[IN-DEPTH ANALYSIS] Australia: Will a Hawkish Central Bank Boost the AUD?

Executive Summary

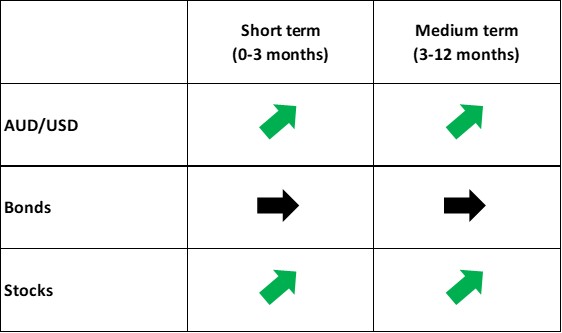

The strength of the Australian dollar (AUD) is influenced by both domestic and external factors. On the domestic front, the hawkish stance of the Reserve Bank of Australia (RBA), rising commodity prices and China’s gradual economic recovery will provide support for the AUD. Externally, the USD Index is expected to rise in the short term before declining later. All in all, in the short term (0-3 months), we anticipate the AUD’s gains against non-US currencies will outpace the USD Index, leading to a modest appreciation of AUD/USD. Over the medium term (3-12 months), a weakening US dollar will further bolster AUD/USD.

* Investors can directly or indirectly invest in the foreign exchange market, bond market and stock market through passive funds (such as ETFs), active funds, financial derivatives (like futures, options, and swaps), CFDs and spread betting.

1. Macroeconomics

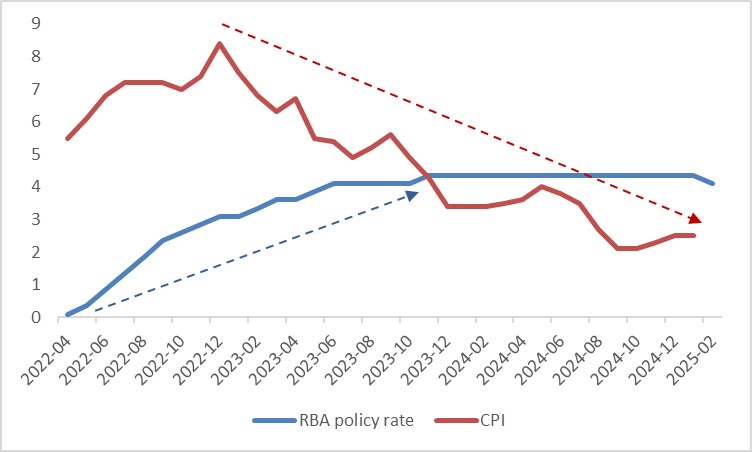

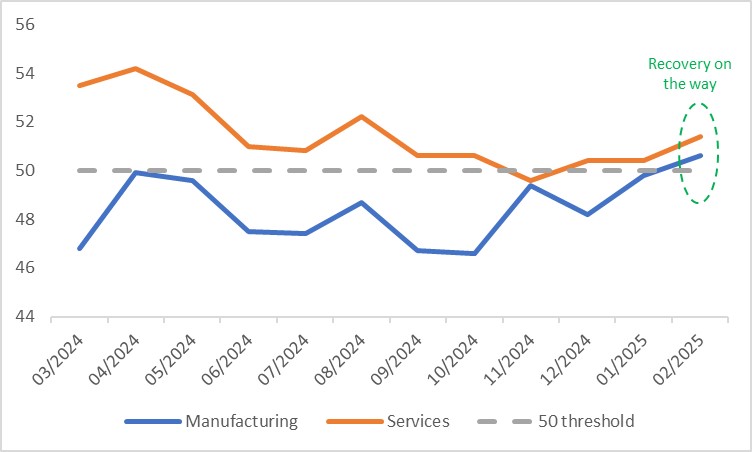

Between May 2022 and November 2023, the RBA successfully completed an interest rate hiking cycle, curbing inflation while avoiding an economic crisis and maintaining a low unemployment rate (Figure 1.1). Although Australia’s economic growth slowed significantly in 2024, high-frequency data suggest a recovery is underway. The Manufacturing PMI rebounded from 47.8 in January 2025 to above the 50 threshold. Over the past year, except for November 2024, the Services PMI consistently remained above 50 (Figure 1.2). The Westpac Consumer Confidence Index turned positive in February after being negative previously.

