US January PCE Commentary: PCE Growth Poised to Ease—Implications for Financial Markets

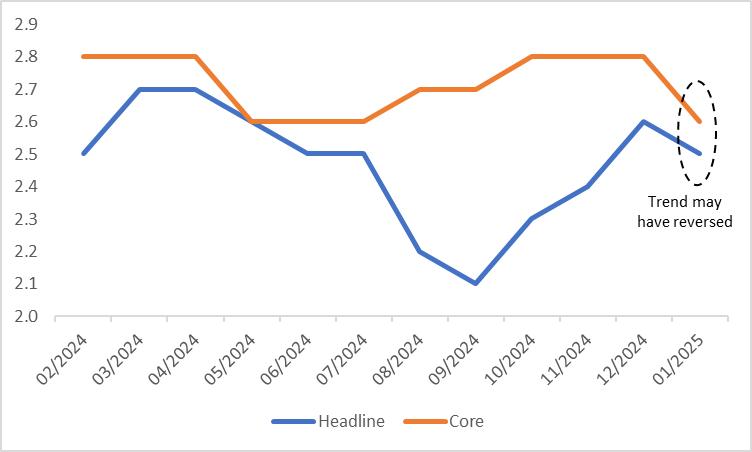

On 28 February 2025, the United States released the Personal Consumption Expenditures (PCE) data for January. The data revealed that the Headline PCE and Core PCE rose year-on-year by 2.5% and 2.6%, respectively, aligning with market consensus expectations but falling below December’s figures of 2.6% and 2.8% (Figure 1). Breaking down the month-on-month PCE increase of 0.3%, goods prices surged by 0.5%, serving as the primary driver of January’s PCE rise. This uptick was largely due to higher motor vehicle and gasoline prices. However, a decline in healthcare costs limited the increase in service prices to just 0.2%, helping to curb elevated inflation.

Figure 1: Headline and Core PCE in January (%)

Source: Refinitiv, Tradingkey.com

From a trend perspective, Headline PCE bottomed out at 2.1% in September 2024, marking three consecutive months of year-on-year increases since October. Meanwhile, Core PCE remained steady at 2.8% from October to December, a slight uptick from September’s 2.7% (Figure 2). Thus, the decline in January’s PCE offers a positive signal. Looking ahead, we anticipate that the inflation rebound seen since the fourth quarter of last year has ended and PCE is expected to gradually trend toward the Federal Reserve’s 2% target. This is primarily driven by weakening domestic demand in the U.S., which is slowing economic growth and suppressing inflation from the demand side.

Figure 2: PCE (%)

Source: Refinitiv, Tradingkey.com

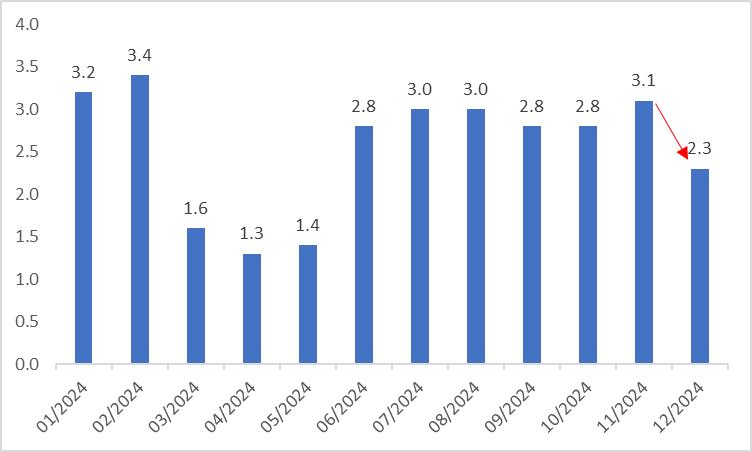

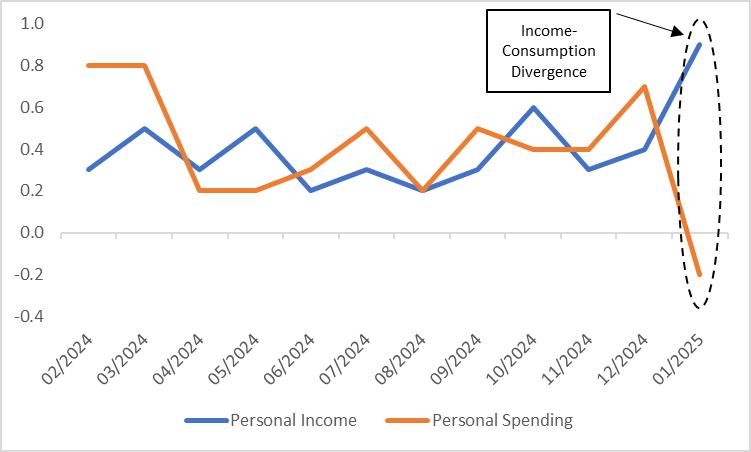

On the broader economic front, the annualized GDP growth rate for the fourth quarter of 2024 was 2.3%, falling short of the consensus estimate of 2.6% (Figure 3). High-frequency data also points to softening momentum, with the recently released consumer confidence index showing a decline. According to related data released on February 28, despite personal income rising by a robust 0.9% month-on-month in January—well above the market’s 0.3% expectation and December’s 0.4%—personal spending dropped by 0.2% (Figure 4). This suggests that, despite income gains, consumers are reining in spending amid uncertainties about the economic outlook.

Figure 3: US GDP growth (annualized, %)

Source: Refinitiv, Tradingkey.com

Figure 4: Personal income and spending growth (m-o-m, %)

Source: Refinitiv, Tradingkey.com

Given the slowdown in PCE—one of the Federal Reserve’s most closely watched metrics—and early signs of economic weakening, we expect the central bank to cut interest rates 3-4 times by the end of this year, significantly more than the two cuts currently priced into market expectations. If our assessment of the Fed’s rate-cut path proves correct, over the medium term (3-12 months), the USD Index and Treasury yields are likely to peak and retreat. With the resumption of a rate-cutting cycle, we also anticipate further upside potential for U.S. equities.