India: A Country That Has Already Missed the Boat

Executive summary

Based on our summary table below, we believe that Indian stocks still present investment opportunities in the short to medium term. However, given that the Indian macro economy appears to “have missed the boat” for manufacturing-led development, holding these stocks for the long term—particularly beyond a decade—may not be a prudent investment strategy.

1. Background and long-term outlook

After World War II, India adopted the economic model of the former Soviet Union. Influenced by a centrally planned economy and plagued by bureaucratic inefficiency and corruption, India's economic growth during this period was sluggish. The situation worsened in 1991 with the disintegration of the Soviet Union, which was India's largest trading partner at the time. This led to a significant drop in exports. Compounding the problem were the effects of the Gulf War, soaring international oil prices, and a sharp increase in the cost of energy imports, all of which pushed India's economy into crisis.

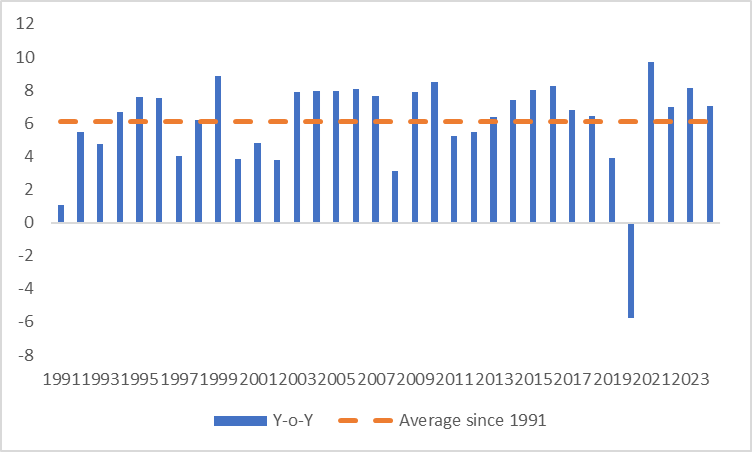

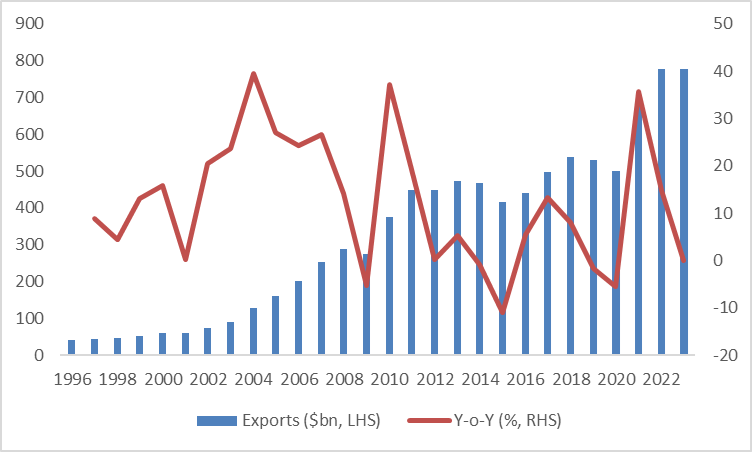

Fortunately, assistance came from the International Monetary Fund (IMF). Alongside providing financial aid, the IMF required India to implement comprehensive reforms in line with the "Washington Consensus". These reforms marked the beginning of India's transition to a market economy. Leveraging inherent advantages such as low labour costs, a large pool of technical talent, and widespread English proficiency, India achieved remarkable growth. Since the 1990s, the country's average annual real GDP growth rate has reached 6.1%, while its annual export growth rate in US dollar terms has climbed to an impressive 12.3% (Figures 1.1 and 1.2).