Figure 1.1: RBA policy rate vs. CPI (%)

Source: Refinitiv, Tradingkey.com

Figure 1.2: Australia PMI

Source: Refinitiv, Tradingkey.com

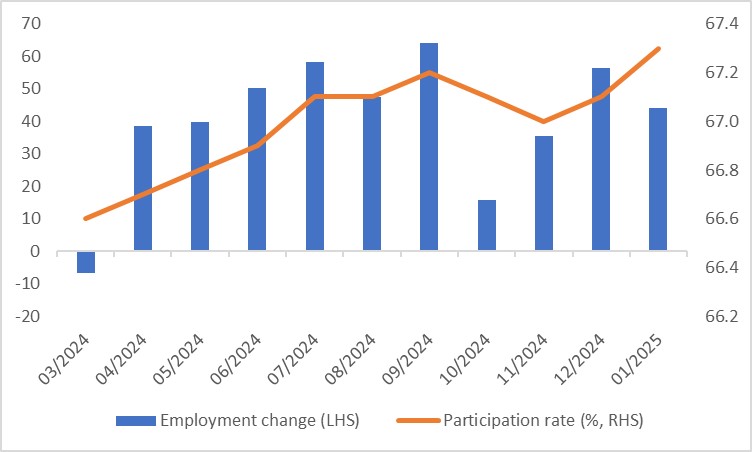

In the labour market, January 2025 saw 44,000 new jobs added, surpassing the consensus estimate of 19,400 and marking the tenth consecutive month of job growth. This lifted the participation rate from 67.1% in December 2024 to 67.3% in January 2025 (Figure 1.3). While the unemployment rate has edged up recently, it remains below its historical average, signalling a tight labour market.

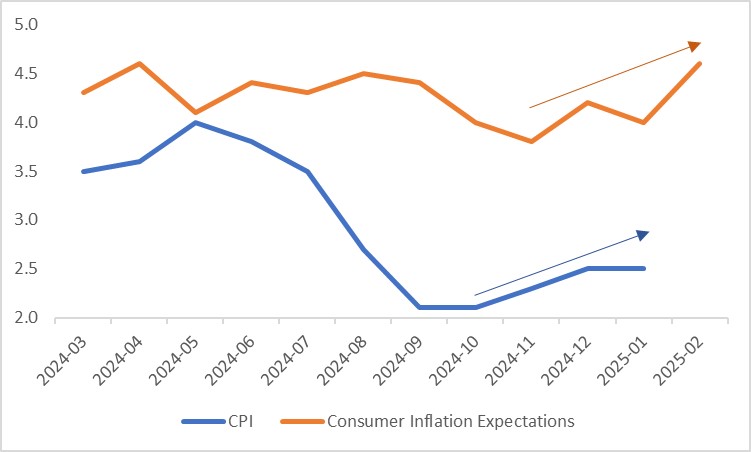

On inflation, the fourth quarter of last year recorded a Trimmed Mean CPI increase of 3.2% year-on-year. Though this has declined since late 2023, it still exceeds the RBA’s 2%-3% target range. January’s CPI rose 2.5% year-on-year, marking three consecutive months of increases since October 2024. With a tight labour market, inflationary pressures are likely to persist. The Melbourne Institute’s Consumer Inflation Expectation rose to 4.6% in February from 4% in January, reinforcing concerns about reflation (Figure 1.4).

Given the economic recovery, tight labour market and rising inflation, following the RBA’s latest 25bp rate cut in February, we believe further rate cuts before the second half of this year are unlikely. Even then, only one additional cut is expected in H2 2025.

