Netflix: Cash cow in industry where no one else can be profitable, but the share price is not attractive

Profile

Netflix, Inc. provides entertainment services. It offers TV series, documentaries, feature films, and games across various genres and languages. The company also provides members the ability to receive streaming content through a host of internet-connected devices, including TVs, digital video players, TV set-top boxes, and mobile devices. It has operations in approximately 190 countries. The company was incorporated in 1997 and is headquartered in Los Gatos, California.

Overview

In 2024,NFLX is having a great year as a stock with 89% return year-to-date, far outpacing the S&P500(27.31% YTD). This was not the case a few years ago, when due to increased competition, NFLX lost subscribers for the first time and made the stock drop 75% from October 2021 to May 2022.

Source: TradingView

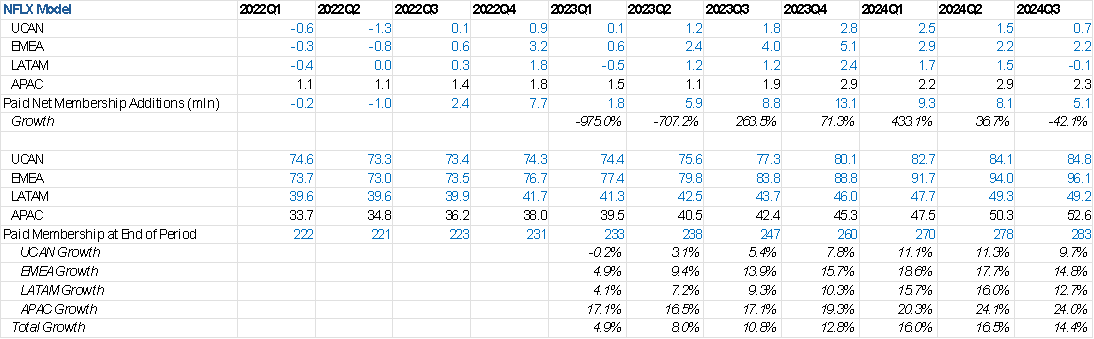

Currently Netflix seems stronger than ever. One of the most decisive actions the company did to improve its situation is to crack down password sharing in 2023. This forced users who use others’ accounts to subscribe separately. This measure had an obvious effect on its paid membership additions.

Source: Company Financials

What do investors love about NFLX this year?

- Revenue growth accelerated

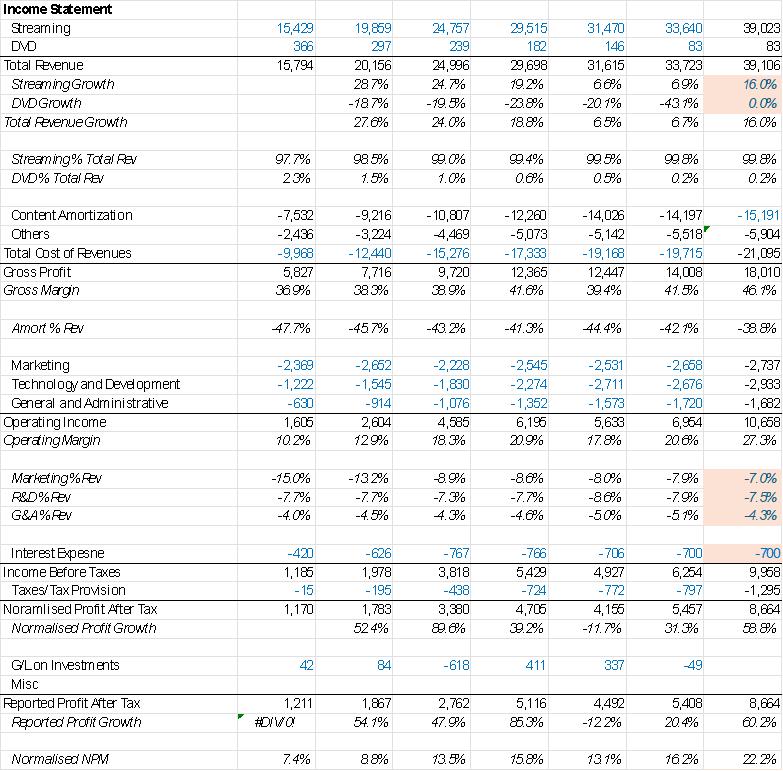

YoY revenue growth in 2022 and 2023 was 6.5% and 6.7%. So far this year, NFLX is demonstrating 15-16% growth from 2023 and this is expected to continue for Q4. The revenue acceleration is mainly driven by growth in subscribers and the subs mainly come from the password-sharing crackdown that took place one year ago.

- Impressive growth in margins

The operating margin of Netflix was just 10-13% prior to COVID-19. It reached 21% in 2023 and now is revolving around 27-28%. This is very clear evidence of the scalability of the streaming business, as operating costs of running such business will be similar regardless of users being 5mln or 500mln.

- Ramping up the ad-tier business ; no contradiction between subscription and engagement in ads.

Ad revenue is still not a significant part, but this will change in the coming years. Netflix ad tier members grew 35% QoQ in 2024Q3 from a small base and the ad revenue will double in 2024. Basic ad plan accounted for 50% of new subscriptions in the respective countries.

Many investors were worried that subscribers will react negatively to the ads, but this is a good chance for NFLX to provide cheaper plans and further fuel the subs growth. Also, in the last earnings call, the management noted they have not observed lower levels of engagement among ad-tier users vs ad-free users.

- Optimistic guidance for 2024 and 2025

Netflix is expected to finish 2024 with 14%-15% YoY with raised operating margin forecast of 27%. The management seemed quite comfortable with the business as they also forecasted 11%-13% revenue growth for 2025 with an absolute value in the range of 43-44USDbn, with 28% OPM.