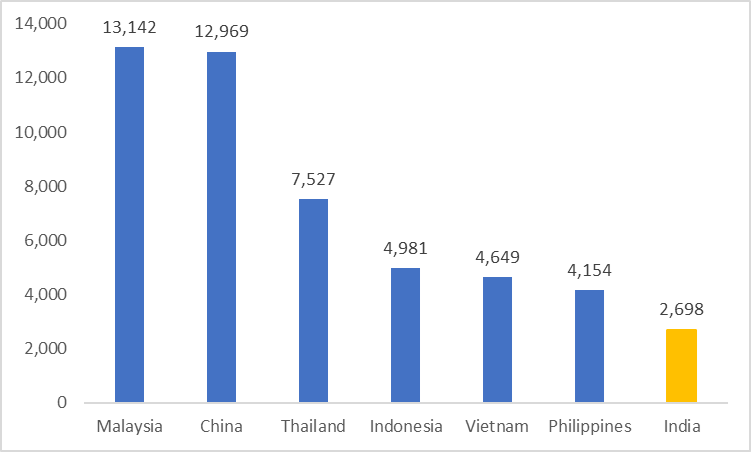

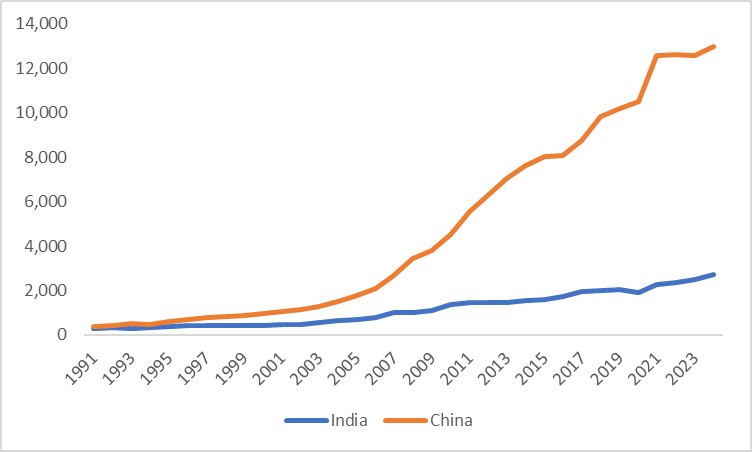

Despite decades of rapid growth, India's GDP per capita remains significantly lower than that of China and ASEAN countries (Figure 1.3). Since its economic reforms in 1978, China has risen to middle-income status, largely driven by a robust manufacturing sector and substantial productivity improvements (Figure 1.4). This raises an important question: can India replicate China’s success?

Unfortunately, the likelihood appears slim. India seems to “have missed the boat” for manufacturing-led development. The rise of protectionism globally poses challenges to export-driven strategies, and labour-intensive industries are increasingly being replaced by automation technologies like robots and AI. Moreover, India continues to face deep-rooted social and structural challenges, including a weak industrial base, pervasive corruption exacerbated by its license-driven regulatory system, and the enduring caste system. These factors collectively hinder India's long-term economic development.

Figure 1.1: India's real GDP growth (%)

Source: IMF, Tradingkey.com

Figure 1.2: Indian exports

Source: Refinitiv, Tradingkey.com

Figure 1.3: GDP per capita (USD)

Source: IMF, Tradingkey.com

Figure 1.4: GDP per capita (India vs. China), USD

Source: IMF, Tradingkey.com

2. Short- and medium-term macroeconomics

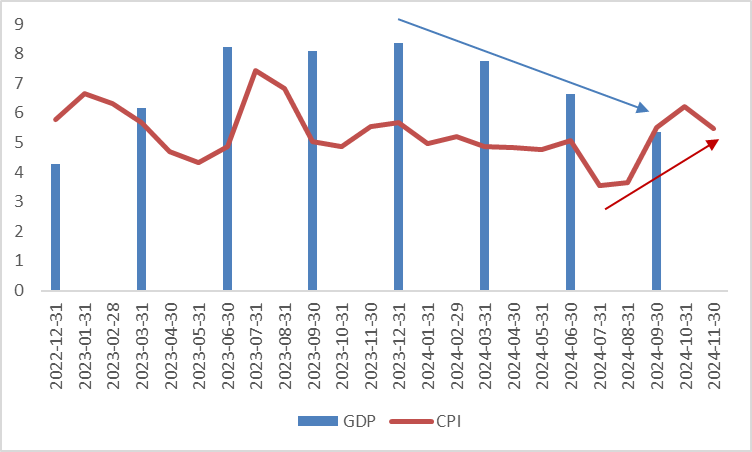

Since FY2022, India has enjoyed a “Goldilocks economy” characterized by high growth and low inflation. However, recent developments suggest signs of economic weakness, primarily driven by softening urban consumption. On the external demand front, the potential imposition of high tariffs by the Trump administration could trigger a global slowdown in 2025, impacting India’s goods exports and restraining corporate capital expenditure. On the inflation side, headline CPI has been rising since August of last year, driven by elevated food prices.