Figure 1.3: Australian employment change vs. participation rate

Source: Refinitiv, Tradingkey.com

Figure 1.4: CPI vs. Consumer Inflation Expectations (%)

Source: Refinitiv, Tradingkey.com

2. Exchange Rate (AUD/USD)

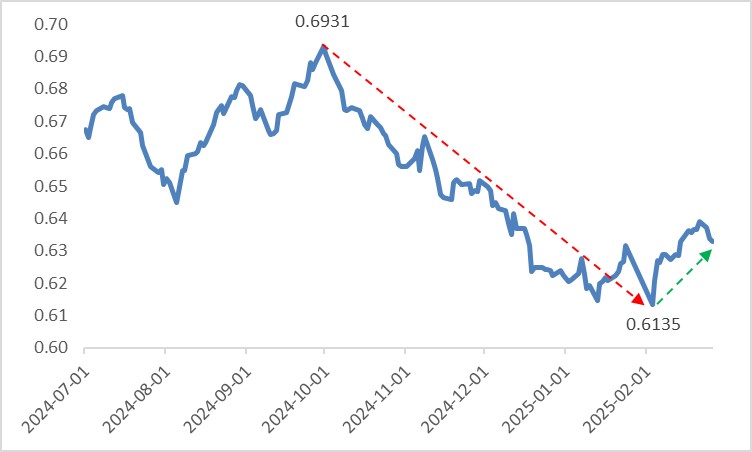

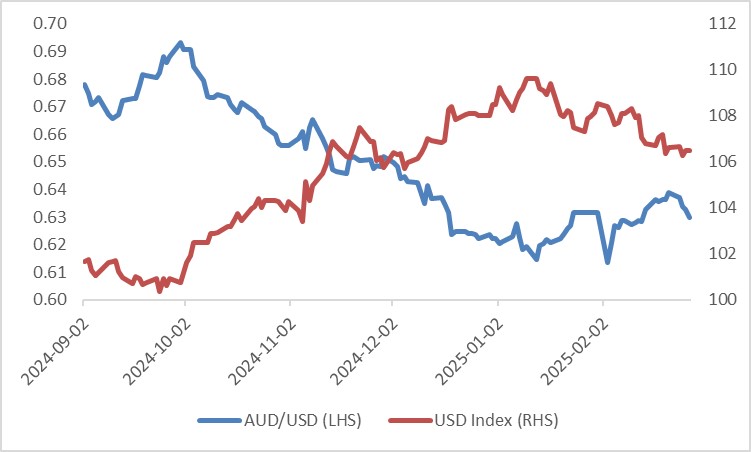

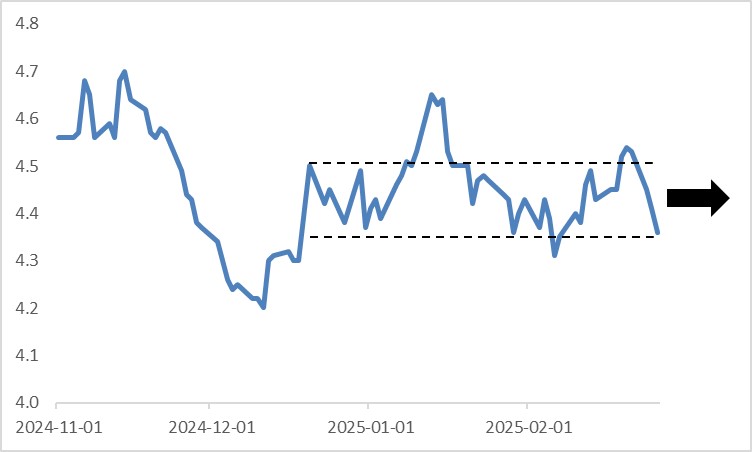

After a sharp decline from 0.6931 on 30 September last year, AUD/USD bottomed out at 0.6135 on 3 February this year and began to rebound (Figure 2.1). This shift was driven mainly by external factors—namely, the USD Index—rather than Australia’s domestic economic conditions (Figure 2.2).

Looking ahead, the AUD’s performance will hinge on both domestic and external dynamics. Domestically, inflation moderated in 2024, prompting the RBA to cut rates by 25bp to 4.1% on 18 February. Despite the cut, the RBA governor’s hawkish remarks at the press conference—highlighting a tight labour market and upside inflation risks—suggest this move does not signal further easing. This hawkish stance will support the AUD. Additionally, rising commodity prices and China’s economic recovery will bolster the AUD through export channels (Figure 2.3).