- No price increase announced as expected

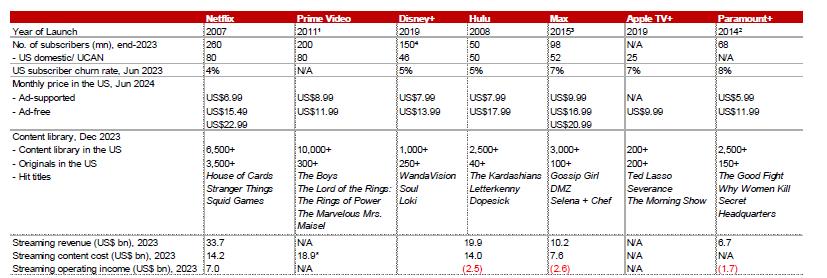

NFLX still has room for price increases as the ad-supported plans are among the lowest and the ad-free plans are not significantly overpriced vs peers.

Source: Digital TV Research, Company Data, Statista

- High moat---originally produced content

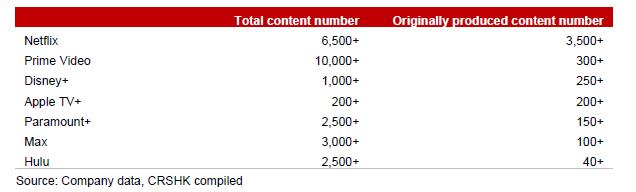

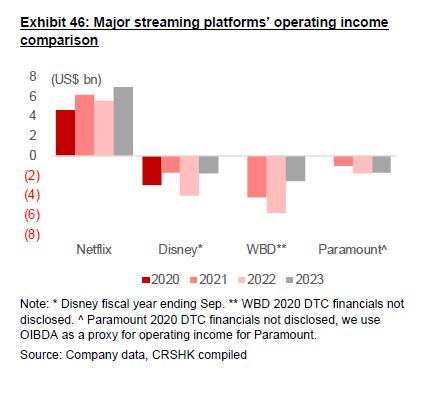

Netflix spending on content is assigned as an outflow from CFO and the gradual amortization is expensed in the P&L as a cost of revenue. Netflix has the largest amount of original content and the second largest amount of content (only behind Prime). The original shows are the main selling point that makes viewers subscribe. And due the fact that NFLX is way more profitable than its peers, the latter are often forced to sell their content to Netflix in order to raise cash, which shows how powerful the company is versus its competitors.

Assumptions

Growth will come primarily from adding subscribers. Even with one quarter left, 14-15% growth for the full 2024 is rather certain. However, I expect lower growth in 2025 and onwards. The effect of the password-sharing crackdown is going away. But in contrast, the cheaper ad-supported plans will keep the subscriber growth at around 10%.

ASP was flat in 2024, and this has to do with lack of big releases in terms of content. However, there will be some big releases soon and this can be a good reason for the management to increase prices next year. However, the effect will be rather small as the expansion of ad-supported plans will prevent the ASP going significantly up.

Netflix margins are rather easily expandable due to the scalability of the business model. Content amortization is stable, expecting to grow with 7% (7% is the CAGR of growth of content assets in the balance sheet).

For margins, 2024 was more of an exception. Marketing and content costs were lower due to the Hollywood filmmakers’ strike and not much new content. 2025 and 2026 will not see such dramatic margin expansion as the 1) Content and amortizing costs will go up; 2) Marketing as a percentage revenue will ramp up to 2023 levels; 3) More investments would be needed in establishing the ad business infrastructure.

However long term we expect margins to grow even further as the advertising revenue becomes a more significant driver. For instance, the operating margin of META, as a purely ad-revenue business, is nearly 40%.

Valuation

It is not easy to value NFLX in the context of its peers, as the biggest competitors are not standalone companies but part of a larger businesses (Disney, Amazon, Apple).

PE TTM | 50.78 |

PE 2024 | 45.38 |

PE 2025 | 38.39 |

PE 2026 | 31.86 |

NFLX is currently traded at around 51x TTM earnings, 45x 2024E earnings and 38x 2025E earnings. The valuation seems quite generous, especially if we compare it to Meta. Even though META and NFLX are not from the same industry, they are both in a similar situation where they dominate their respective industries. Meta is currently traded at around 30x TTM earnings, while historically it has been in the range of 25-30x. In such a scenario, NFLX should cost around 630-680 USD per share.

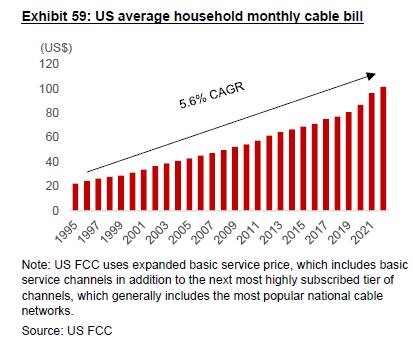

However, if Netflix continues with its successful content strategy and successfully rolls out the ad business, there will be a long runaway for profitability and price increases in the future, despite the fact that the developed markets (Europe and North America) are quite mature. Price increases may come from 1) Households in the majority own several subscriptions and if Netflix continues to provide value with its content, households may consider unsubscribing from the competitive platforms and stick with Netflix; 2) The average monthly cable bill for US households has been growing 5.6% on average implying that subscribers have high willingness to accept increases in their cable bill.

Furthermore, margins will expand as the business transitions towards more advertising, as advertising generally is a high margin industry.

Conclusion

It won’t be an exaggeration if we say that NFLX has the highest quality content assets. Based on these content assets, along with smart pricing policies, NFLX can sustain its growth for years to come. Margins are also easily scalable. Currently NFLX is generously valued, so there is not a huge upside potential. However, long term the prospects for the company are abundant.