Amid the dual pressures of slowing growth and rising inflation (Figure 2), the Reserve Bank of India (RBI) kept the policy rate unchanged on 6 December 2024, while reducing the reserve requirement ratio by 50bp. Looking ahead, if inflation is brought under control, we anticipate that the RBI may implement significant interest rate cuts in 2025.

Figure 2: Indian real GDP growth and CPI (%)

Source: Refinitiv, Tradingkey.com

3. Stocks

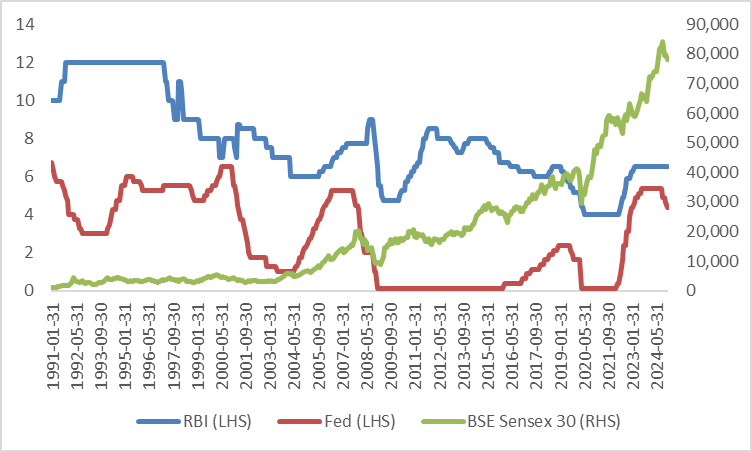

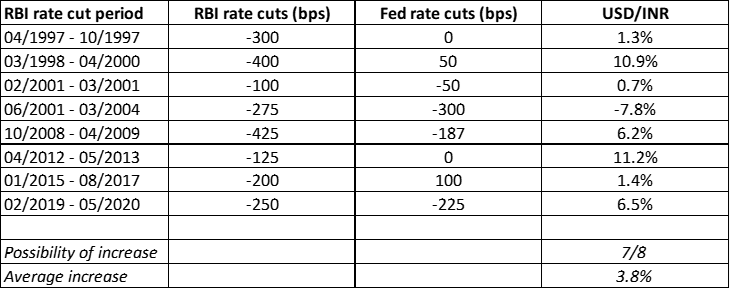

While many economists and analysts have extensively studied the impact of the Fed's rate cuts on US financial markets, fewer have delved deeply into the RBI’s effects on Indian markets. This article takes a historical perspective, examining the impact of eight rate-cut cycles since India embraced a market economy in 1991 on its stock, bond, and foreign exchange markets. It also forecasts the potential influence of rate cuts in 2025.

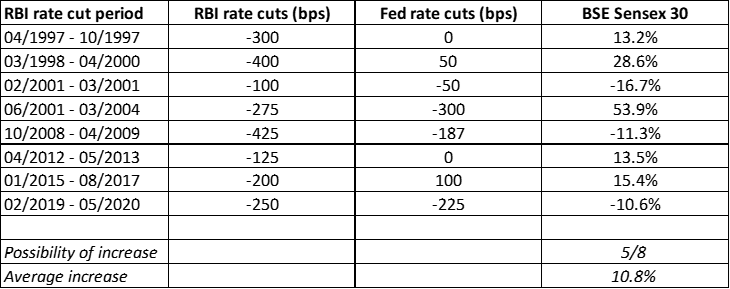

Historically, during these eight rate-cut cycles, the Indian stock market posted gains in five, with an average return of 10.8% (Figures 3.1 and 3.2). This aligns with economic principles, as rate cuts typically improve financial conditions, benefiting equity markets.

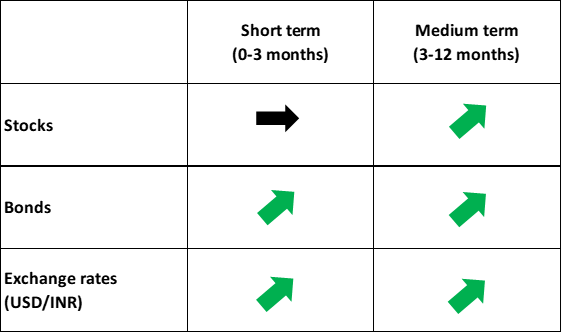

Looking ahead, in the short term, due to challenges from low growth and high inflation, we assign a neutral rating to the Indian stock market. However, in the medium term, the anticipated rate-cut cycle in 2025 is expected to support a new phase of stock market gains. It is worth noting that while overseas investors may earn profits in the Indian stock market, the depreciation of the Indian rupee could diminish their returns when converted to dollars (a detailed analysis of the exchange rate is provided in Section 5). Nevertheless, we believe that the potential gains from the Indian stock market are likely to far exceed the impact of rupee depreciation, enabling overseas investors to achieve more substantial US dollar returns.

