilient, there is a high chance this is not what the customers may prioritize. PLTR is a more niche firm operating with very high complexity projects, however oftentimes the projects customers give to data analytics companies do not need the complexity PLTR can handle. Thus, competitors with capabilities not as superior as Palantir can outcompete them either with better pricing or a wider range of product offerings.

Additionally, the large number of companies operating in this field may create irrational competition leading to ASP trending down and margin suppression.

Investment Thesis

Source: TradingKey, Company Financials

Source: TradingKey, Refinitv

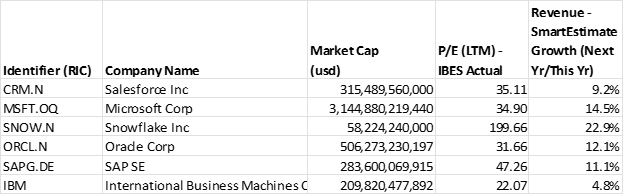

With TTM P/E Ratio of 308x, I believe PLTR is in a quite overvalued territory. The multiple is far above anything we see among the direct competitors.

Why is the market so bullish?

Firstly, this is a high growth industry. Big data analytics firms are expected to grow with a CAGR of 25-30% in the next five years. Secondly, the product is of an extremely high quality, proven by its previous implementation in various complex government tasks. Thirdly, they have the advantageous cost structure and the lack of need to spend a lot on marketing.

Judging from the points above, Palantir will be able to maintain a growth around the industry level or slightly above and the margins will continue to expand as the operational leverage will take place and the portion of share-based compensation will diminish. Thus, I expect the net income to triple in the coming two years.

All these points represent a rather blue-sky scenario for Palantir, and it still feels not enough to justify this enormous multiple.

What are the risks?

In fact, Palantir operates in a very crowded industry, and it has yet to prove that the quality of their product can successfully compete with the big established players on the market, especially if these players are able to up-sell their customers with their advantageous prices and wide range of products. Furthermore, even if the revenue from government agencies can provide a protection against economic downturn, this can come with other types of risks including harmed reputation and unpredictability from government side.

A valuation of 70-100x LTM Earnings will be more suitable for PLTR valuing it at around 20.00 USD per share.