Externally, in the short term (0-3 months), the USD Index is expected to rise due to the “Trump Trade” and the Fed pausing rate cuts. Over the medium term (3-12 months), a fading “Trump Trade” and renewed Fed easing will cause the USD Index to peak and retreat.

Combining these factors, we expect AUD/USD to rise modestly in the short term, as AUD gains against non-US currencies outpace the USD Index. In the medium term, a weakening US dollar will drive further AUD/USD appreciation.

Figure 2.1: AUD/USD

Source: Refinitiv, Tradingkey.com

Figure 2.2: Strong inverse relationship between AUD/USD and the USD Index since September highlights that the primary driver of AUD movements has been the US dollar

Source: Refinitiv, Tradingkey.com

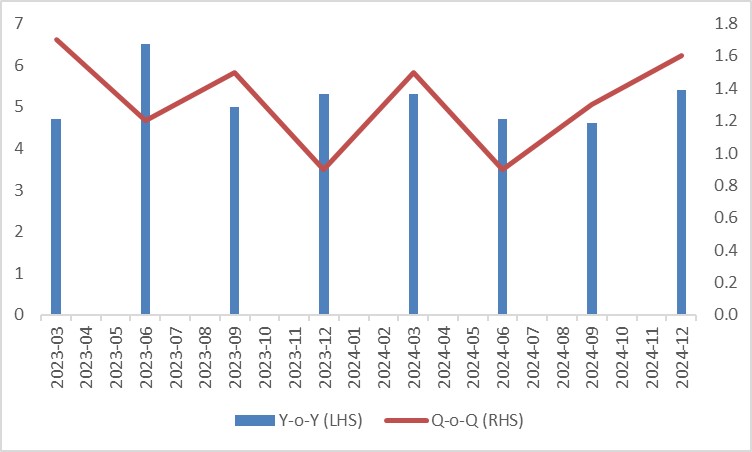

Figure 2.3: China real GDP growth (%)

Source: Refinitiv, Tradingkey.com

3. Bonds

Since December last year, Australian government bond yields have fluctuated within a range. We expect this pattern to persist, driven by opposing forces. On one hand, rising inflation, a tight labour market and the RBA’s shift from dovish to hawkish provide upward pressure on yields. On the other hand, expectations of a global economic slowdown—particularly due to Trump’s tariff policies impacting global trade—will exert downward pressure. These counteracting forces will keep yields range-bound, limiting significant upward or downward movements (Figure 3).

Figure 3: Australian 10Y government bond yields (%)

Source: Refinitiv, Tradingkey.com

4. Stocks

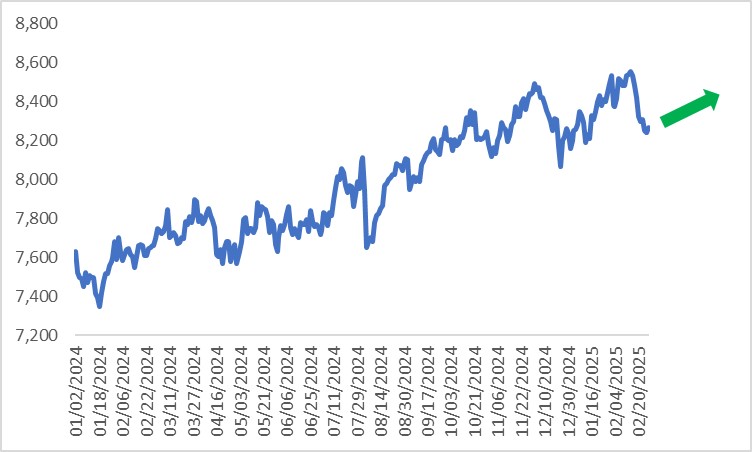

Over the past year, the Australian stock market has exhibited a strong upward trend (Figure 4). Looking forward, two factors remain supportive. First, high-frequency data underscore the resilience of the Australian economy, with its recovery now well-established, benefiting listed companies’ revenues and profits. Second, China’s gradual economic rebound supports commodity exports, favouring resource-heavy sectors. However, elevated valuations and a slow rate-cut cycle will cap significant gains. Thus, we expect the Australian stock market to see moderate growth in the short to medium term (within one year).

Figure 4: S&P/ASX 200

Source: Refinitiv, Tradingkey.com