A fitting metaphor often used in financial markets compares the macroeconomy to a person and the stock market to a dog being led by that person. In the short term, the dog (stock market) may occasionally wander ahead or lag behind. Yet in the long run, the dog (stock market) inevitably follows the person’s (macroeconomy) direction. Similarly, over the ultra-long term (beyond 10 years), as India’s macroeconomy appears to “have missed the boat”, the potential for high returns on Indian stocks is likely to diminish.

Figure 3.1: Policy rates and BSE Sensex 30

Source: Refinitiv, Tradingkey.com

Figure 3.2: BSE Sensex 30 performance during RBI rate cut periods

Source: Refinitiv, Tradingkey.com

4. Bonds

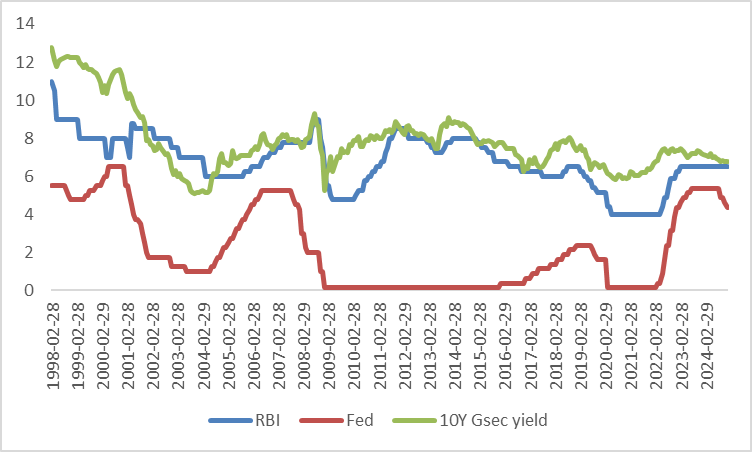

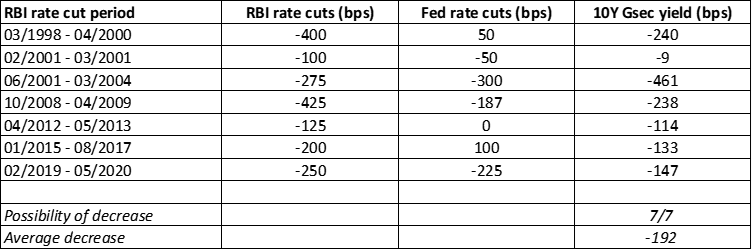

Due to limited data availability, our analysis of the bond market focuses on the past seven interest rate cut cycles. Figure 4.1 illustrates the strong correlation between the yield on India's 10-year government securities (Gsecs) and the RBI’s policy rate. Since 1998, every interest rate cut cycle has resulted in a decline in Gsec yields (Figure 4.2). Looking ahead to 2025, we are optimistic about Indian bonds amid expectations of a new round of interest rate cuts. Any price corrections should be viewed as attractive buying opportunities.

Figure 4.1: Policy rates and 10-year Indian Gsec yield (%)

Source: Refinitiv, Tradingkey.com

Figure 4.2: 10-year Indian government bond yield during RBI rate cut periods (%)

