What Should Stock Investors Watch in Friday’s US Jobs Report?

TradingKey - At this point in time, the stock market is obsessing over how much the US Federal Reserve (Fed) will cut interest rates in 2025. Amid some uncertainty, particularly with the incoming Trump administration, and some robust economic data, the market has recently dialled back its expectations on monetary easing from the US central bank.

The next point of focus for investors is the monthly US job report, or employment numbers, that are released on Friday (10 January) before the market opens. Remember, the US stock market is closed on Thursday (9 January) to mourn the recent death of former US President Jimmy Carter.

So, when the market reopens on Friday, what should investors be looking out for from the latest US jobs report that covers the December 2024 period?

Cooling job market, still not yet in trouble

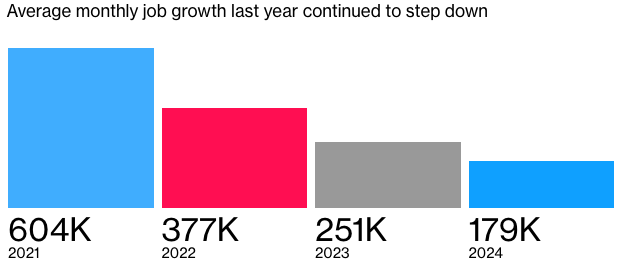

The last year or so has seen cooling job growth in the world’s largest economy and the numbers expected from the December jobs report look set to confirm this trend.

While the November payrolls report saw a huge 227,000 jobs added, some of this was making up for the below-trend October, when net job additions only totalled 36,000. That was down to two big hurricanes that hit the US in late September/early October.

However, the overall expectation for Friday’s report is a payrolls increase of 165,000, according to a median projection of economists surveyed by Bloomberg. That would put the average monthly job growth for the whole of 2024 at just shy of 180,000 and, if numbers come in as expected, it would be further evidence that the jobs market is starting to slow.

Jobs market healthy but slowing

Sources: Bureau Labor of Statistics, Bloomberg

If the Fed can engineer the “soft landing” that it wants for the US economy then a cooling jobs market is exactly what it is aiming for – following a reduction in inflation – as the jobs growth seen in 2021 and 2022 was red hot.

Recent Fed minutes give sign of what’s to come

On Wednesday (9 January) after the market closed, there was also the release of the latest minutes from the Fed’s December meeting that took place on 18-19 December 2024. Without calling out Trump directly, minutes from the meeting did outline the board’s worries about how both immigration and trade policy will impact the US economy.

The minutes read that “almost all participants judged that upside risks to the inflation outlook had increased” and that “participants cited recent stronger-than-expected readings on inflation and the likely effects of potential changes in trade and immigration policy”.

That was broadly in line with what the market was thinking – that the Fed will tread more carefully in the first half of this year to gauge how the incoming Trump administration’s policies play out.

In keeping with the “dot plot” from the December FOMC – that saw the Fed’s number of projected 25-basis point rate cuts for 2025 drop from four in September to just two – the Fed’s minutes read that the “committee was at or near the point at which it would be appropriate to slow the pace of policy easing”.

Looking towards data in the coming weeks and months

Investors can be certain that the jobs report, whether it’s an upside or downside surprise, will not significantly alter the Fed’s path unless other data points start to point towards an emerging trend. Currently, the unemployment rate in the US is at a very manageable 4.2% and the most recent JOLTs (job openings) report suggested that hiring remains robust.

For the stock market, it could mean further volatility in the weeks ahead as other key data come through – such as the consumer price index (CPI) and the Fed’s preferred gauge of inflation, the PCE Index. Furthermore, investors should be closely monitoring president-elect Trump’s entry into the Oval Office, which is set for 20 January.

Once Trump is back in office, investors will have a better idea of what his cabinet’s priorities are for 2025 and what that could mean for markets and, of course, interest rates.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.