Source: Refinitiv, Tradingkey.com

5. Exchange rates

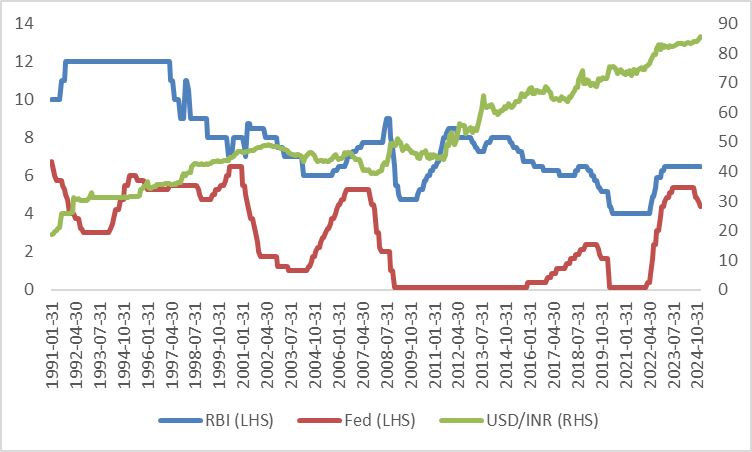

Historically, the Indian rupee has depreciated in seven out of the past eight rate-cut cycles. The only exception occurred during the period from June 2001 to March 2004, when the rupee appreciated due to the Fed cutting rates more aggressively than the RBI (Figures 5.1 and 5.2).

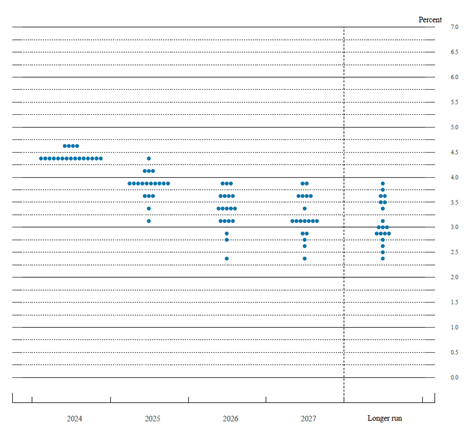

Looking ahead to 2025, the Fed’s dot plot indicates two rate cuts of 25bp each (Figure 5.3), while we anticipate the RBI to implement 3-4 rate cuts. This divergence in monetary policy suggests that the rupee is likely to face continued depreciation this year.

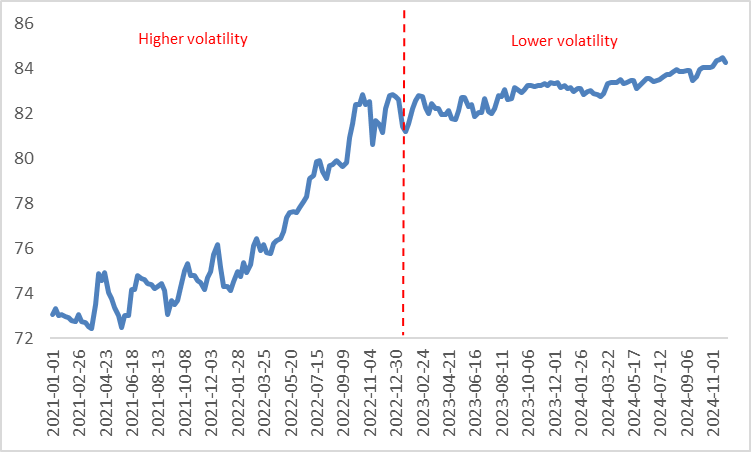

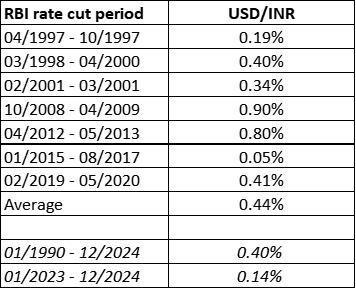

Excluding the June 2001 rate cut cycle, the USD/INR exchange rate has historically appreciated at an average rate of 0.44% per month during the remaining seven cycles—higher than the long-term average of 0.4% since 1991. However, since the beginning of 2023, the monthly average appreciation of the USD/INR has slowed to 0.14%, primarily due to the RBI's intervention in the foreign exchange market (Figures 5.4 and 5.5).

While the RBI is expected to maintain its intervention efforts in 2025, the divergence in rate cuts between the RBI and the Fed leads us to believe that the rupee’s monthly depreciation rate will exceed 0.14% this year.

Figure 5.1: Policy rates and USD/INR

Source: Refinitiv, Tradingkey.com

Figure 5.2: USD/INR during RBI rate cut periods

Source: Refinitiv, Tradingkey.com

Figure 5.3: Fed’s dot plot (December 2024)

Source: Fed, Tradingkey.com

Figure 5.4: USD/INR

Source: Refinitiv, Tradingkey.com

Figure 5.5: USD/INR (monthly average changes)

Source: Refinitiv, Tradingkey.com